Imagine you are sitting on an asteroid in deep space and you have a friend who has a spaceship that can travel at 99% the speed of light. Yes, this is physically impossible for a host of reasons, but bear with me for now. Out of boredom you decide to challenge your friend to a race — their spaceship vs. a beam of light. Your friend agrees, but you have to give them a small head start.

Shortly after the race begins, your friend is moving away from your asteroid at 99% of the speed of light when you send out the beam of light to race alongside them. From your perspective on the asteroid, you will see the beam of light pass your friend’s spaceship like a faster car passing a slower car on a freeway. After all, 100% the speed of light is faster than 99% the speed of light. However, what will your friend experience on their spaceship?

You might think that your friend will also see the light beam pass them like a slightly faster car on a freeway, but this is incorrect. Your friend will see the light beam pass them at the speed of light. Why? Physicists discovered that the speed of light is constant for all observers. Given this is true, how is it possible that you and your friend can see the same event, but it will take you more time to view it?

The answer is: as your friend’s velocity approaches the speed of light, their time slows down. You can calculate how much time slows as you approach light speed using the Lorentz factor. For example, in the thought experiment above (i.e. 99% the speed of light), 7 seconds of your time would only take 1 second of your friend’s time. This idea, which is one of the most amazing and unintuitive in all of physics, is known as time dilation and comes from Einstein’s theory of special relativity.

I tell you about time dilation and special relativity because they illustrate an important truth about the universe and investor experience…it’s all relative. In the thought experiment above you and your friend experience the same event very differently without noticing it. You both will experience 1 second of time the same way, but what happens in that second is very different. This is just as true in investing where you and I will experience the same market event very differently because of our biases, our personal investment history, and other ideas that have shaped our worldview.

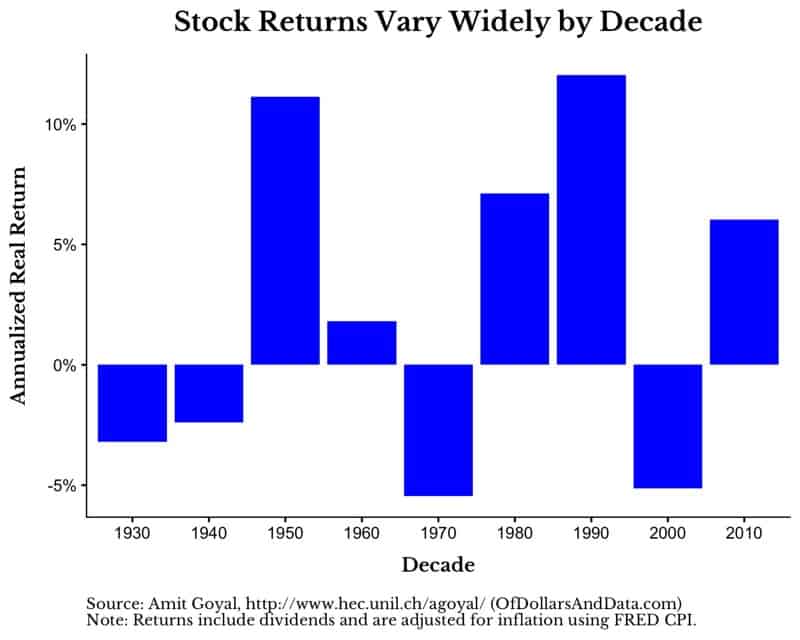

For example, consider real U.S. stock returns by decade (including dividends):

When you look at this chart what conclusion do you draw? Yes, returns vary, but does that mean that we should just buy and hold? Does it imply that investing is mostly luck? The investors from the 1930s and 1940s will likely have a very different answer than those from the 1980s and 1990s.

