With the S&P 500 now 8.6% off its recent highs, I’ve seen quite a few people argue that a market crash can be a good thing, especially for younger investors. As Chamath recently tweeted:

The upside of shrinking these asset prices is that it gives [young and working class people] a legitimate chance to buy into those markets at lower levels, making equity ownership and/or home ownership more possible.

All else equal, this is correct. If we assume that the market will eventually recover, then a decline in equity prices today allows young and “asset-light” investors to buy cheaper today and earn higher returns in the future.

But the problem with this logic is that all else isn’t equal. Market crashes don’t happen in a vacuum. When asset prices decline, economic consequences typically follow. Workers lose their jobs or don’t get promoted. Hiring freezes up. People stop spending as much money. And this negative cycle feeds on itself.

If you happen to be someone who keeps their high-paying job during such a time, then, yes, a market decline can be a buying opportunity. But this isn’t the case for everyone. In fact, the paper The Short- and Long-Term Career Effects of Graduating in a Recession suggests that those who start their career during a recession tend to see 5% lower lifetime earnings. As the authors state:

A typical recession—a rise in unemployment rates by 5 percentage points in our context—implies an initial loss in earnings of about 9 percent that halves within 5 years, and finally fades to 0 by 10 years. For this time period, these reductions add up to a loss of about 5 percent of cumulated earnings.

I know what you might be thinking: “Yes, I lose 5% of my lifetime earnings, but I get to buy stocks at a 20%+ discount. How is that not a huge win?”

There are a few problems with this thinking, each of which I will address in turn.

A Small Loss in Earnings means a Bigger Loss in Savings

A small reduction in your current earnings is likely to have a much bigger impact on how much you can save each year. If this is the case, then you’d be much worse off with lower earnings (and stock prices) then if stocks never declined at all.

For example, imagine someone earning $100,000 a year (after tax) that spends $80,000 a year. This would give them a savings rate of 20% [$20,000/$100,000 = 20%]. But now drop their earnings by 5% (-$5,000) without changing their spending. In this case, their annual savings go to $15,000 a year. That’s a 25% decline in savings from just a 5% decline in earnings!

And if stock prices are only down 20%, then you are buying fewer stocks today because your savings declined by more than stock prices did. Quick math to prove this: imagine an S&P 500 ETF is priced at $100. With $20,000 in savings, you could buy 200 shares [$20,000/$100]. If the price declines to $80 a share (a 20% decline), but your savings also decline to $15,000 annually, you can now only buy 187.5 shares [$15,000/$80].

More importantly, a 5% decline in your earnings might seem small, but across your lifetime it’s HUGE. If we assume that you will earn anywhere from $2M-$4M throughout your career, then a 5% drop would be $100,000-$200,000. And these earnings will come directly out of your savings, all else equal. Do you think a few discount stock purchases in your 20s are going to make up for losing $100k-$200k? No chance.

Price Discounts Don’t Last Long

The other problem with the argument that “market declines are good for younger investors” is that stock prices don’t stay depressed forever. So even if you have a moment to buy stocks at a discount, relative to all of the investments you will make across your lifetime, the impact will be marginal.

