There’s an old saying that goes, “Concentrate to get rich, diversify to stay rich.” The idea being that you should put all of your assets into one (or a few) investment(s) to build your wealth and then spread your capital around later in life to preserve it.

However, the longer I’ve been investing the more I’ve come to despise this phrase. Because while concentration can lead to riches, it can also lead to ruin. This is known as concentration risk and there are plenty of examples of it throughout financial history:

- In 1998, Long Term Capital Management lost $4.6 billion and had to be bailed out due to their concentrated positions in interest rate swaps.

- In 2008, Lehman Brothers filed for bankruptcy because of their extensive exposure to mortgage-backed securities filled with subprime loans.

- In 2021, Bill Hwang of Archegos Capital lost $20 billion in two days after his concentrated bets on a handful of stocks went south.

The financial graveyard of history is filled with concentrated investors.

And just last week, Silicon Valley Bank (SVB), the premier bank to Silicon Valley startups, became the latest victim to join their ranks after a bank run forced them into receivership with the FDIC.

Where did the 16th largest bank in the U.S. go wrong with regards to concentration risk? Let’s dig in.

How Concentration Risk Killed Silicon Valley Bank

When it comes to the demise of SVB, there are two areas where concentration risk played a pivotal role.

First, SVB had a concentrated position in longer-term Treasury bonds which they acquired before the recent rise in interest rates. Therefore, as rates increased throughout 2022, their bond portfolio took a massive hit. As Marc Rubinstein stated in his excellent overview of SVB’s demise:

Unrealised losses snowballed, from nothing in June 2021, to $16 billion by September 2022…So big was this drawdown that on a marked-to-market basis, Silicon Valley Bank was technically insolvent at the end of September. Its $15.9 billion of HTM mark-to-market losses completely subsumed the $11.8 billion of tangible common equity that supported the bank’s balance sheet.

But, what made the first concentration problem worse was a second concentration problem—SVB’s customer base.

Unlike many other banks in the United States, SVB specialized in banking for startups. In fact, according to SVB’s own marketing, nearly half of the 130,000 venture-backed startups in the U.S. banked with SVB.

As a result, SVB was more susceptible to macroeconomic shocks that could negatively impact its homogenized customer base. Unfortunately, the one macroeconomic shock that could harm SVB’s customers was the same shock that could harm its assets—rising interest rates.

So when rising rates materialized, SVB went into a death spiral. As Matt Levine summarized:

And so if you were the Bank of Startups…it turned out that you had made a huge concentrated bet on interest rates. Your customers were flush with cash, so they gave you all that cash, but they didn’t need loans so you invested all that cash in longer-dated fixed-income securities, which lost value when rates went up.

But also, when rates went up, your customers all got smoked, because it turned out that they were creatures of low interest rates, and in a higher-interest-rate environment they didn’t have money anymore. So they withdrew their deposits, so you had to sell those securities at a loss to pay them back. Now you have lost money and look financially shaky, so customers get spooked and withdraw more money, so you sell more securities, so you book more losses, oops oops oops.

This is an example of how concentration can go wrong fast.

But to provide a more realistic example of how concentration risk impacts a typical investor, we turn to our next section.

Visualizing Concentration Risk (for the Typical Investor)