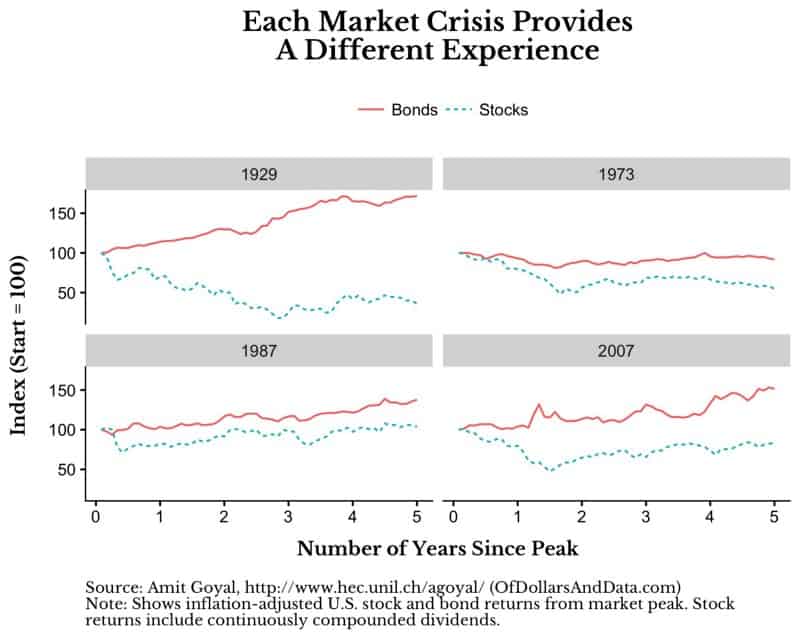

We can go further and compare U.S. stock and bond returns during the biggest stock market crashes of the past century. If we start at the peak before the crash, we can see how each market crash provides a different experience for the investors of that era:

However, this graphic isn’t the best we can do. We can overlay these peaks on top of each other to get an even better comparison of each one:

As you can see, each one of these periods provided a different takeaway for investors. I might say, “Bonds provide stability when stocks crash,” but the investors of 1973–1974 would say, “Not so fast.”

The point is that realizing your financial frame of reference can be helpful for understanding how you might react to future market events. For example, I know that I am biased against real estate investments because I saw my parents lose their home in the housing crisis of 2007–2008. This is clearly an example of recency bias clouding my judgement, but I honestly can’t seem to shake it though I know better.

So ask yourself: what is your financial frame of reference? Are you biased for or against any particular asset class? If so, do you have evidence for this? Studying market history can help to tame these biases, but they will always be difficult to overcome. So next time you hear someone make a comment about the market, before you agree or disagree, remember the relative lens through which they (and you) view the financial world.

Absolutes in a Relative World

I recently had dinner with a private wealth manager who told me about a client of his who got upset with him for placing a trade in a mutual fund instead of an ETF. For those of you that don’t know, mutual funds trade at closing prices while ETFs trade at the time of execution. On that particular day, the market rose from 3pm (when the trade was placed) to 4pm (closing time). As a result, this particular client paid an extra 25 basis points (0.25%) due to the price increase over the last hour of the day.

This might seem like a small cost, especially to someone worth upwards of $10 million who was trading only $20,000, but that client was furious that they didn’t get the absolute best price. This is an example of financial relativity gone wrong. From an absolute perspective, you and I can see the 25 basis points is irrelevant in the long run, but it didn’t feel that way to the client.

I tell this story because I think the key to happiness in life and finances is remembering the absolutes in a relative world. Studies suggest that people prefer having more relative wealth over absolute wealth, but that doesn’t mean you should fall into the same logical trap. Despite the evidence that we are living in one of the greatest times in history, relative minds will always think otherwise. With that being said, I will leave you with a story that illustrates this point as told by Jack Bogle, the founder of Vanguard:

At a party given by a billionaire on Shelter Island, Kurt Vonnegut informed his pal, the author Joseph Heller, that their host, a hedge fund manager, had made more money in a single day than Heller had earned from his wildly popular novel Catch 22 over its whole history. Heller responds, “Yes, but I have something he will never have . . . Enough.”

Thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 59. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data