Imagine you are a participant in a large race. However, unlike an ordinary race, this race never ends, participants come and go every day, and no one starts the race at the same spot. This might seem like an odd kind of race to participate in, but you (like everyone else) don’t have a choice in the matter.

The “race” I am talking about is wealth accumulation in the United States. In this race, you can think of your position (relative to others) as your current wealth and your speed as your current income.

Today, the United States is going through a period where a small group of racers is far ahead of everyone else (i.e. wealth inequality).

Historically, the U.S. has dealt with inequality by progressively taxing income. Those with higher incomes are taxed at a higher rate than those with lower incomes.

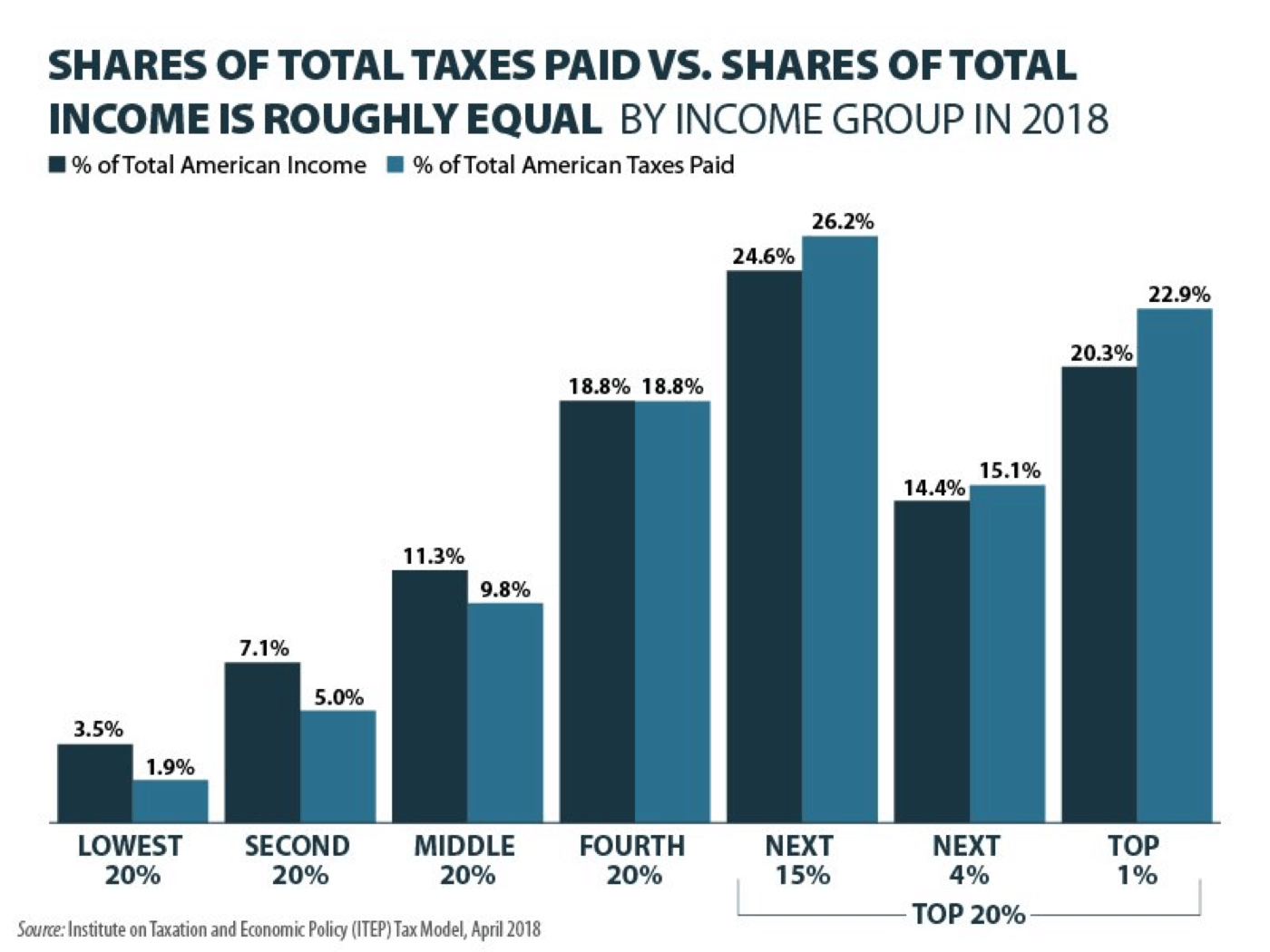

Using the racing analogy, the IRS tries to slow down the fastest racers. If you look at the share of total taxes paid versus the share of total income earned in 2018, you will see that the IRS is achieving this goal to some extent:

