One of the most common questions I get asked by readers is: Should I max out my 401(k) earlier in the year or just contribute normally to max it out by year end?

Though I am not the biggest fan of maxing out your 401(k), especially for young, aggressive savers, there is some evidence that maxing out earlier in the year can provide some benefit over maxing out by year end. Why is this true?

Because markets tend to go up. And since markets tend to go up, there is a slight advantage to getting your money into the market sooner rather than later. Of course, over a one year period, the difference between doing all your contributions in January (“Max Early”) and doing contributions throughout the year (“Average-In”) will be quite small, even when investing in a 100% U.S. stock portfolio.

In fact, since 1978 (when the 401k was first introduced), the biggest difference between maxing early and averaging-in to a 100% U.S. stock portfolio over one year was about 13%-15%. This means that, for a $20,000 contribution, choosing one strategy over the other could have netted you as much as $2,000-$3,000. But, that’s only in the most extreme years.

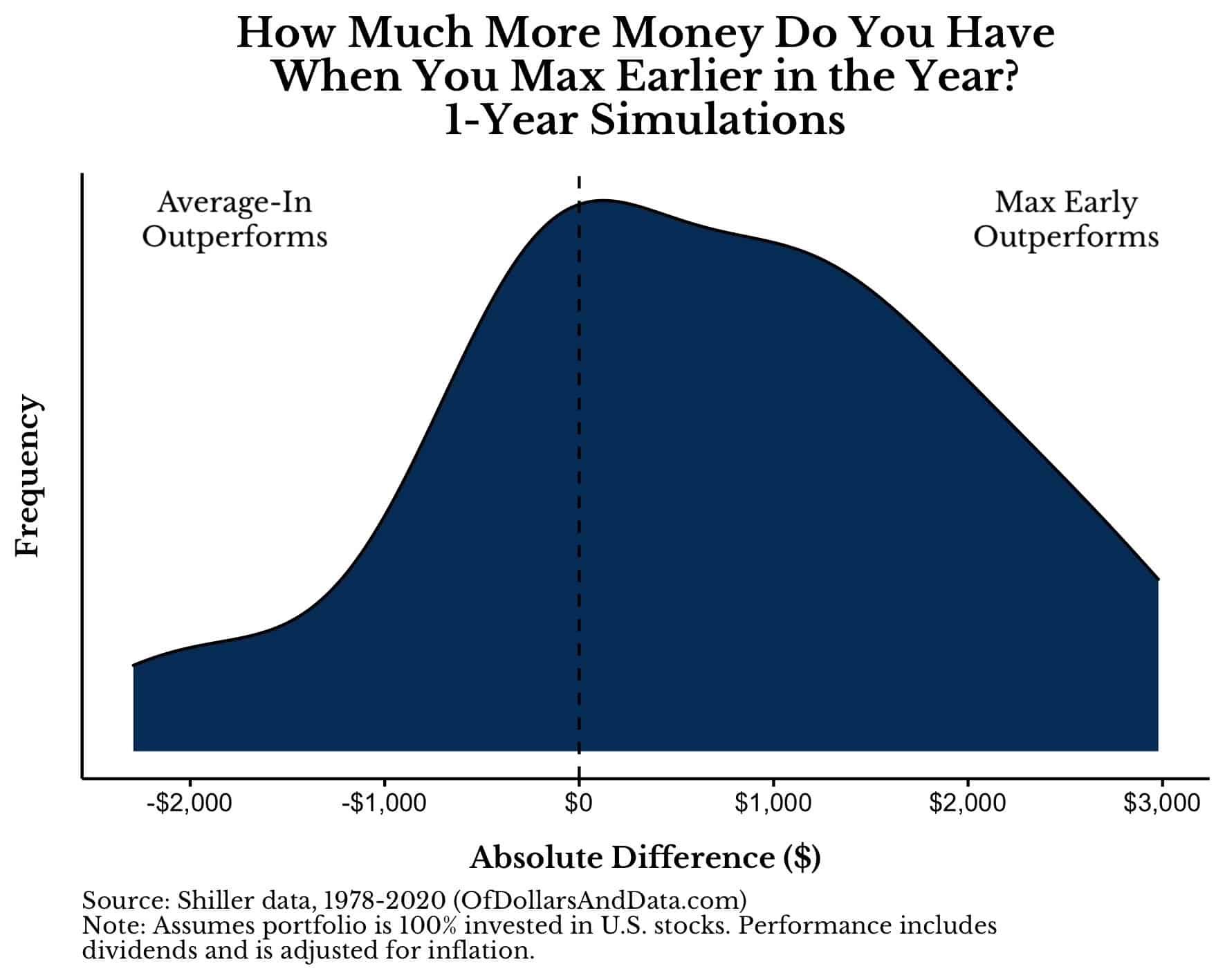

Typically, the amount of outperformance you get by following one of these strategies for a year is under $1,000 or about 5% of total contributions. If you were to look at the distribution of how much Max Early outperforms Average-In over each 1-year period since 1978, you can see this more clearly:

As you can see, this distribution is somewhat symmetrical, meaning that in some years Max Early outperforms and in some years Average-In outperforms. You can see this if you look at the dashed $0 line in the plot above.

The $0 line can be thought of as the dividing line between which strategy performs better. And since there is more mass on the right side of the $0 line, it implies that Max Early has a slight edge over Average-In across all 1-year periods since 1978. To be more precise, the Max Early strategy outperforms by $700 in a typical year.

Long story short: if you are deciding whether to max out your 401(k) early for just one year, it doesn’t really matter what you do. Yes, statistically maxing early should provide a slight advantage, but that advantage isn’t all that big in the grand scheme of things. So when does maxing your 401(k) earlier in the year actually matter?

When Does Maxing Out Your 401(k) Early Actually Matter?

Maxing out your 401(k) earlier in the year can make a bigger difference if you do it for multiple years in a row. Though one year won’t make a difference to your financial plan, the data suggests that doing this for many years can have a sizable impact.

