Retirement planning is an essential part of personal finance that requires careful thought and consideration. One of the most popular retirement savings vehicles in the U.S. is the 401(k) plan, which allows employees to make pre or post-tax contributions to a dedicated investment account. Many financial experts recommend maxing out your 401(k) to take full advantage of the tax benefits, but is this the best strategy for everyone?

The evidence suggests that it may not be.

In this blog post, I will answer the question: “should I max out my 401k?” by demonstrating that the benefits associated with maxing out your 401(k) aren’t as large as you might believe. I will do this by first explaining how a 401(k) works. Then I will discuss the potential drawbacks of maxing out your 401(k). And, finally, I will quantify the annual tax benefit of a 401(k) and why maxing out may not be worth it for you.

My hope is that this post will provide you with the right information to make the best decision for your financial future. With that being said, let’s get started by reviewing the basics of a 401(k) plan.

The Basics of a 401(k) Plan

A 401(k) plan is a retirement savings account sponsored by an employer which allows employees to save and invest a portion of their paycheck into a tax-advantaged investment portfolio.

How a 401(k) Works

- Contributions: Employees can elect to contribute a percentage of their pre-tax salary to a traditional 401(k) plan and/or a percentage of their post-tax salary to a Roth 401(k) plan (if offered by their employer).

- For example, if you have a salary of $100,000 and you contributed $10,000 into a traditional 401(k), that $10,000 would not be subject to federal income tax nor state and local income taxes (in most jurisdictions). While this $10,000 would still be subject to FICA taxes (Social Security and Medicare), your total taxable income at year-end would only be $90,000 [$100,000 – $10,000 pre-tax 401(k) contribution].

- On the other hand, if you contributed $10,000 to a Roth 401(k), that $10,000 contribution would occur after paying all relevant federal, state, and local income taxes. Contributions to a Roth 401(k) do not lower your taxable income, so you would have a taxable income of $100,000 at year-end.

- If you want to figure out whether a traditional 401(k) or a Roth 401(k) is better for you, check out this article.

- Investments: The funds in a 401(k) account can be invested in a variety of asset classes, including stocks, bonds, cash, and real estate. Investments are typically made into diversified index funds and mutual funds. While these funds often provide investors with easy diversification, it’s important to be aware of the fees (e.g., expense ratios) associated with the options in your plan.

- Tax-free growth: The benefit of a 401(k) is that all of your contributions grow tax-free. In other words, you won’t have to pay capital gains taxes on the growth in your investments. As long as you wait until you are 59½ to make withdrawals from your account, the only taxes you will ever pay for on 401(k) contributions are income taxes. You either pay income taxes on your withdrawals in retirement (if you have a traditional 401(k)) or income taxes before making contributions while working (if you have a Roth 401(k)).

- If we assume that you pay the same tax rate on withdrawals (in retirement) as you do on contributions (while working), then a traditional 401(k) and a Roth 401(k) are identical investment vehicles. That means that there’s no difference between choosing one or the other (if your tax rate is constant). If you don’t believe me, read this article until you do.

Contribution Limits, Employer Matching, and Vesting

- Annual contribution limits: The IRS sets annual limits on the amount individuals can contribute to a 401(k). When you contribute to this limit, you have “maxed out” your 401(k). For 2023, the maximum contribution limit is $22,500, with an additional catch-up contribution of $7,500 for those aged 50 and older.

- Employer matching: Some employers offer matching contributions to their employees’ 401(k) plans, effectively providing “free money” as an incentive to save for retirement. Matching programs vary, but a common arrangement is a 50% match up to a certain percentage of an employee’s salary.

- For example, if a company has a 50% match on up to 4% of your salary, then you would need to contribute 8% of your salary to your 401(k) to get your full employer match. In other words, when you contribute 8%, your company contributes an additional 50% of that (or 4% of your total pay) into your 401(k) as well. If a company offers a 100% match on up to 4% of your salary, then you would only need to contribute 4% of your pay to get the full employer match.

