In the world of personal finance, we are constantly bombarded with messages about the “one thing” that could significantly improve our financial lives. Whether it be a particular kind of investment, a novel mindset, or the latest money-saving technique, there’s no shortage of ideas on how to get ahead.

Unfortunately, while many of these ideas are great in theory, they tend to not measure up in practice. These are what I refer to as the most overrated things in personal finance. So, if you’re interested in separating what truly matters from what doesn’t, then this is the blog post for you.

To start, let’s examine why early retirement isn’t always the dream it’s made out to be.

Early Retirement

Early retirement. No bosses. No meetings. No more work, ever. What’s not to like?

Though early retirement might seem attractive at first glance, unfortunately, there are a few key downsides that are commonly overlooked:

- Lost Sense of Purpose. While some people can enter early retirement without skipping a beat, many individuals who decide to retire early from the workforce soon realize that working is about far more than money. As Kevin O’Leary, aka Mr. Wonderful from Shark Tank, stated about retirement after selling his first company at 36:

“I retired for three years. I was bored out of my mind. Working is not just about money. People don’t understand this very often until they stop working.

Work defines who you are. It provides a place where you are social with people. It gives you interaction with people all day long in an interesting way. It even helps you live longer and is very, very good for brain health… So when am I retiring? Never. Never.”

Ernie Zelinski echoed a similar sentiment about the importance of work in How to Retire Happy, Wild, and Free:

“Regardless of how talented you are and how successful you are in the workplace, there is some danger that you will not be as happy and satisfied as you hope to be in retirement…What may be missing is a sense of purpose and some meaning to your life. Put another way, you will want to keep growing as an individual instead of remaining stagnant.”

So, unless you can find a way to keep a sense of purpose during retirement, you may want to re-think your approach before you put in your final two weeks’ notice.

- Increased Reliance on Market Returns. While retirees, in general, must hope for good future market returns to make it successfully through retirement, this is even more true for those who retire early. As I discussed a few weeks ago, the 4% rule doesn’t have a 100% success rate over longer time periods (i.e. 60 years). This means that anyone who does decide to leave the workforce early will need to hope that they don’t get an unlucky series of returns during their half century (or more) retirement. The counter argument to this is that younger retirees may be more able to re-enter the workforce if the going gets tough. I agree, but then it kind of defeats the purpose of early retirement, doesn’t it?

- Fear Surrounding the Future. The last issue I have with early retirement is that you have placed even more emphasis on the future going according to plan. You can stay in early retirement if you don’t get very sick. You can stay in early retirement if there isn’t another Great Depression. And so on and so forth. Unfortunately, life rarely goes to plan. While you could still get sick or experience another Great Depression while in the workforce, at least you would have a career and additional assets to fall back on. That won’t necessarily be true if you decide to retire early. Jared Dillian summarized it perfectly in his recent post on the FIRE movement:

Retiring at age 35 sounds interesting in principle, but it in practice, it would be hell. Imagine being completely idle and have nothing to do except worry about your small pile of money turning to dust.

When you combine the increased fear with the reduced sense of purpose, early retirement is a lot less promising than it initially seems.

Lastly, I just wanted to note that I take issue with early retirement not financial independence. Financial independence is a worthy goal that everyone should strive for, if they can. Unfortunately, some people get confused and think I am attacking financial independence anytime I discuss early retirement. The FIRE movement has done a great job of making these two distinct topics seem one and the same, but they are not.

Now that we’ve looked at why early retirement may not be all it’s cracked up to be, let’s discuss why investment properties aren’t always worth the hassle.

Investment Properties

Nothing says passive income like an investment property. Buy the property, find tenants, and watch the checks roll in. How much easier could it get? While the allure of owning a host of investment properties sounds appealing, there are a few key reasons why you might want to reconsider:

- High Entry Costs. Owning investment properties requires a significant amount of capital to do it successfully. Not only do you have to cover the downpayment (typically 20%), but you’ll also have to cover other closing costs and potential renovations for the property. In addition to the money that you’ll spend, you’ll need to know how to buy, rent, and manage these properties. These financial and educational entry costs are quite high relative to other asset classes where you can still earn a decent return for much less time and effort.

- More importantly, with interest rates exceeding 6% today, the cost of buying an investment property (using financing) has gone up. This means that a lot more has to go right today than if you had bought when rates were closer to 3%.

- Tenant Issues. Assuming you have the money and some idea of what you were doing, you would still need to deal with finding and managing tenant issues. Properties depreciate and you will need to deal with the ongoing costs of servicing them and possibly dealing with tenants who don’t want to pay or who refuse to vacate your property. Depending on which state you’re in, dealing with evictions can become quite expensive and time-consuming. If you don’t enjoy human conflict, then being in the rental business may not be right for you.