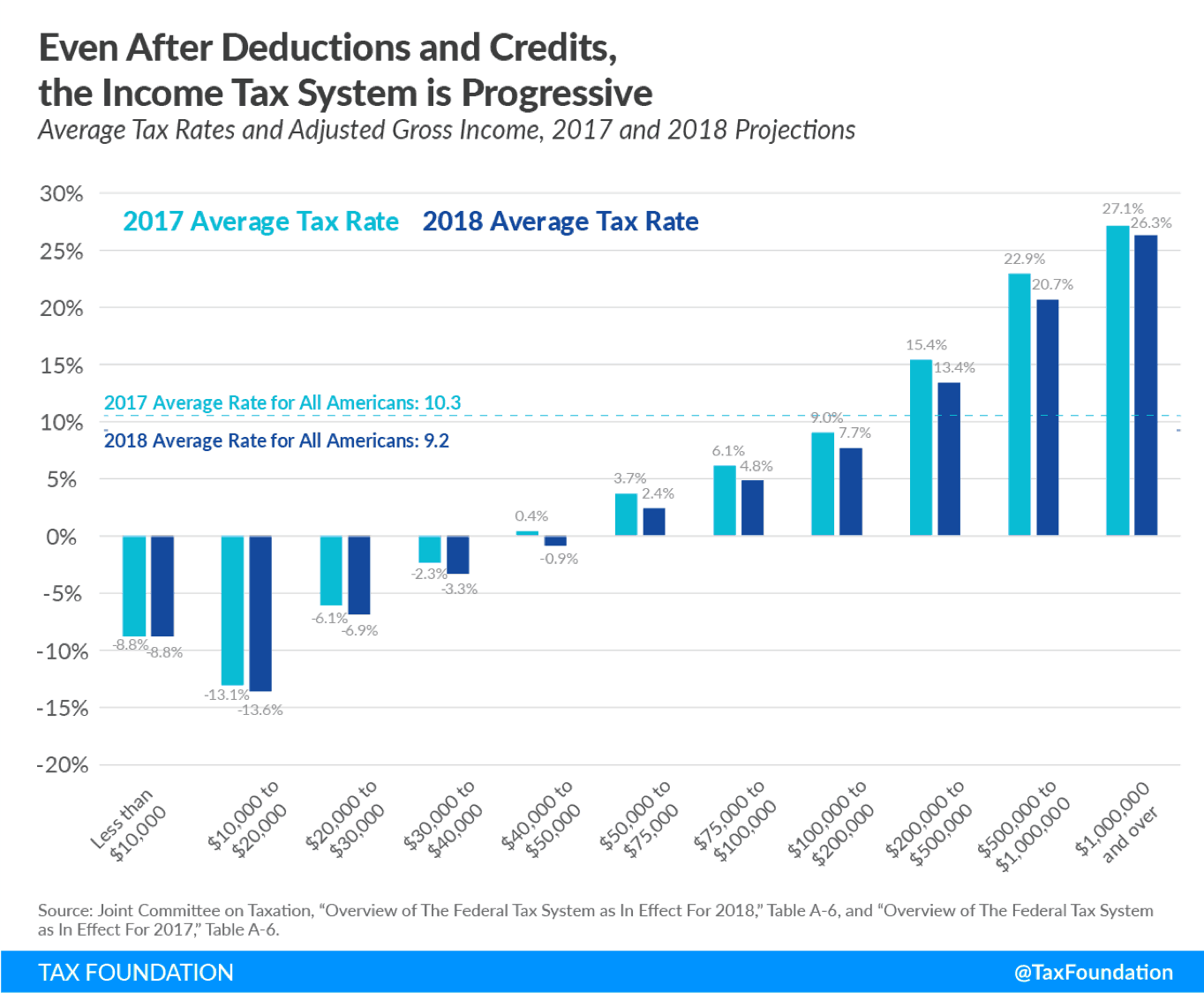

And when you include deductions and credits, the U.S. income tax system looks even more progressive:

However, there is a new kind of thinking in town. Rather than slowing down the fastest racers, the new thinking suggests that we should take those racers that are the furthest ahead of everyone else and pull them back in the race. Enter the wealth tax.

The wealth tax has gotten lots of attention recently after Bernie Sanders came out with a policy proposal to “Tax Extreme Wealth.” Like Senator Elizabeth Warren’s “Ultra-Millionaire Tax” plan, Bernie’s proposal would progressively tax larger fortunes at higher rates.