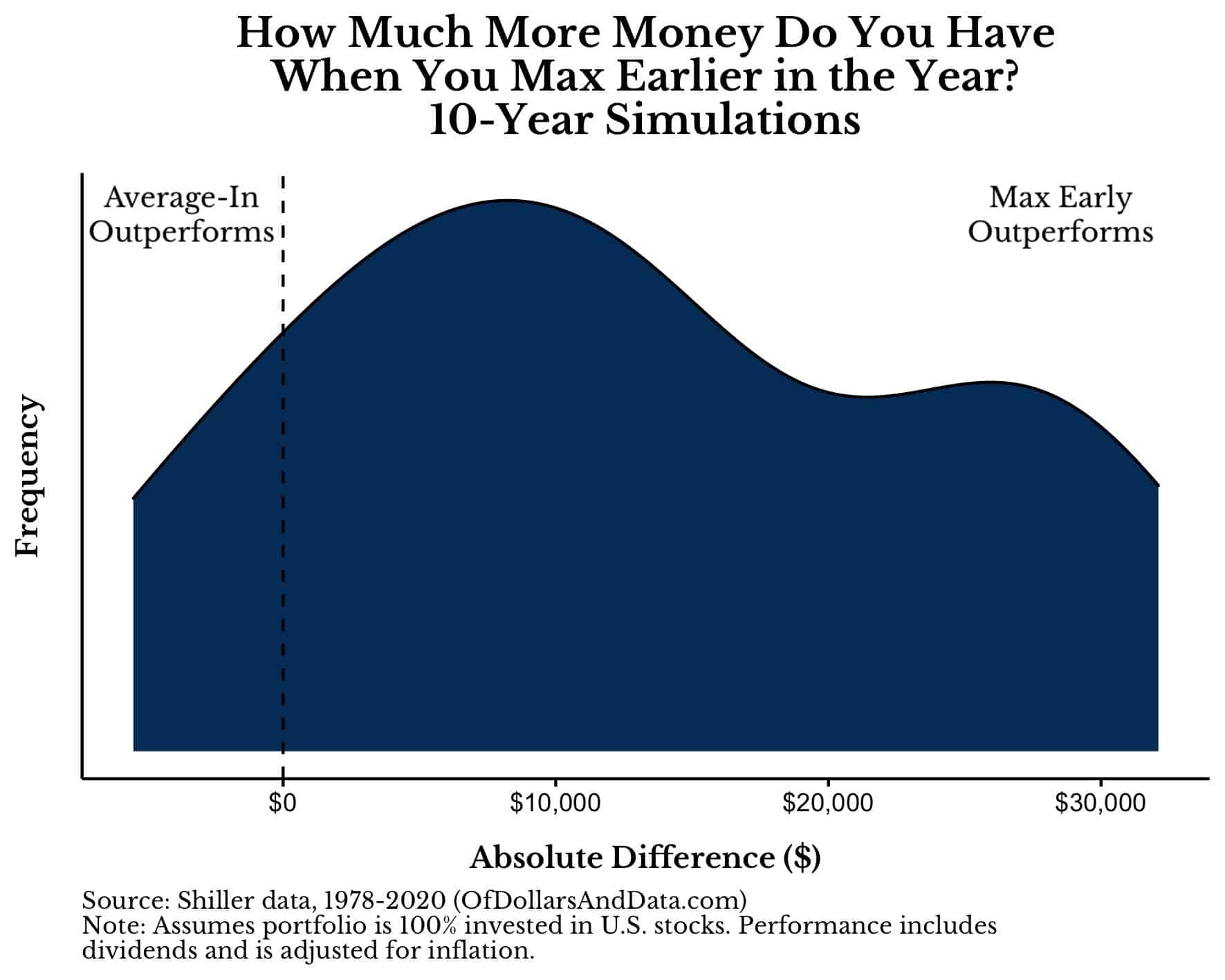

For example, imagine we compare the Max Early strategy and the Average-In strategy for 10 years in a row. So each year (for 10 years) Max Early would contribute $20,000 in January while Average-In contributed $1,667 each month for 12 months.

After running this simulation and comparing the performance between these two strategies for each 10-year period since 1978, there is a clear winner:

As you can see, over a 10-year time frame Max Early really pays off. In absolute terms, the typical performance difference is $11,500 in favor of Max Early or about 4%-5% of total contributions. In the grand scheme of things, this still isn’t a ton of money, but it’s not negligible either.

After examining both the 10-year simulations and the 1-year simulations, a pattern emerges—the typical outperformance of Max Early over Average-In is about 5% of total contributions. This is a rough approximation of what you should expect if you follow this strategy for any number of years.

So, if you were to max out your 401(k) earlier in the year for 20 years (at an annual contribution of $20,000), you should expect to have about 5% more than if you didn’t max early. On $400,000 in contributions (over 20 years) that means an extra $20,000. I ran the numbers as a sanity check and the median outperformance of Max Early for every 20-year period since 1978 was $22,000 (a little above 5% of total contributions).

While it’s nice that the empirical evidence matches the theory, we haven’t addressed the elephant in the room—is this strategy even feasible?

Is Maxing Out Your 401(k) Earlier in the Year Feasible?

While maxing out your 401(k) earlier in the year could provide you with some benefit, the number of households that could do this with ease is quite small. Why? Because to max out your 401(k) in the first month of the year would require $20,500 in contributions over 2 paychecks. That means that this strategy is limited to someone making at least $240,000 a year.