- Unless you are in a dire financial situation or your company’s 401(k) plan is atrocious (i.e. high fees or terrible options), then you should always contribute up to the employer match in your 401(k). Though there are debates to be had about maxing out your 401(k), the employer match is an instant 100% return on your money that you won’t get elsewhere.

- Lastly, all employer matched funds are made into a pre-tax account (like a traditional 401(k)). Even if you are making post-tax contributions to a Roth 401(k), your employer matching contributions will be pre-tax.

- Vesting of matched contributions: Be mindful as to when your employer’s matching contributions vest (or become yours to keep). Though some companies give you your matching contributions right away (so if you leave the company you can take them with you), others require you to stay a certain number of years before your matching contributions are yours (or become “vested”).

- For example, a company may say that your matching contributions vest by 25% every year (over four years). So if you leave before one year of employment, you get no matching contributions (0% vested). If you leave after one year, but before two years, you get 25% of your employer matching contributions (25% vested), and so forth.

Now that we’ve reviewed the basics of a 401(k), let’s look at some of the potential drawbacks of maxing out your 401(k).

The Potential Drawbacks of Maxing out a 401(k)

While there are undeniable benefits to contributing to a 401(k) plan (especially up to the employer match), going beyond the employer match and maxing out your contributions may not always be the most advantageous strategy. Here, we explore some potential drawbacks of maxing out your 401(k).

Limited Investment Choices

Employer-sponsored 401(k) plans often come with a limited selection of investment options compared to other investment vehicles, such as IRAs or taxable brokerage accounts. As a result, you may not have access to the same asset classes and you might have to pay more for them as well. If all the funds in your employer’s 401(k) plan have higher expense ratios (>1%), then you may have no choice but to pay such fees even though cheaper options are available elsewhere.

Fees and Administrative Costs

Speaking of fees, 401(k) plans are often subject to various fees and administrative costs, such as expense ratios, management fees, and record keeping fees. In fact, the average American typically pays about 0.45% in total 401(k) fees each year. These fees can erode your investment returns over time, particularly if the available investment options carry high expense ratios or other charges.

Illiquidity and Early Withdrawal Penalties

401(k) accounts are generally less liquid than other investment accounts due to restrictions on withdrawals before the age of 59½. While you technically can withdraw your contributions from a Roth 401(k) early, I don’t think you should view your retirement accounts in this way.

Additionally, early withdrawals from a 401(k) account are typically subject to a 10% penalty, in addition to being taxed as ordinary income. This can make it difficult to access these funds in case of financial emergencies or other unexpected expenses.

Less Financial Optionality/Flexibility

By maxing out your 401(k) contributions, you may be overly concentrating your wealth in tax-deferred accounts, potentially limiting your financial flexibility and tax planning options in your future. I feel like I made this mistake by contributing too much to my 401(k) throughout my 20s. While my retirement projections look great now, I placed some limits on what I can do with my money now.

For example, because of my excessive 401(k) contributions I can’t afford the sizable down payment needed to buy a place in Manhattan. Yes, Manhattan is one of the most expensive housing markets in the U.S., but having an extra $50,000 outside of my retirement accounts would make it easier to afford.

While I’ll admit that this is partially my fault for not planning ahead, I was also seduced by the “max out your 401(k)” advice I heard so often when I was younger.