- Hard to Find a Good Property Manager. If you don’t like dealing with tenants, then your solution is to find a property manager to do it for you. However, finding a good property manager could be as difficult as managing the property yourself. Though I’ve never personally had to hire a property manager, my understanding from my research on the topic is that it’s hard to find a good one. Just consider this extensive Reddit post on the topic in the RealEstateInvesting subreddit. It’s a chore. And, trust me, you will need to find a good one. Robert Kiyosaki, famed real estate investor and author, said as much in Rich Dad, Poor Dad:

A great property manager is key to success in real estate. Finding a good manager is more important to me than the real estate.

So, unless you have the time to either manage the properties yourself or become an expert in identifying the best managers, you shouldn’t even start.

- Concentration Risk. Lastly, one of the biggest issues with owning investment properties is concentration risk. Whether you own a few investment properties in different areas or a lot of properties in the same area, your finances will be overly exposed to those local markets. Unlike owning a Real Estate Investment Trust (REIT), which is typically already diversified, having a few investment properties increases your concentration risk in those regions.

Owning investment properties has lots of benefits, especially on the tax side (see the 1031 exchange). However, in order to reap these benefits you will need to deal with high entry costs, possible tenant issues, finding a good property manager, and concentration risk, among other things. If this list doesn’t intimidate you, then you might enjoy having an investment property. Otherwise, there are other ways to get expose (hint: REITs) without the headache.

Lastly, some real estate gurus will tell you that you almost never lose money in real estate. This simply isn’t true. While we might not hear about these stories as often (after all who wants to promote how they lost money), trust me they happen.

Now that we’ve discussed some of the downsides of investment properties, let’s look at why rebalancing may not be as important as you think.

Rebalancing Your Portfolio

I’ve changed my mind on the importance of rebalancing. Many years ago, I used to believe that you had to rebalance on some exact frequency otherwise you’d miss out on some “rebalancing bonus.” Unfortunately, after running the numbers on your typical stock/bond portfolio, I’ve realized that how often you rebalance matters less than you think.

Does this mean that you should never rebalance? No, I think rebalancing is good for reducing portfolio volatility and can be profitable during large market downturns. However, since large crashes of this kind are rare, rebalancing typically means reducing your portfolio’s return since you end up selling your fastest growing assets (typically stocks) to buy your slowest growing assets (typically bonds).

So what’s the right frequency? I’ve concluded that a good rebalancing frequency is anywhere from once every six months to once every three years. You want to rebalance often enough to keep your portfolio volatility in check, but not so often that you end up overly reducing your exposure to your fastest growing assets. Anywhere in this time frame is fine, but you do want to rebalance at some point.