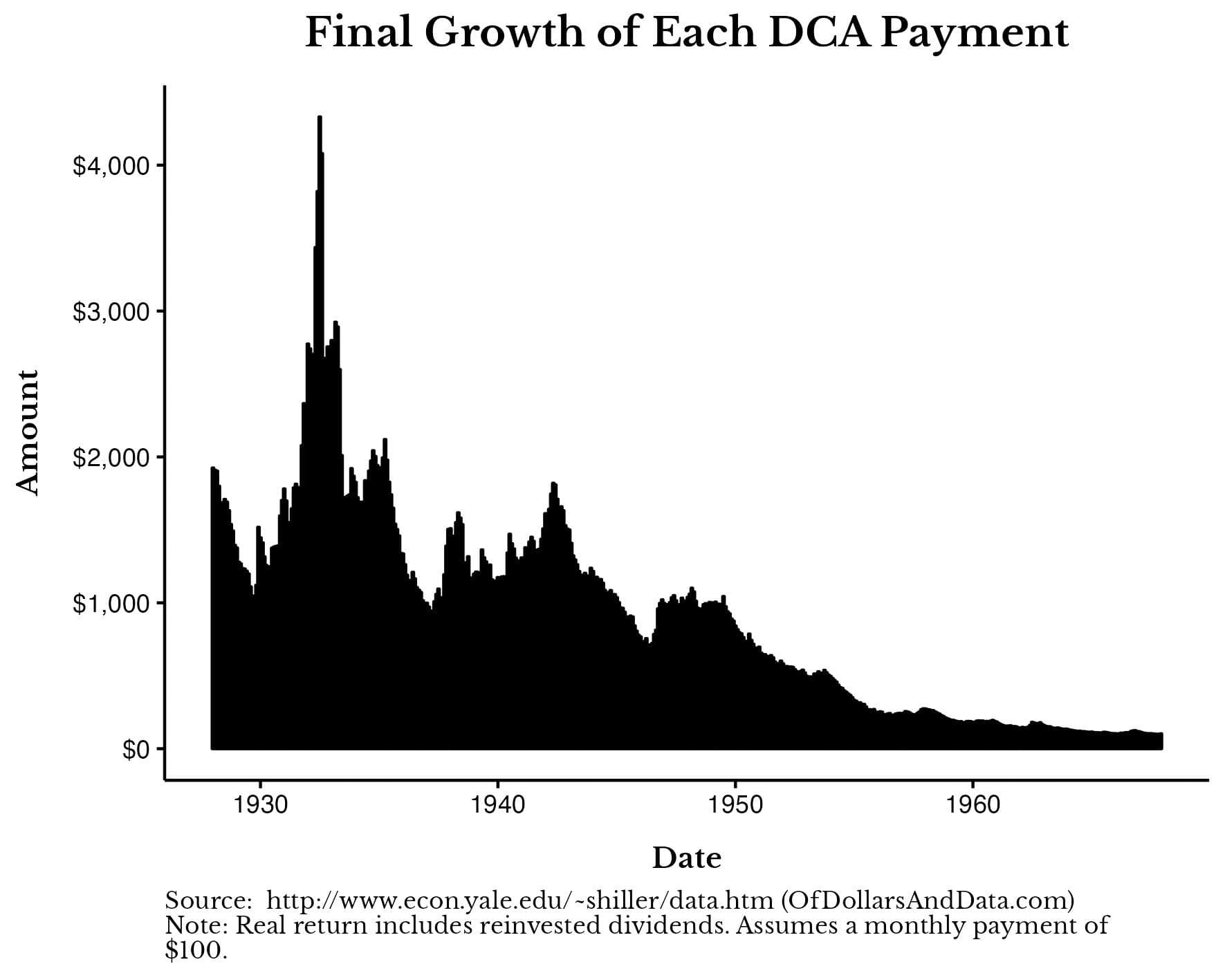

For example, imagine you invested $100 a month into U.S. stocks throughout the Great Depression. How much more money would you have made off your purchases made near the bottom compared to the purchases made right before or after? Only about 2x. The chart below shows what each $100 payment would grow to from when it was made until 1968 (the end of the 40 year analysis period):

As you can see, the payments made during the bottom in 1932 grew by about 2x more than the payments made in the years immediately before or after. Don’t get me wrong, that’s a great return. But, across your lifetime, these handful of purchases will only have a marginal impact. They won’t be the difference between poverty and financial freedom. They are just going to make your retirement slightly nicer. Keep this in mind before rooting for a market crash.

It Will Never Happen to Me

Lastly, a market crash can seem like a buying opportunity if you think that it will have little impact outside your portfolio. So far we’ve only analyzed the scenario where you see a 5% decline in your lifetime earnings due to a recession early in your career.

But what if you experience something far worse? What if you lose your job? What if you can’t find work at all? What if you have to financially support a family member? It’s easy to talk about market crashes in theory, but in practice they can be far more challenging.

The problem is that market crashes don’t exist independent of the economy. It’s like those people who want to buy a house but are waiting “until prices crash.” Do you think there exists a world where housing prices crash and everything else stays the same? No way. If housing prices decline in a material way, there will be many other problems you will need to deal with in the meantime.

The same thing is true of financial crises in general. Such declines have higher-order effects that could create problems for you that you would never anticipate. I’m not trying to scare you, but believing that “it will never happen to me” is no way to run your financial life either.

The solution to this problem isn’t to hope for a recession though, it’s to make sure you’re prepared for one.

