The computer graphics team at Lucasfilm was working around the clock to finish their two minute animated short, The Adventures of Andre and Wally B., before the annual SIGGRAPH computer graphics conference in Minneapolis. However, it was becoming clear that the team would not finish in time. It was July 1984 and the animation that the Lucasfilm team had set out to make was far beyond its time. Instead of creating 15 second snippets of company logos dancing or flags waving in the wind (as they had seen in prior years), the Lucas team was attempting a two minute short story about a human-like figurine being chased by a bee through a forest.

Ed Catmull, of later Pixar fame, recalls how the Lucas team had underestimated the computing power needed to render all of their detailed images. As a result, their final product was unfinished with “wire frame images — mock-ups, made from grid polygons, of the finished characters — instead of fully colored images.” Ed recounts the moment when the unfinished short was unveiled at the conference (emphasis mine):

The night of our premiere, we watched, mortified, as these segments appeared on the screen, but something surprising happened. Despite our worries, the majority of the people I talked to after the screening said that they hadn’t even noticed that the movie had switched from full color to black and white wireframes! They were so caught up in the story that they hadn’t noticed its flaws.

This was my first encounter with a phenomenon I would notice again and again throughout my career: For all the care you put into artistry, visual polish frequently doesn’t matter if you are getting the story right.

This passage from Creativity Inc., Ed Catmull’s book on creativity in business and the rise of Pixar, demonstrates an important lesson for investors about how great stories can blind us from reality. Just like the viewers at the SIGGRAPH conference did not notice the flaws in the unfinished Lucasfilm short, investors tend to overlook investment flaws when enthralled by a compelling narrative. And financial history is riddled with cases that illustrate this.

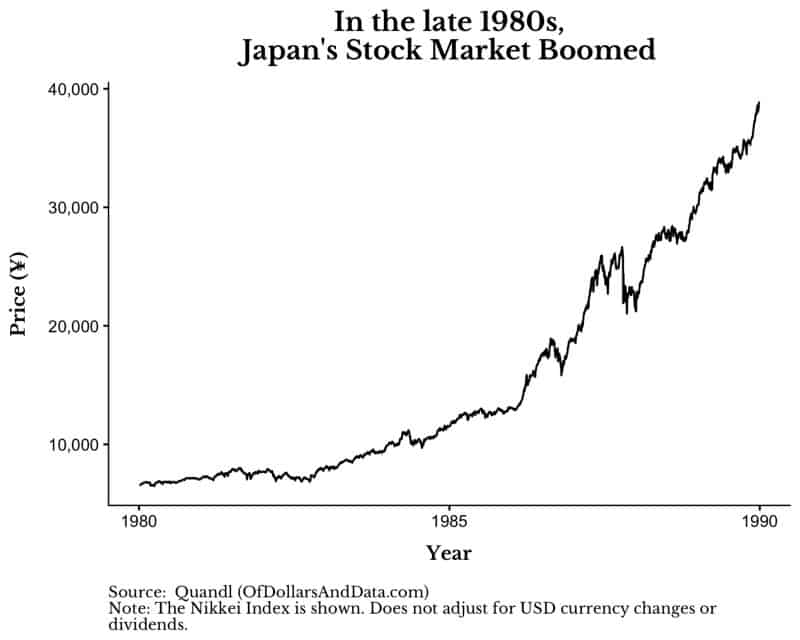

For example, in the late 1980s the story was that Japan was taking over the world. Their economy had been growing much faster than any other developed country and it was assumed that this level of growth would continue:

