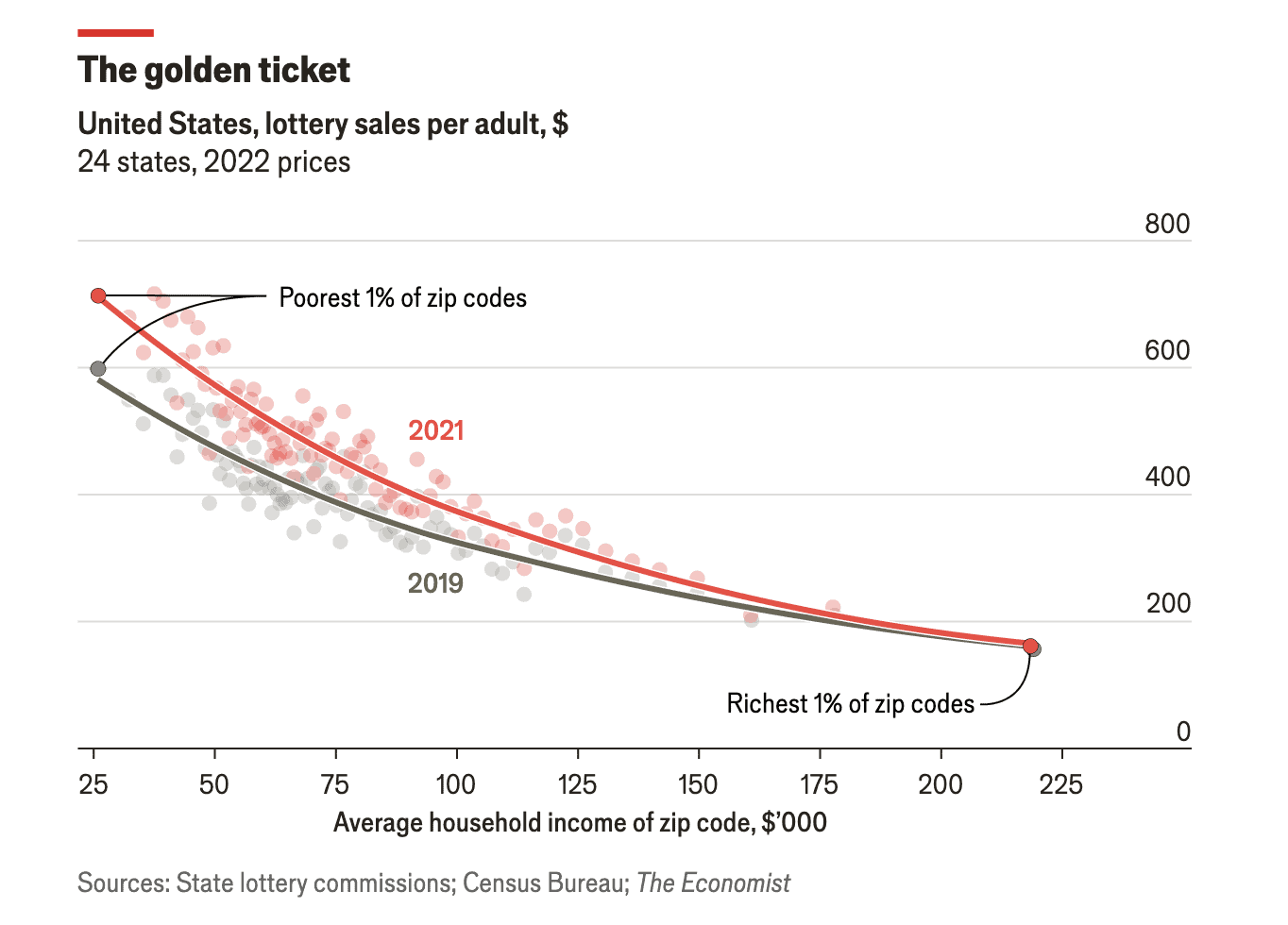

Recently, the Economist published an article on the economics of American lotteries. In it they found that, if Amercia’s lotteries were a single company, they “would be the ninth-most profitable in the country.” Unfortunately, the bulk of these profits come from some of the poorest people in the United States. As the article states:

In the poorest 1% of zip codes that have lottery retailers, the average American adult spends around $600 a year, or nearly 5% of their income, on tickets. That compares with just $150, or 0.15%, for those in the richest 1% of zip codes. In other words, the poorest households spend roughly 30 times more on lotteries than richer ones, as a share of income.