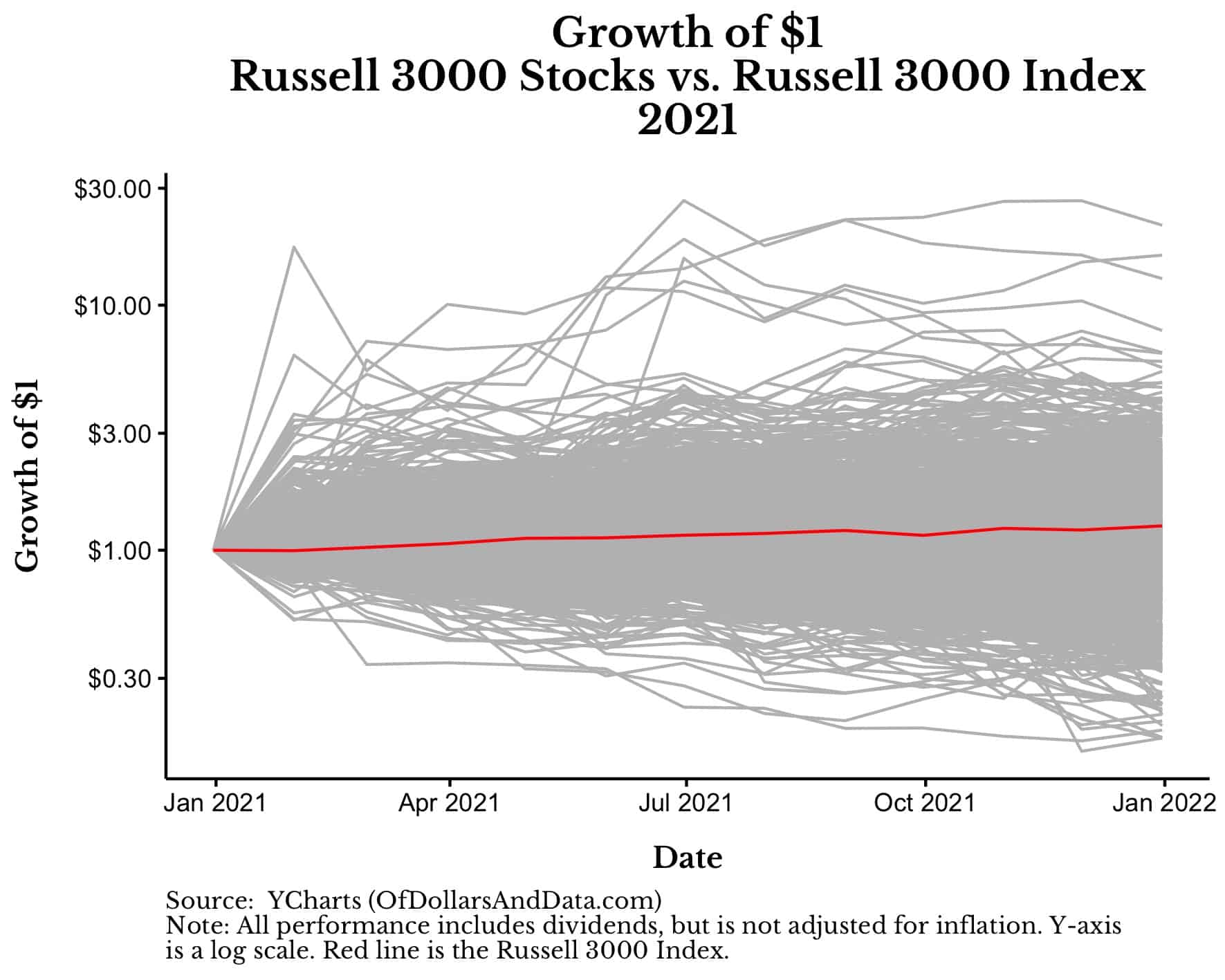

If you want a visualization of concentration risk, you only need to compare the performance of the Russell 3000 Index versus its individual stock components for 2021 and 2022.

I’ve done this in the plot below which shows the performance of the Russell 3000 Index (in red) and each of its underlying stocks (in gray) throughout 2021 [Note: the y-axis is a log-scale]:

This plot demonstrates the dispersion in performance that accompanies more concentrated positions (i.e. individual stocks). In particular, some stocks grew by 3x (or more) while others were cut in half. The 25th percentile performance was 0%, the median performance was +23%, and the 75th percentile performance was +49% in 2021. This all happened in a year where the Russell 3000 Index was up 26% (e.g. $1 grew to $1.26 by year end).