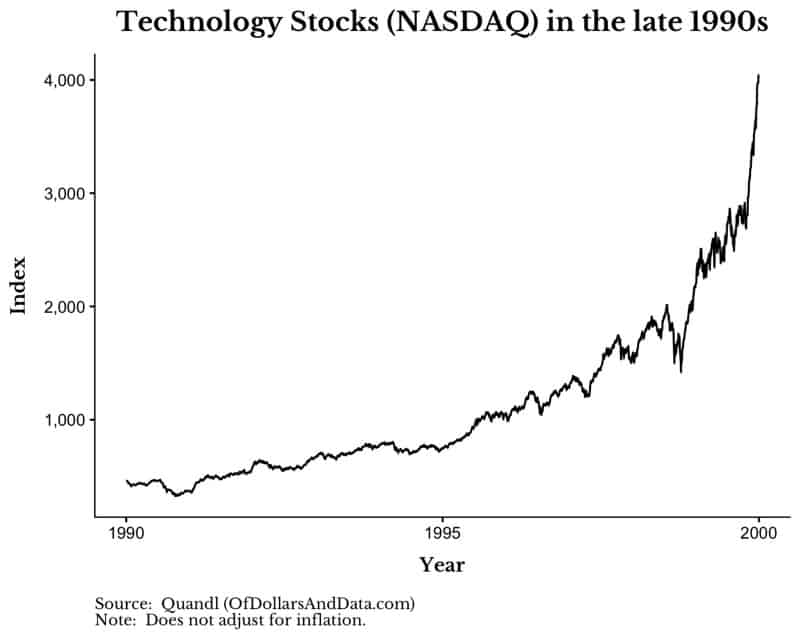

By the late 1990s, the story was that technology stocks were the future (Marc Andreessen argues this story was generally right, but too early):

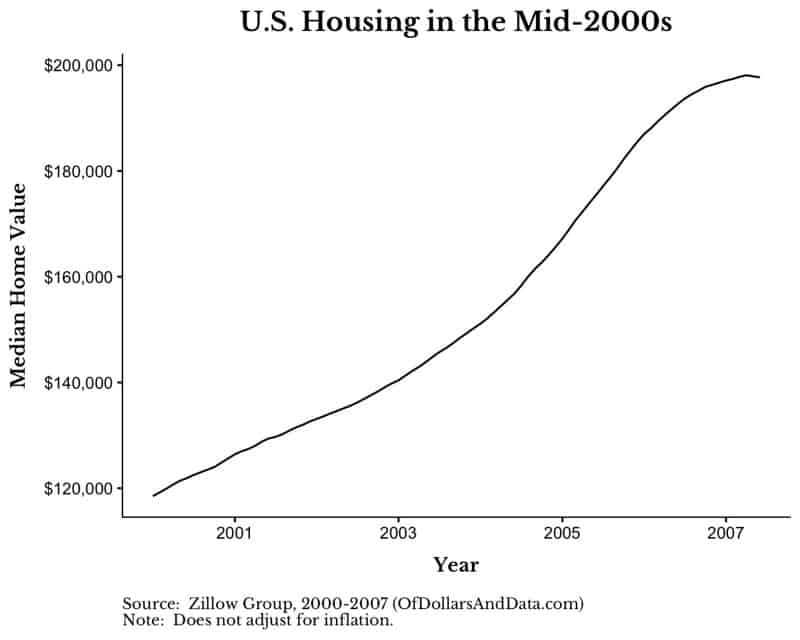

By the middle of 2006, the story was that you couldn’t lose money in U.S. housing (at least on aggregate):

As you know, all of these stories eventually rang hollow, but this was after investors collectively fell for the belief that “this time is different.” Don’t get me wrong, knowing when a story is valid has not been and will never be easy. However, realizing that stories are a key component of determining asset prices can help you understand why we continue to see irrational behavior in various asset markets throughout the world. As I like to remind myself, assets are not priced based upon fundamentals, but by what someone else is willing to pay for them. Or as John Maynard Keynes once said:

The market can remain irrational longer than you can remain solvent.

It is important to remember this because while earnings growth, dividend yields, and discount rates matter, ultimately, these are all viewed through the prism of belief. You and I can have the same information, but have very different interpretations based on the stories we tell. Ben Carlson illustrated this wonderfully when he recently tweeted about the changing story behind cryptocurrencies:

However, stories can do much more than this. Carlson also wrote a great post on the power of narrative where he highlighted a deep insight from Josh Wolfe:

I love Wolfe’s idea about how amazing storytellers can lower the cost of capital because they can raise expectations.

Just think about how profound this is. If you can tell a good enough story, you can raise someone’s expectations (i.e. reduce their discount rate) and, thus, increase their willingness to pay for something. You didn’t change earnings growth. You didn’t change management. You didn’t change strategies. You just told a better story.

What Story Are You Telling?

Every investor has a story they tell themselves in regards to their portfolio. What’s yours? Is it “I can beat the market by picking stocks”? Is it “I am clueless about the future, so a basket of global stock and bond indices is the way to go”? I can’t help you define your story, but thinking about it should help you uncover any possible flaws you might be overlooking.

Lastly, if you want to dig deeper, I highly recommend Sapiens by Yuval Noah Harari and Ben Carlson’s other post on this topic. Thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 64. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data