Bernie’s plan has the following marginal tax rates for married individuals (the brackets would be cut in half for single filers):

- 1% on all wealth greater than $32 million

- 2% on all wealth greater than $50 million

- 3% on all wealth greater than $250 million

- 4% on all wealth greater than $500 million

- 5% on all wealth greater than $1 billion

- 6% on all wealth greater than $2.5 billion

- 7% on all wealth greater than $5 billion

- 8% on all wealth greater than $10 billion

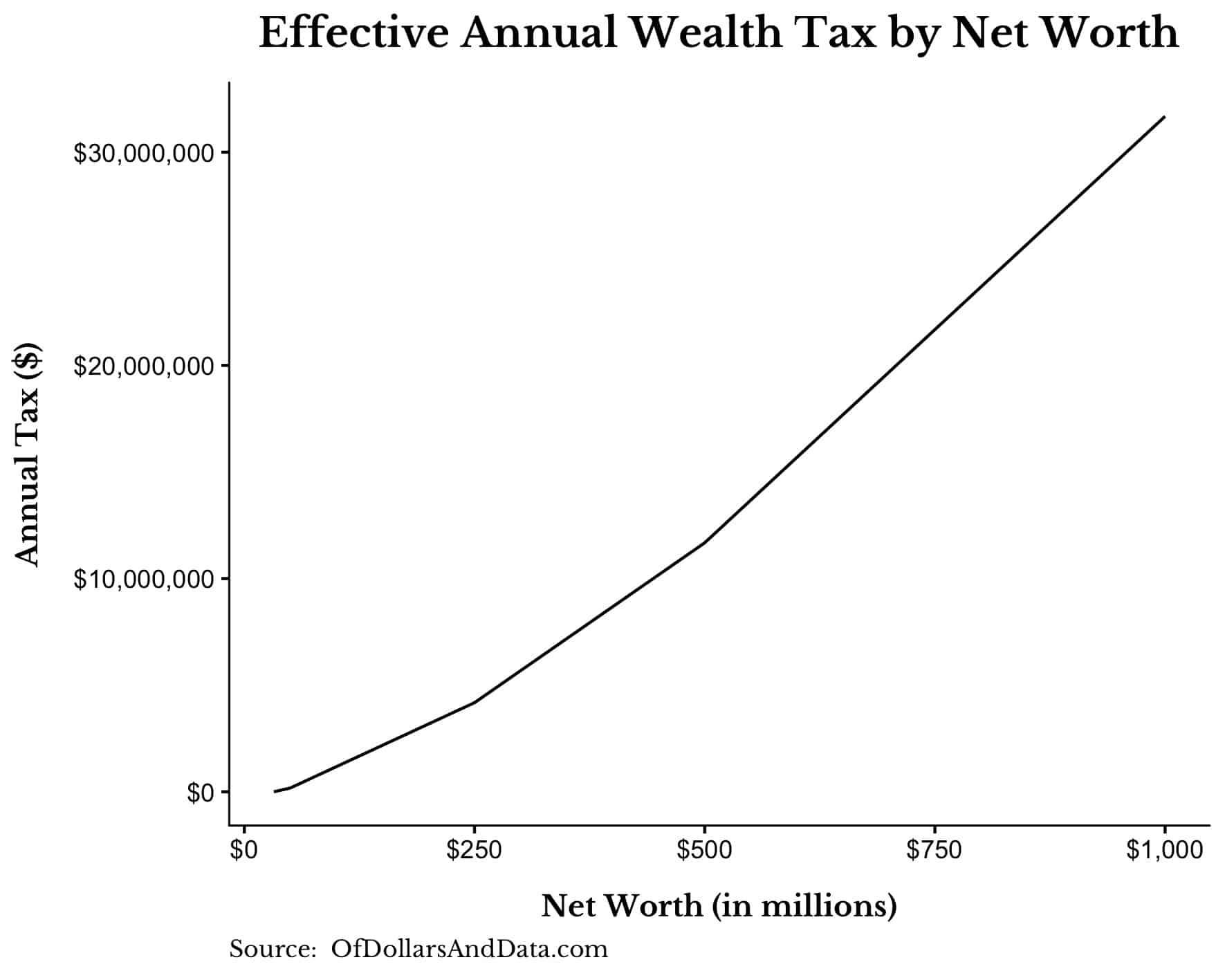

So, a couple with $32.5 million would have to pay an annual tax of $5,000 [($32.5 million – $32 million) * 1%] while a couple with $1 billion would have to pay close to $32 million annually.