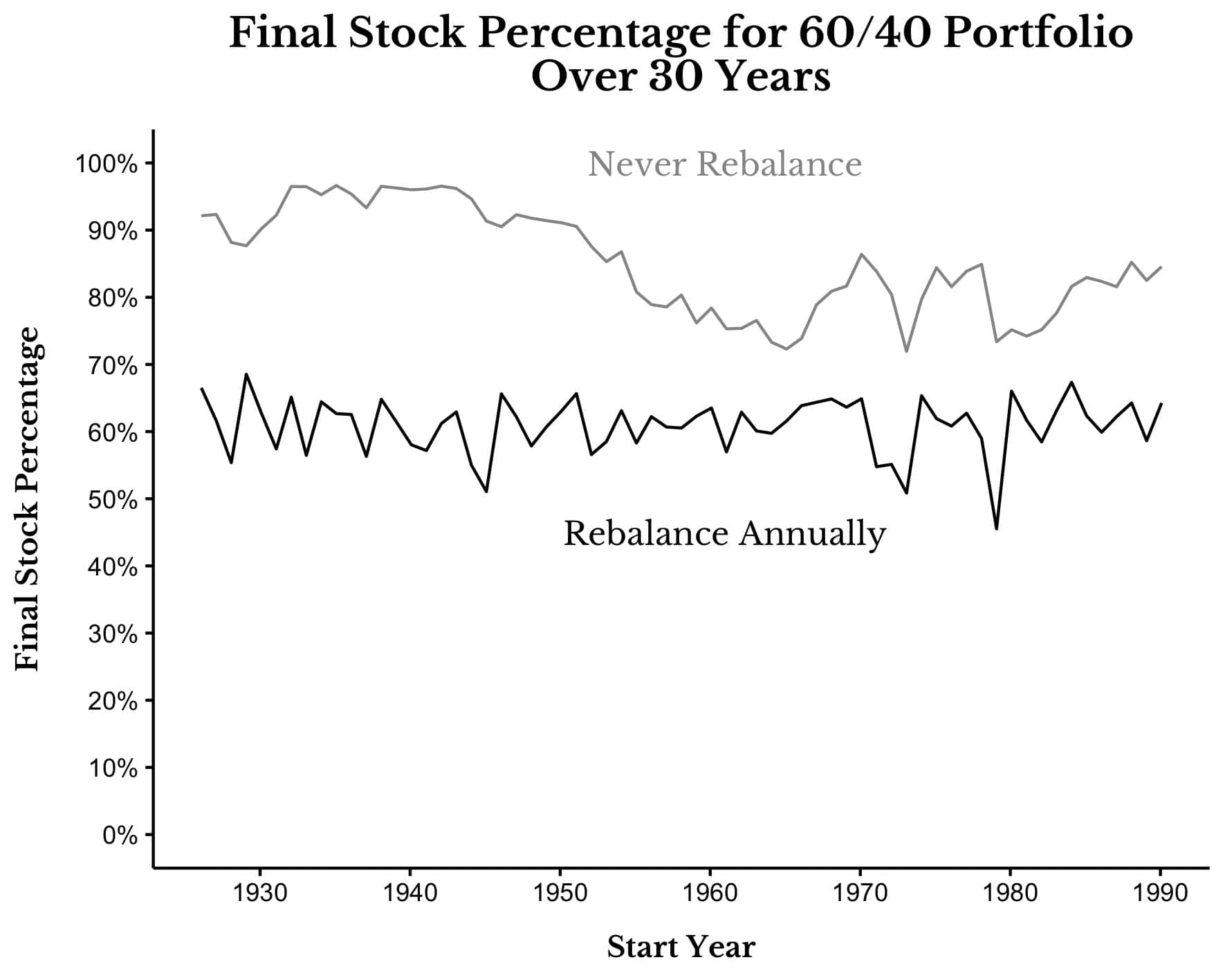

If you never rebalanced, your fastest growing assets would come to dominate your portfolio. As I illustrated in Just Keep Buying, if you never rebalanced a 60/40 portfolio, your 60% stocks would end up being 80% (or more) stocks within a few decades. The chart below shows the final stock percentage in a 60/40 portfolio after 30 years when you rebalance annually versus never rebalance:

As you can see, if you want to keep your portfolio’s volatility relatively consistent, you need to rebalance.

Of course, rebalancing like this (aka selling down an overweight asset to buy an underweight asset) can have tax consequences if you do this in a taxable account where you have capital gains. This is why my preferred method of rebalancing is called an accumulation rebalance—I periodically buy more of the underweight assets in my portfolio to bring them back to their target allocation.

For example, imagine I had an 80/20 U.S. stock/U.S. bond portfolio. After a year let’s say the portfolio is 85% stock/15% bond. Instead of selling down 5% of my stocks to buy 5% more bonds, I would take my regular savings (that I was going to invest anyways) and put it solely into bonds to move my allocation back toward 80/20.

By doing this, I can keep my allocation roughly in check without ever having to sell anything in my portfolio. It’s the best of both worlds. While this method is great for accumulators (those still working and saving money), this method may be more difficult for those retirees who can’t keep buying.

Lastly, the rebalancing I am referring to here is mostly for stock/bond portfolios. Technically, if you can find a bunch of high return assets with low correlations with one another, then rebalancing can have even more benefits. Unfortunately, since these assets are difficult to find (and invest in) for retail investors, I tend to focus on the rebalancing situations retail investors are most likely to face (aka stock/bond rebalancing).

Either way, I personally plan on using an accumulation rebalance strategy going forward and I hope to never think about this topic ever again.

Now that we’ve looked at some areas that are overrated in the personal finance space, let’s cover a few that aren’t.

What’s Not Overrated?

Though there are many topics in personal finance where the benefits may be overstated, here are a few areas where I believe the opposite is true:

- Knowing history. Of all things I’ve done as an investor, having some idea of history, and, in particular, market history has made a huge difference in how I behave financially. Once you realize that “history doesn’t repeat, but it rhymes” then it becomes much easier to stay calm when the going gets tough. I’ve had to rely on this many times before when the world felt like it was going to end. The more you know, the better equipped you will be to deal with whatever the world throws at you. Of course, I’m a financial blogger who believes in the power of financial education, so I may be a bit biased.

- Diversification. While diversification definitely has its downsides, on the whole the benefits are far, far greater. Diversification allows us to preserve capital so it can continue to work for us year after year. Though some may argue that you should “concentrate to get rich, diversify to stay rich,” this is only true if your concentrated position works out. Go tell the employees of Enron (who had their life savings in the company) “concentration to get rich” and see what they tell you. The fact is that you can get quite wealthy with diversification, it just might take a little longer. Ultimately, diversification is about survival and there are few things better in investing than that. As the famous saying goes, “There are old pilots and there are bold pilots, but there are no old, bold pilots.”

- Raising your income. I’ve probably written on the importance of raising your income more than any other topic, and for good reason. Income is the foundational pillar upon which most wealth is built. Income is how you create a wedge between your earnings and your expenses so that you can save money. This is why income is more correlated with savings rate than any other measure I’ve seen. So, if you want to increase your ability to build wealth, increase your income and then save the difference. This is easier said than done, but I promise that this is the path you should be taking.

While you may not fully support my assessment of what financial ideas are under/overrated, we can all agree that, periodically, some financial trends become overhyped. When this happens, your best defense is to stick to your plan and focus on what truly matters. How you earn money, how you manage risk, and how you react to markets will be far more important than whatever “new thing” pops up in our financial lives.

Until next time, thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 384. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data