A few weeks ago someone tweeted out a video of Coleman Hawkins’, the star forward for the Kansas State Wildcats, breaking down about the pressure that was placed on him during the basketball season. The tweet read:

i want to feel bad, but:

coleman hawkins made $2 mil in NIL this year. he’s 23. he’s set for life.

This started a firestorm on financial Twitter. Some people argued that $2M at 23 was clearly not enough to be “set for life”, while others claimed that it was. So, which is it?

The answer is…it depends. Unfortunately, financial debates like this are incredibly nuanced and are based on what kind of assumptions you make. As the saying goes, “The devil is in the details.”

That’s what this blog post is about. Under what circumstances could you be “set for life” with $2M at age 23, and under which circumstances would you not be. Let’s dig in.

How $2M at 23 Can Last a Lifetime

Imagine on your 23rd birthday you get handed a check for $2M. Congrats! In one moment you’ve earned what a typical American earns over their entire career. Does this mean that you can celebrate and never work again? Well, it depends.

If we assume that you had to pay taxes on your $2M check (as Coleman Hawkins did), then that would leave you with around $1.2M (60% of $2M). If you put that into a U.S. Treasury bill today (earning 4% per year) that would generate $4,000 a month in income (before taxes). After federal taxes (assuming a single filer with the standard deduction) you are looking at around $3,700 in post-tax income.

Assuming short-term rates stay at 4% forever, can you live the rest of your life off of $3,700 a month? Maybe if you moved abroad or lived in a low cost of living area in the U.S., it’s possible. That $3,700 would be enough to live on until you got older and inflation started to catch up with you. At that point you could then use the 4% Rule to actually withdraw money (e.g., 4% of $1.2M or $48,000 per year) until you died.

If you had $2M to start (instead of the $1.2M that Coleman Hawkins would’ve had), that would give you $5,800 a month in Treasury bill income. You could easily use this for a few decades and then switch to the 4% Rule later to keep pace with inflation. Once again, this assume a constant return of 4% on Treasuries and a very low cost of living in the U.S. or abroad.

Why can’t you use the 4% Rule out the gate at age 23? Because of sequence of return risk. If you get unlucky, your money won’t last your entire lifetime. Assuming a life expectancy of 78, your $2M has to last for 55 years. And, unfortunately, a diversified portfolio isn’t guaranteed to make it.