Visually, the effective annual wealth tax due (for those households worth up to $1 billion) would look like this:

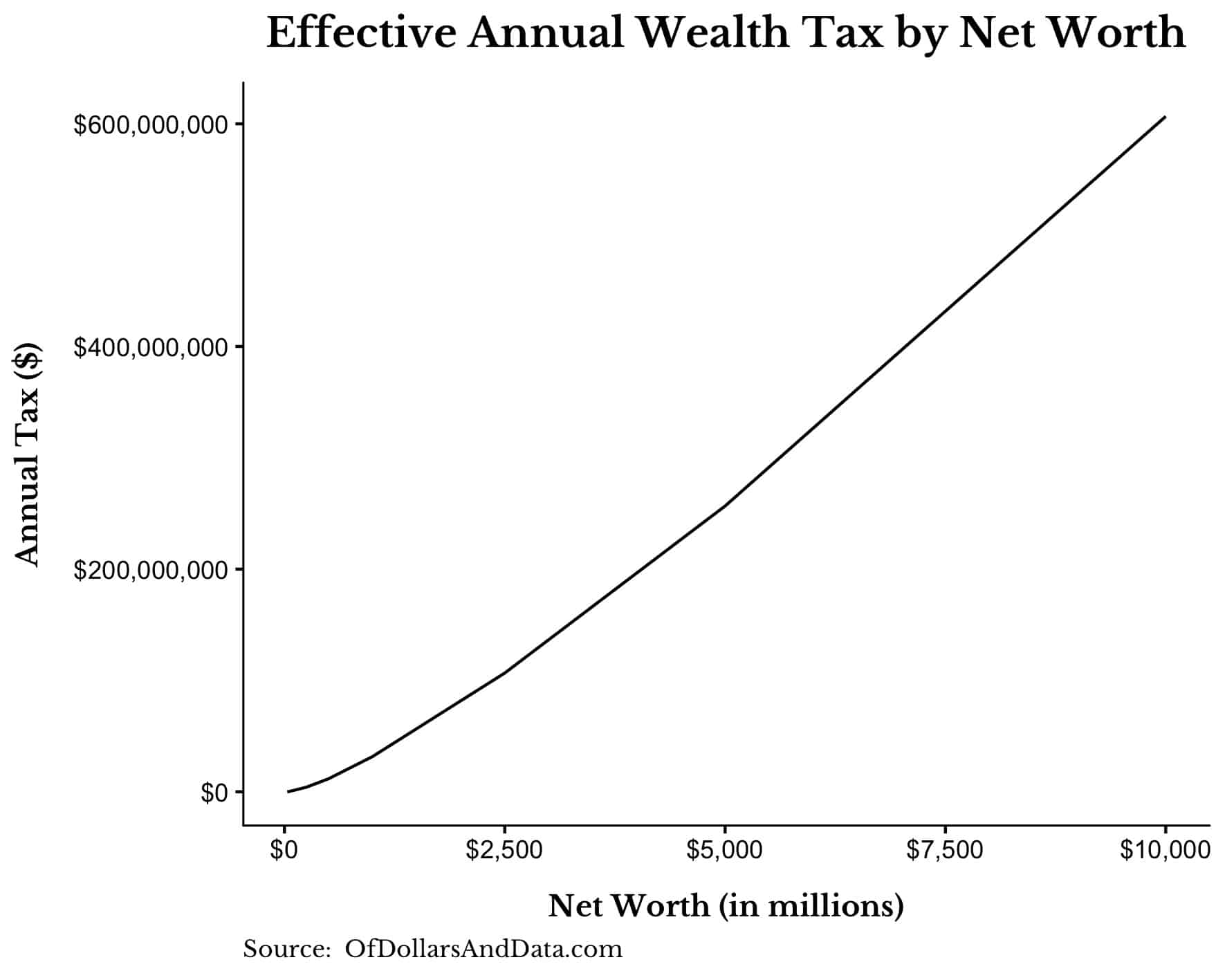

As we increase a household’s net worth up to $10 billion (the largest bracket mentioned in Bernie’s plan) the effective annual tax due would be:

As you can see, a wealth tax would raise a lot of money (in theory) and would raise it from those individuals that have seen the largest wealth gains in the last half century.

This is one of the benefits of a wealth tax over an income tax—it taxes those who already have wealth versus those who are currently trying to earn wealth.

For example, it’s easy for someone like Warren Buffett to say, “Raise my incomes taxes,” because he is already rich. He has won the race and is essentially asking to slow down other participants from catching up to him.