Of course, if you make less than this, you could still max out over the first two to three months of the year, but the benefit would be smaller than the 5% highlighted above. Nevertheless, just because this strategy isn’t feasible for most people with a 401(k), this doesn’t imply that it isn’t feasible for other retirement accounts.

For example, if you were to max out your Roth IRA by contributing $6,000 in January instead of throughout the year, your expected benefit would be about $300 (5% of $6,000) in a typical year. Yes, $300 isn’t a lot, but do that every year and it can add up over time.

Whether or not you choose to max out one of your retirement accounts earlier in the year is up to you. Though I don’t see a huge benefit to doing so, if you are someone who needs every extra dollar you can get, then maxing early should help.

This is especially true if you max out early over many years in a row. As the charts above illustrate, the longer you follow the Max Early strategy, the higher the likelihood of absolute outperformance.

[Author’s note: I’ve had a lot of people comment that many 401(k) plans will NOT match your contributions throughout the rest of the year (i.e. no true-up provision) if you decide to max early. If this is the case, then you will probably lose more money by not getting your full match then what you gain by being in the market earlier in time. Ask your employer before maxing early as this could end up costing you more money than it makes you.]

Either way, don’t stress yourself out over this decision. The benefit of doing so isn’t worth the mental cost. With that being said, happy investing and thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 278. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data