Don’t Hope, Prepare

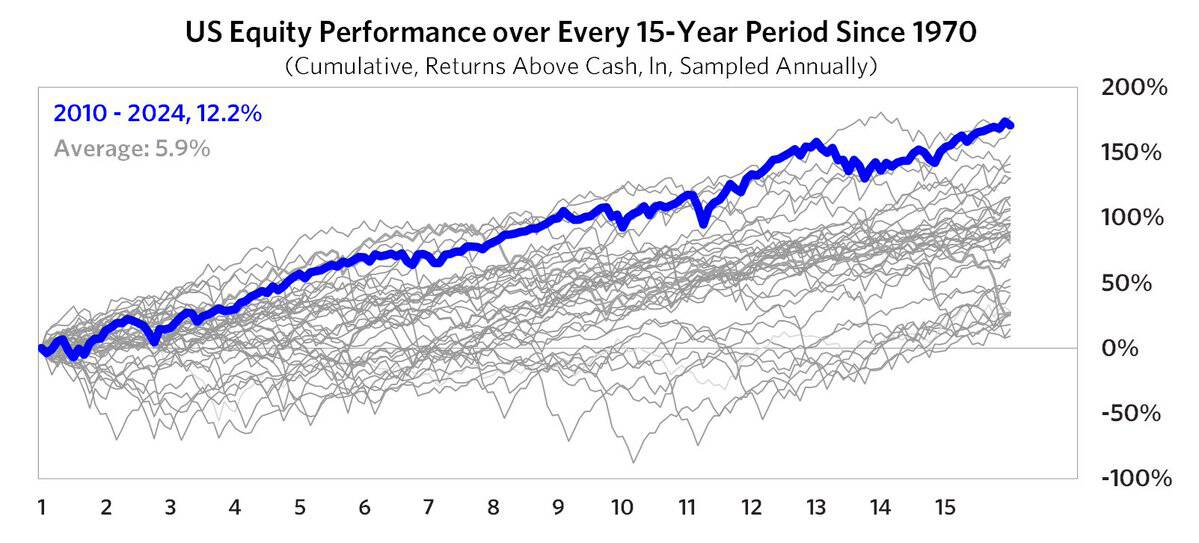

Meb Faber’s Idea Farm recently pointed out that the past 15 years were the best 15-year period for equities (relative to cash returns) going back to 1970:

While this doesn’t imply that a crash is guaranteed, we also know that bull markets don’t last forever. The truth is that no one knows what is going to happen next, especially with the uncertainty in Washington. But what I do know is that it doesn’t hurt to prepare for the worst.

How do you do that? Here are a few of my thoughts:

- Know Your Portfolio. Saying you’re diversified is one thing, but knowing it is another. Make sure that your portfolio has both risk and non-risk assets (e.g. Treasury bills, short-term bonds) to weather a financial storm. It also doesn’t hurt to own some asset classes that are less correlated with equities. This may include: physical real estate, gold, art, crypto, and others. While I am not a fan of owning a lot of non-income producing assets (e.g. gold, art, crypto, etc.), these assets can provide diversification benefits to a traditional stock/bond portfolio.

- Know Your Network. Having the right portfolio is just the beginning though. If you really want to prepare for a recession, you should know your network. For many people, the greatest asset in a recession isn’t their portfolio, but their connections. And when I say connections, I don’t just mean your closest friends and family, but your acquaintances as well. Some research suggests that it’s actually these “weaker ties” (e.g., friends of friends) that are most likely to help you find a new job. This is why it’s important to ensure that your network is strong before you ever have to use it.

- Know Your Budget. While I’m not a fan of cutting spending as a way to build wealth, during a recession it’s a different story. Knowing how much money you have coming in and going out is helpful during the good times, but it’s absolutely essential in the bad ones. The first thing you should do is audit your spending to see if there is anything that you can reasonably cut out. The goal is to provide you with a little more wiggle room while times are tough. Once you’ve done that, the rest is about waiting things out until economic conditions improve.

- Know Your Opportunities. Last, but not least, look for new opportunities that emerge during difficult times. It’s easy to see recessions only as periods of destruction, but they can also be periods for growth. If you’ve ever wanted to start a business or take a different path, a recession may provide the right environment to do so. During economic crises, there tends to be less competition, lower costs/better terms, and more access to talent than during normal times. Taking advantage of such conditions could help you make the pivot that redefines your career. Of course, there can be risk with such actions, but the risk may be lower than normal during such uncertain times.

Ultimately, recessions aren’t opportunities to celebrate, they’re challenges to overcome. And while such events can provide unique investment opportunities, the broader economic damage they typically cause outweighs such benefits.

Therefore, instead of hoping for a market crash, make sure you are prepared for one. By knowing what’s in your portfolio, your network, your budget, and your opportunity set, you can ensure that you face the future with confidence. As Zig Ziglar was known to say, “Success is when opportunity meets preparation.”

Until then, happy investing and thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 441. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data