However, a wealth tax changes the position of the players, which is far more effective and, dare I say, fair to those people who are trying to get rich now.

Yet, there remain three major issues I see with implementing a wealth tax: measurement, evasion, and efficacy.

What is it worth now?

My biggest issue with a wealth tax is how difficult it would be to accurately measure and assess a tax on someone’s net worth fairly and predictably. For example, how do you value something with few comparable assets?

Or, what do you do when you owe wealth taxes on an asset that has decline significantly in value?

If someone owned WeWork when it was valued at $47 billion, would it be fair for them to pay $3.6 billion in taxes when WeWork is now valued at $10 billion? And how do you value assets with extreme volatility?

For example, what is the value of Bitcoin for tax year 2017 in the year 2018?

Though Bernie’s proposal doesn’t perfectly answer these questions, it does provide the following guidance:

For assets that are difficult to appraise, the Treasury Department would have the option of allowing taxpayers to have appraisals done periodically instead of annually. The Treasury Department would establish the average rates of appreciation for several classes of assets. Those appraised only every few years would be assumed to appreciate in the intervening years at the average rate established for their designated class.

This is a good start, but this entire line of questioning illustrates the difficulty of wealth taxes—wealth is hard to measure. While income is a knowable quantity, asset valuation is far more elusive.

If we want wealth taxes that work effectively, we will have to figure out a way to accurately answer the question, “What is it worth now?”

Why there are so “few” swimming pools in Greece

Let’s pretend that a wealth tax was passed in the United States. What would happen next? Would the ultra-wealthy just smile and pay the tax? Of course not.

Overnight an army of tax lawyers and consultants would begin pouring over the new law looking for loopholes and other ways to save money for their clients. Page after page would be dissected and analyzed until the impact of the new law was minimized.

And for those individuals where the tax burden was still too great, they might simply take their assets and leave the country. Of course you can impose penalties for those that try to leave, but think about what message this sends to those considering bringing their assets to America from other countries?

Evasion is a central problem for taxation authorities across the globe. As Josh Brown recently pointed out, “Only 324 people in Athens paid the “swimming pool tax” in 2010. There were 16,974 swimming pools that year.”

So before we can determine whether a wealth tax would “raise an estimated $4.35 trillion over the next decade,” we have to consider the likelihood and cost of evasion.

Can the U.S. eradicate polio?

I recently saw Inside Bill’s Brain, the Bill Gates documentary on Netflix, and was astounded by the size of the challenges that Bill and Melinda are taking on with their foundation. Eradicating polio, inventing ultra-cheap toilets, and creating safe nuclear energy are not easy problems to solve.

However, Bill and Melinda have a chance of solving them because of the immense wealth that they have accumulated since Bill founded Microsoft.

Naturally, this leads to a question surrounding the implementation of a wealth tax: Can the United States government use Bill Gates’ money as efficiently as Bill Gates?

Given the amount of scientific and technological breakthroughs that the U.S. government has been responsible for historically, I cannot answer this question with a definitive “Yes” or “No.” However, it is a question we need to ask when considering how a wealth tax would affect private philanthropy.

For example, in 2017 Americans gave over $400 billion to charitable causes with the largest growth in contributions coming from foundations created by major philanthropists (i.e. the ultra-rich). If a wealth tax were implemented, how large of a reduction would we see in private philanthropy and would this reduction be worth it?

What Does the Data Say?

While I am all for discussing the pros and cons of a wealth tax, we must also consider what the empirical results say for those countries that have actually tried to implement a wealth tax. Fortunately, an article from NPR did just this:

In 1990, twelve countries in Europe had a wealth tax. Today, there are only three: Norway, Spain, and Switzerland. According to reports by the OECD and others, there were some clear themes with the policy: it was expensive to administer, it was hard on people with lots of assets but little cash, it distorted saving and investment decisions, it pushed the rich and their money out of the taxing countries—and, perhaps worst of all, it didn’t raise much revenue.

The results of these wealth tax experiments in Europe suggest that wealth taxes have limited effectiveness, but Elizabeth Warren argues that those wealth taxes had too many exemptions, allowed for easy capital flight, and were imposed on people who weren’t rich enough.

All of Warren’s arguments might be true, but I am still not convinced that wealth taxes will have their intended effect. First Congress creates taxes, then the ultra-wealthy try to avoid them. It’s a financial arms race that will never end.

Big thanks to Bill Sweet for discussing this issue with me during March for the Fallen. I could not have written this post without him. Lastly, thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 144. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data