Sam Walton created more wealth in the twentieth century than almost anyone else. His relentless spirit to compete while building WalMart is the reason why the Waltons are still the richest family in America with a combined net worth of over $150 billion. What I found most interesting about Walton’s story, which you can read in his autobiography Sam Walton: Made in America, was his willingness to experiment and challenge his own beliefs while trying to become the best retailer in America.

Sam’s intensity with experimentation was unparalleled. He would sell popcorn and ice cream in his stores to get more foot traffic. He would go around middlemen in the supply chain to reduce prices. He would visit his competitors’s stores to steal their ideas. There is even a story (which I can’t seem to find a good source for) about the night Walton was thrown in a Brazilian prison because he was caught on all fours measuring the width of the aisles of one of Brazil’s largest retailers.

The point is that Walton was so obsessed with retailing that he wasn’t worried about destroying his old beliefs if he found new evidence that contradicted it. David Glass, who was once the CEO of WalMart, further highlights this point (emphasis mine):

Two things about Sam Walton distinguish him from almost everyone else I know. First, he gets up every day bound and determined to improve something. Second, he is less afraid of being wrong than anyone I’ve ever known. And once he sees he’s wrong, he just shakes it off and heads in another direction.

I bring up Walton and his fearlessness about being wrong, because today I want to do the same exercise by playing devil’s advocate against my own investment beliefs.

I first had this idea after I realized that many of the individuals in the finance community (myself included) end up consuming much of the same content. For example, I had flagged a particular quote from The Success Equation I wanted to use in a blog post and that same day Michael Batnick sends out a tweet with the exact quote I had highlighted:

The very next day Morgan Housel independently tweeted another quote from this book and I started to ask myself whether FinTwit was an echo chamber of sorts. For the record, this community is very intellectually honest and evidence based, but I sometimes wonder if our collective thinking becomes too aligned at times. We read the same blog posts. We listen to the same podcasts. We see the same Tweets. So what ideas might we need to challenge? Consider the following:

- We believe that equity markets will compound at a reasonable positive rate for the foreseeable future

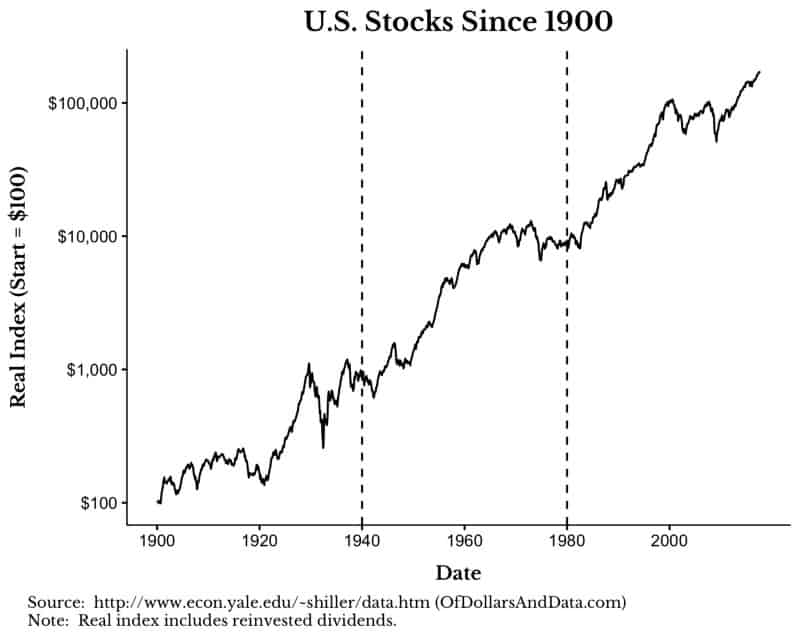

Don’t get me wrong, we have hundreds of years of evidence suggest that this statement will hold true (see Triumph of the Optimists). Therefore, it is not unreasonable to assume that global equities will compound at some non-zero real rate going forward. However, what if this belief doesn’t hold? There have been periods of history where humanity regressed economically. Shall I remind you of the Dark Ages? While I don’t think this is likely to occur again, how much confidence do we really have for equity markets over the next century? For example, consider this chart:

What does it show you? Does it show that the U.S. stock market always goes up over longer time periods (40 years) since 1900? Technically, yes. But, consider how little data this belief is based on. It contains 3 non-overlapping 40 year investment periods. That’s it. 3 data points and we almost never question the long term soundness of U.S. equity markets or equity markets in general. Consider how many other ideas like this are based on a short record of history.

- We extrapolate present conditions into the past

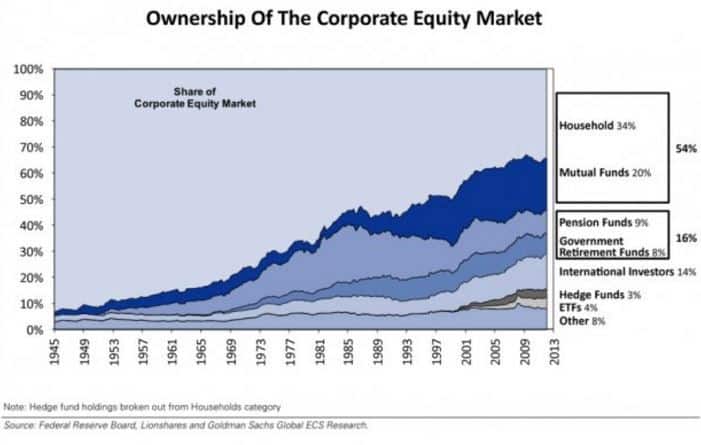

I am as guilty of this as anyone else, but I’ve noticed that we spend a lot of time discussing long term investing without much regard to how much investing has changed from one generation to the next. How can we compare investors from 1920 to today when they are so different? Consider this chart which shows equity market ownership breakdown from 1945–2013:

The typical investor in 1945 had a far different experience than one today. Those investors had to take far more risk because diversification wasn’t easy/cheap and they had to pay higher fees and transaction costs along the way. Additionally, in the 1940s there were few investors in the space because most individuals had no need to invest because of the reliance on defined benefit programs.

These material changes matter because they could also lead to a reduction in future returns. If you are skeptical, I ask you to consider this question: if investing is so cheap/easy today, why should it offer the same level of returns as when it was far harder? I will admit my thinking on this might be wrong, but I still haven’t heard a sufficiently good reply to this question, all else equal.

Echoes for Eternity

Even if I am right about the possibility of an “echo chamber” in the finance community, what difference does it really make? The market is going to give us some set of future returns and, as investors, we will have to live our lives with those returns. While Sam Walton was able to run hundreds of experiments to see what worked best, we don’t have that luxury as investors. Yes we can backtest all we want, but that only tells us what used to work, not what will work in the future.

Despite the “echoes” I sometimes hear, the online finance community is one of the most intellectually honest communities I have ever been a part of. Generally, bad arguments don’t get much traction and there are always people present to let you know when you might be wrong (props to Jake). While I don’t fundamentally agree with a lot of the arguments I made here today, it was the act of making them that was of the upmost importance.

Thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 67. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data