Higher Future Tax Rates

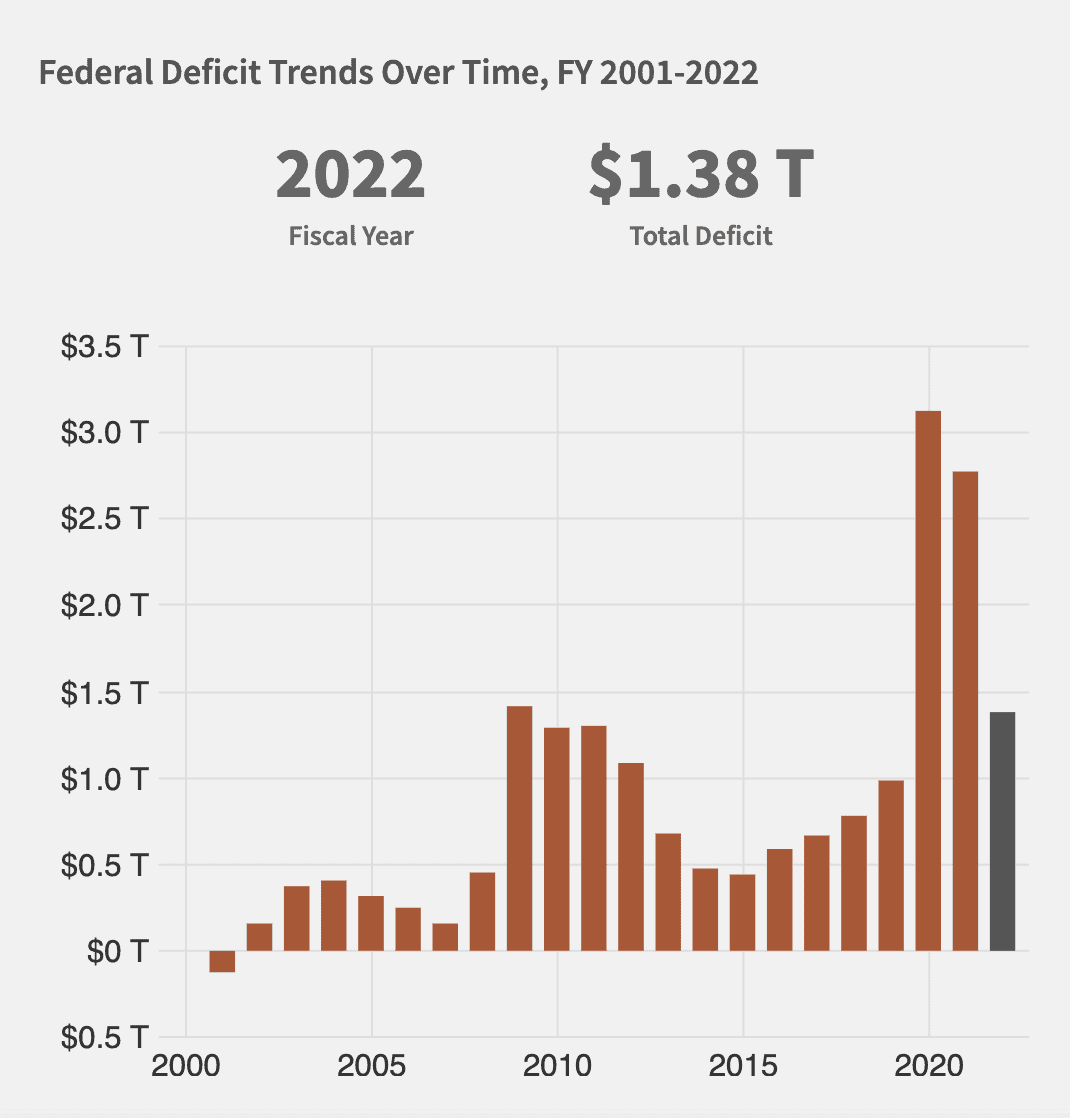

If you are contributing to a traditional 401(k), there is the possibility that you will have to pay much higher taxes in the future. I will admit that I can’t predict the future of U.S. tax policy, but it’s hard to imagine how the U.S. keeps running deficits like the ones pictured below without increasing future tax rates:

I don’t show this chart to cause alarm, but to rationally consider the most likely path forward. Does this chart suggest that taxes will go down over the next few decades? Then why would you put so much of your money into an investment vehicle whose tax rate will be determined by a future Congress that will likely be in dire need of cash?

This is the biggest risk I see to maxing out a traditional 401(k). Contributing up to the employer match is a no brainer that every investor should participate in (if they can). However, beyond that and you have to start considering the tradeoffs much more seriously.

To prove my point, let’s look at the actual annual tax benefit associated with maxing out your 401(k) to see if maxing out is still worth it.

What is the Tax Benefit of Maxing Out a 401(k)?