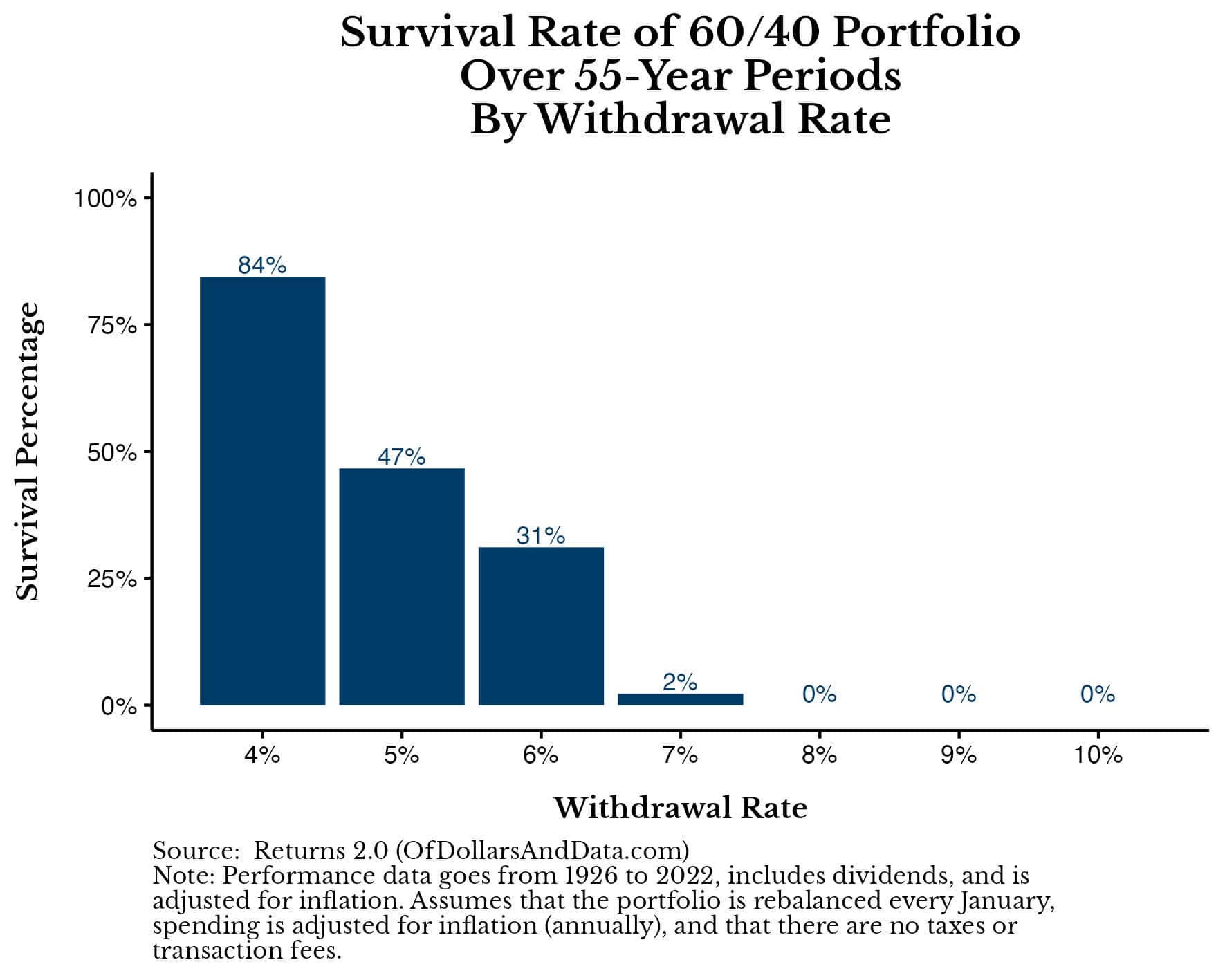

You can visualize this in the chart below showing the percentage of 55-year periods where you wouldn’t run out of money throughout U.S. history for a 60/40 (U.S. stock/U.S. bond) portfolio by withdrawal rate:

While a 4% withdrawal rate will very likely last 30 years, it only has an 84% chance of lasting for 55 years. And if you withdraw too much above 4%, you’ll go broke.

How do you improve your chances of making your money last 55 years? Take more risk.

If you had a 100% U.S. stock portfolio instead, historically, you would’ve had an 87% chance of making it over 55 years using the 4% Rule:

Additionally, you’d have a higher chance of withdrawing a bit more from your portfolio as well.

However, this wouldn’t guarantee success. For all those people saying, “If the market returns 10% per year, I should be able to pull out 7% per year without an issue,” Nope. You are dead wrong. There is a chance that you’d make it, but it’s less than a coin flip (38%).

This illustrates why $2M can only last a lifetime when your costs are quite low. But change any of these assumptions and the thought experiment breaks down. This is especially true when you include the impact of inflation over time.

Why $2M at 23 Probably Won’t Last a Lifetime

When thinking about whether $2M will last a lifetime, the biggest problem is inflation. In our prior example, our hypothetical 23 year old had anywhere from $3,700 to $5,800 a month to live off of for the rest of their life (via Treasury bill income). That might seem like a decent amount today, but in time it likely won’t be.

How do I know? Because let’s go back in time 55 years to 1970. Do you know how much $3,700 a month today was worth in 1970? Around $440. So imagine you started living off of $440 a month in 1970. It probably would’ve been nice. But the problem is that you had to keep living off of that amount.

Do you know anyone today that could live off of $440 a month without any other income or support? I don’t. Even if we assume that you earned $5,800 a month (using the $2M nest egg), that’s still only $690 a month back in 1970. While there are people that could survive on $700 a month today, it’s not an easy existence.

While there are ways to make $2M last a lifetime without working, you’d either have to be quite frugal or get a bit lucky. If your costs went up unexpectedly, markets went into a prolonged decline, or interest rates stayed too low for too long, you might not make it.

But, there’s been a problem with this thought experiment—we assume you never work again. And that isn’t completely realistic. While “set for life” might mean “never working again” for some, it doesn’t have to be. It could mean that you’ll have a much better life as a result. If that’s your definition of “set for life” then I couldn’t agree more.

Enough to Do Anything, But Not Nothing

We can run all the retirement simulations we want, but the truth is that having $2M (or even $1.2M) at age 23 would be life-changing for basically everyone. This amount of money would give you the freedom to do anything, but not necessarily nothing. I stole this line from Warren Buffett regarding his philosophy on giving money to children:

I want to give my kids just enough so that they would feel that they could do anything, but not so much that they would feel like doing nothing.

That’s what $2M at age 23 gets you. It unlocks the freedom for you to pursue whatever projects you want, assuming they generate some income down the line. This is essentially what Coast FIRE is and it’s my favorite FIRE philosophy.

But here’s the part that’s really going to trip you out. There are people out there who are worth more than $2M today that are working jobs they hate. And they are older than 23 too. All else equal, these people would need less money than our hypothetical 23 year-old to grant them the same level of career freedom (i.e., Coast FIRE). But, those older people probably don’t see it this way.

Having $2M at 23 seems like the ultimate form of career freedom, but having $2M at 45 doesn’t. But it’s exactly the opposite. The older person has less time to consume their resources, so they should have more career freedom, all else equal. Of course, if that 45 year-old has a family to support and much higher costs, then all else isn’t equal, but you see my point.

There are wealthy people out there sleepwalking through life who have far more career freedom than Coleman Hawkins does. Some of them are reading this blog post.

But this argument doesn’t feel right does it? Something about being young with money seems more freeing than being older with money. But, for the same amount of money, the older person would have more freedom. If you believe that having $2M at 23 is “set for life,” then having $2M at 35 or 45 or later would be even more so.

The best part about this discussion is that you don’t have to have $2M (or $1.2M) to make a change in your career. But, some of you do have that much and still haven’t taken the leap.

Well, consider this your wakeup call. Because it takes a lot less to be “set for life” than you might think. Thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 444. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data