Historically, I used to think playing the lottery was “stupid” and would often poke fun at people who bought tickets. For example, below are a few of my favorite lottery memes I used to tweet out whenever the Powerball jackpot got high enough:

Historically, I used to think playing the lottery was “stupid” and would often poke fun at people who bought tickets. For example, below are a few of my favorite lottery memes I used to tweet out whenever the Powerball jackpot got high enough:

While I still find humor in these images, I’ve had a change of heart when it comes to how I view those who play the lottery.

My problem was that I was too hyper-rational on the issue. After all, if your chance of winning the lottery basically rounds to zero, why would you play? My belief was that you would be far better off by saving and investing that money instead of spending it on lottery tickets. And, if the typical person who bought lottery tickets followed my advice, they would dramatically improve their financial life.

Unfortunately, my theory was wrong. After running the numbers, I’ve come to realize that foregoing lottery tickets isn’t enough to move the needle for the average American. I can prove it too.

Using the data from the Economist article, we know that the average American living in the poorest 1% of zip codes spends $600 a year, or $50 per month, on lottery tickets. Assuming they bought tickets for 30 years, their total lottery spending would’ve been $18,000. If they had saved that money in cash instead, this means they could’ve had an extra $50 per month for 30 years in retirement. Every foregone lottery ticket is extra spending later.

But that’s the lower bound of what they gave up because they didn’t invest their money. What if they had invested that $50 per month and earned 4% per year (after inflation) instead? In that case, they would’ve ended up with around $35,000 or nearly double the $18,000 they would’ve spent on lottery tickets.

Unfortunately, here’s the bad part—that extra $35,000, if invested at 4% per year, would only generate about $165 per month in additional retirement income. This isn’t nothing, but it’s also not going to dramatically alter their lifestyle. Considering that people in the poorest 1% of zip codes earn about $12,000 per year, an extra $165 per month (or ~$2,000 per year) only equates to a 17% raise in their income (all else equal). And while a 17% raise is nice, it’s not going to change their retirement in any big way.

But you know what would change their financial situation in a big way? Winning the lottery. There’s no debate there. Though the chance of winning is very, very slim, there is at least a chance of a dramatically different financial life. Sacrificing the weekly lottery tickets doesn’t provide that.

This reminds me of the [since deleted] blog post titled Why I Make Terrible Decisions, or, Poverty Thoughts:

I make a lot of poor financial decisions. None of them matter, in the long term. I will never not be poor, so what does it matter if I don’t pay a thing and a half this week instead of just one thing? It’s not like the sacrifice will result in improved circumstances; the thing holding me back isn’t that I blow five bucks at Wendy’s. It’s that now that I have proven that I am a Poor Person that is all that I am or ever will be. It is not worth it to me to live a bleak life devoid of small pleasures so that one day I can make a single large purchase. I will never have large pleasures to hold on to.

From this perspective you can see why some people make seemingly “bad” financial decisions. Because it’s either one of their few joys in life or one of the easiest ways for them to get ahead financially. This explains why financial nihilism has taken off across the U.S. When the cost of living is rising and you feel like you can’t get ahead, sports betting, crypto, and lottery tickets don’t seem like such bad ideas.

But for someone who has their financial life together, such investments can seem downright foolish. For example, imagine a millionaire putting $1,000 into some random altcoin that goes up 100x in a month. How much does that change the millionaire’s lifestyle? Very little. But take someone with only $5,000 to their name and give them a 100x return on a $1,000 investment and their life is transformed.

This single insight explains a lot of the seemingly irrational behaviors we see in the financial world. Once you realize this, it will completely change your perspective on what makes a “good” or “bad” financial decision. Don’t get me wrong, there are people out there who take things too far and have some truly destructive financial behaviors. However, as the data suggests, this isn’t how the typical American behaves, even in the poorest parts of the U.S.

So before you rush to judge someone’s financial behaviors, consider the context a bit more. After all, there’s more to life than money, especially for poor people. Chris Arnade did a great job getting this point across in his book Dignity: Seeking Respect in Back Row America:

Most people didn’t ask for money, even the most desperate. Most just wanted to sit and talk with someone who wasn’t trying to save them, didn’t scold them, and didn’t judge them.

We could all use a little less judgement in our lives, especially around our financial decisions. Thank you for reading.

If you liked this post, consider signing up for my newsletter.

This is post 395. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data