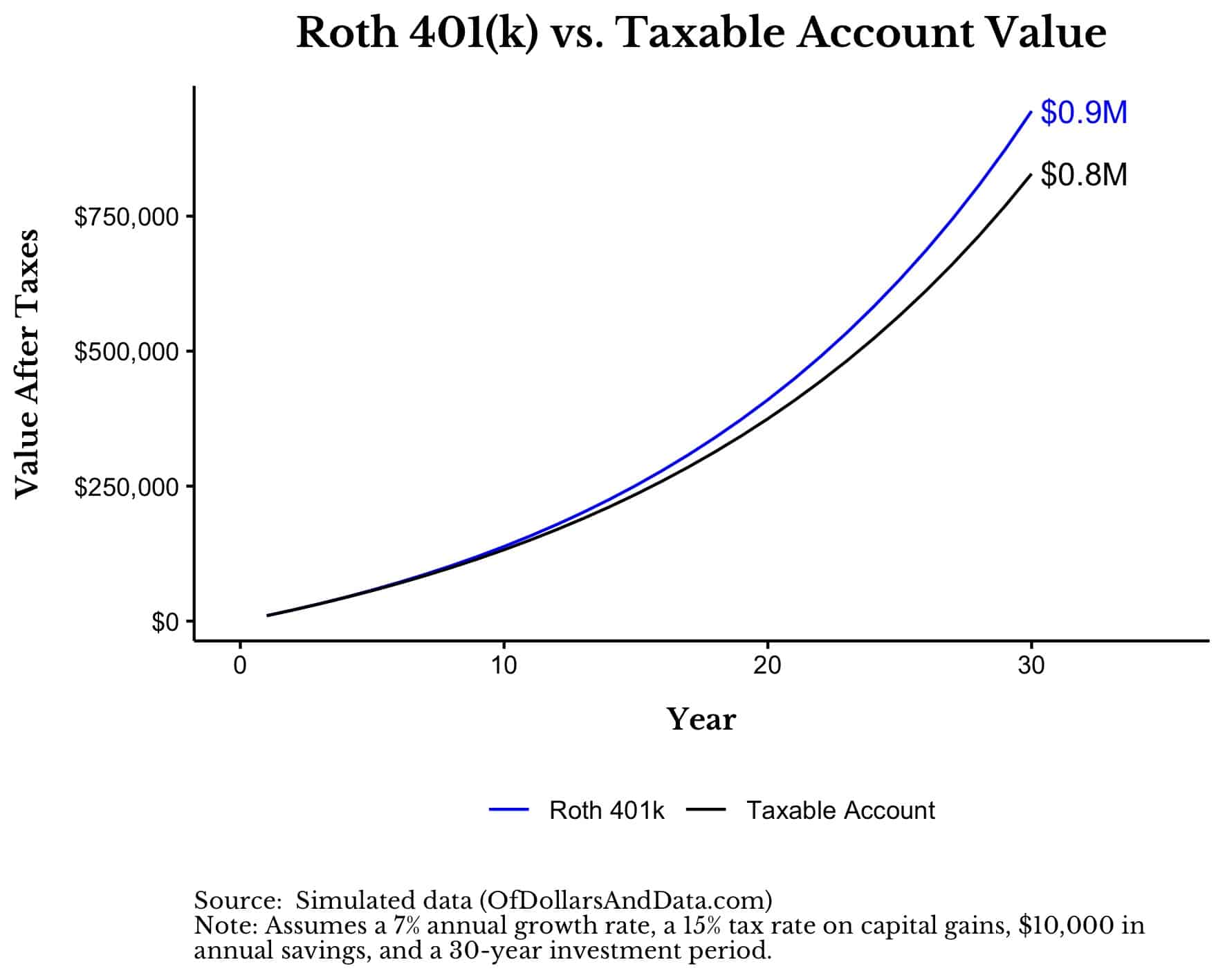

To find the long-term tax benefits of maxing out your 401(k), I will compare a $10,000 annual investment into a Roth 401(k) versus a $10,000 annual investment into a taxable account (i.e. brokerage) over 30 years.

Note that I am using a Roth 401(k) and not a traditional 401(k) because I only want to figure out the benefit of avoiding capital gains taxes in a 401(k). As I stated above, this is the main tax benefit associated with using a 401(k) as compared to a taxable account. Therefore, since contributions made into a Roth 401(k) and a brokerage account are both after income taxes have been paid, the only difference in their long-term growth is the capital gains taxes that the Roth 401(k) avoided.

For this comparison, I assumed that both accounts grew at 5% a year and that the taxable account had to pay the long-term capital gains rate of 15% on a 2% annual dividend and when the portfolio was sold (in the last year). This means that no sales were made in the taxable account until retirement (when all long term capital gains taxes are paid). It’s buy and hold for three decades.

After running this simulation for 30 years, I found that the Roth 401(k) ended up with $114,000 more than the taxable account (after all capital gains taxes had been paid):

That $114,000 means that the Roth 401(k) ends up with 14% more than the taxable account after 30 years. How much of an annualized benefit is this when we consider all contributions? 0.73%. That’s it. You get 0.73% in extra return each year to lock up your capital until you are 59½.

More importantly, my analysis assumes that you have the same investment options (and pay the same fees) in a Roth 401(k) as you would in a taxable account. But, as I demonstrated in the previous section, this isn’t always true.

In fact, if the investment options in your employer’s 401(k) plan are just 0.73% more expensive than what you would pay in a taxable account, then the annual benefit of a Roth 401(k) would be completely eliminated!

For example, if we assume that you would have to pay 0.1% per year in fees to get a diversified portfolio in a taxable account, then paying anything more than 0.83% (0.73% + 0.1%) in your Roth 401(k) would eliminate its long-term tax benefit entirely. And since we know that the average American pays 0.45% in 401(k) fees each year, this means that the typical American’s 401(k) plan provides about 0.38% per year (beyond the employer match) in tax benefits relative to a well-managed taxable account.

Of course, if the fund fees in your employer’s 401(k) plan are low (0.2% or less), then there is still some monetary benefit to maxing out. But, you should ask yourself: is 0.6%-0.7% a year worth locking up a decent part of your wealth until old age? I’m not necessarily sure.

And while this estimate was only relevant for a Roth 401(k), assuming that your tax rate will stay the same over time, then a traditional 401(k) would provide the same annual tax benefit of 0.73% per year. However, if tax rates increase enough over time (as I argued they might in the prior section), then this benefit could be completely eliminated.

Now that we have quantified just how much of a tax benefit a 401(k) provides (above a taxable brokerage account), let’s wrap things up by explaining why maxing still might make sense for some people.

The Bottom Line

Regardless of whether you use a Roth 401(k) or a traditional 401(k), the benefits of contributing beyond the employer match are smaller than you might have initially imagined. My issue with this is that so many personal finance experts have sung the praises of “maxing out your 401(k)” without providing any data to back up their claims.

How do I know? Because I used to be one of them. I used to advocate maxing out your 401(k) because it seemed like the logical thing to do. And with so many other financial personalities championing the same thing, why would I even question it?

But since running the numbers, I know better. This is why it’s hard for me to support maxing out your 401(k) for an extra 0.73% per year. That illiquidity premium is just too small to be worth it even if you don’t need the money for something like a down payment on a house. And for those with a traditional 401(k), the benefits seem likely to be even smaller given the current trend of U.S. deficit spending and the possibility of future tax increases.

However, I do see why maxing out a 401(k) could make sense for behavioral reasons. The analysis above assumes that you can buy and hold assets in your taxable account for decades without touching the money. That’s easy in theory, but difficult in practice.

If you are someone who finds it hard to manage their own money, then the automation and illiquidity provided by a 401(k) could be a financial lifesaver. You won’t find these benefits in a spreadsheet, but they definitely matter.

Either way, the choice is yours. For some of you, maxing will be a great decision that will set up a comfortable retirement. For others, it could be locking up too much of your capital too soon in life. In the end, you have to make your own financial decisions. I just want to provide a useful framework for when you do.

Happy investing and thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 210. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data