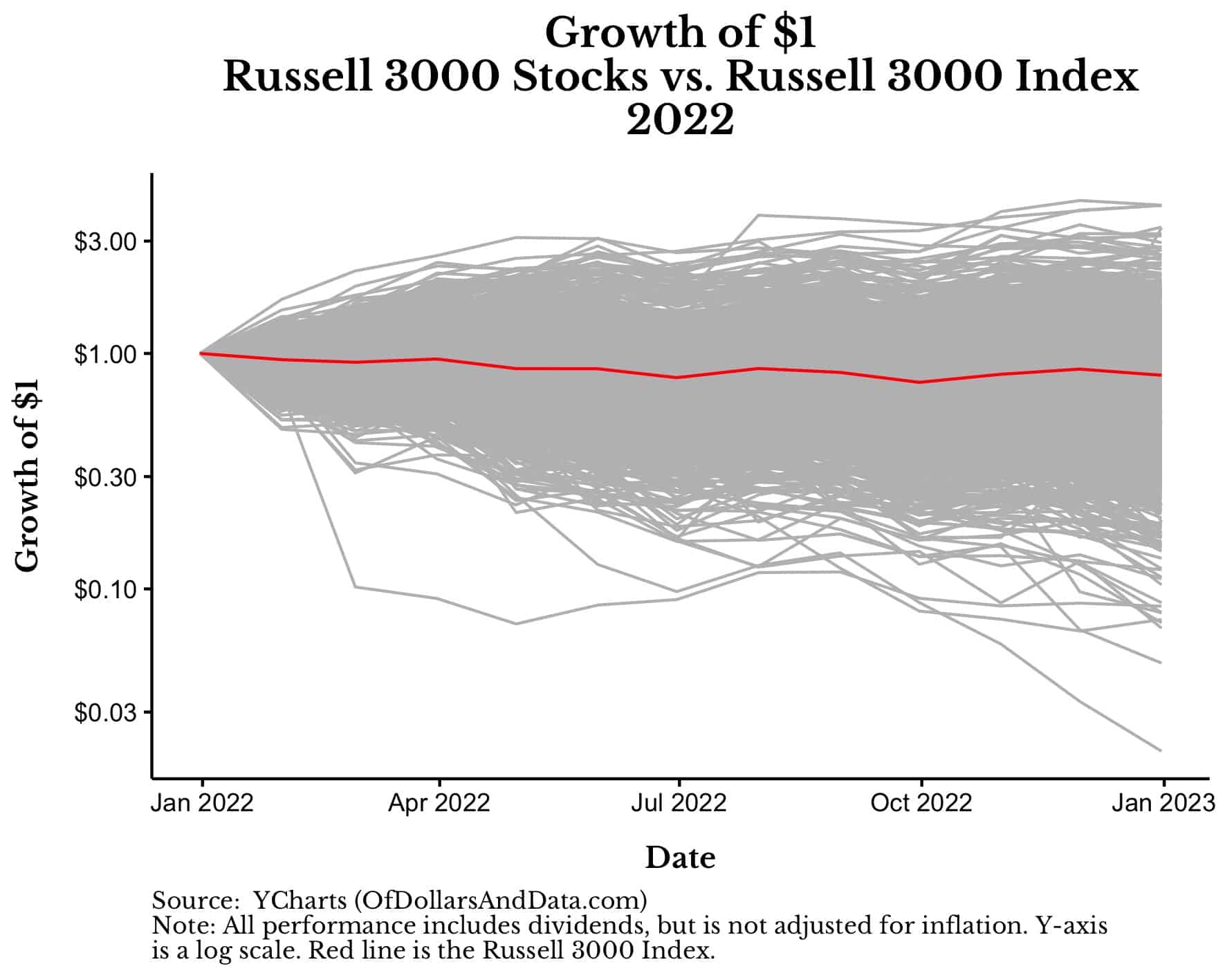

However, 2021 was a good year for most stocks and stock indices. If we were to plot the same thing for 2022 (a not so good year), then the story would be quite different:

Now we can see the downsides of concentrated positions a bit more clearly. In 2022 there were no stocks that went up 10x or more (like we saw in 2021) and there were even quite a few stocks that lost over 70% of their money by year end (e.g. $1 became $0.30). In particular, the 25th percentile performance was -38%, the median performance was -18%, and the 75th percentile performance was +3%. This was in a year where the Russell 3000 Index lost 20% (e.g. $1 became $0.80) by December 2022.

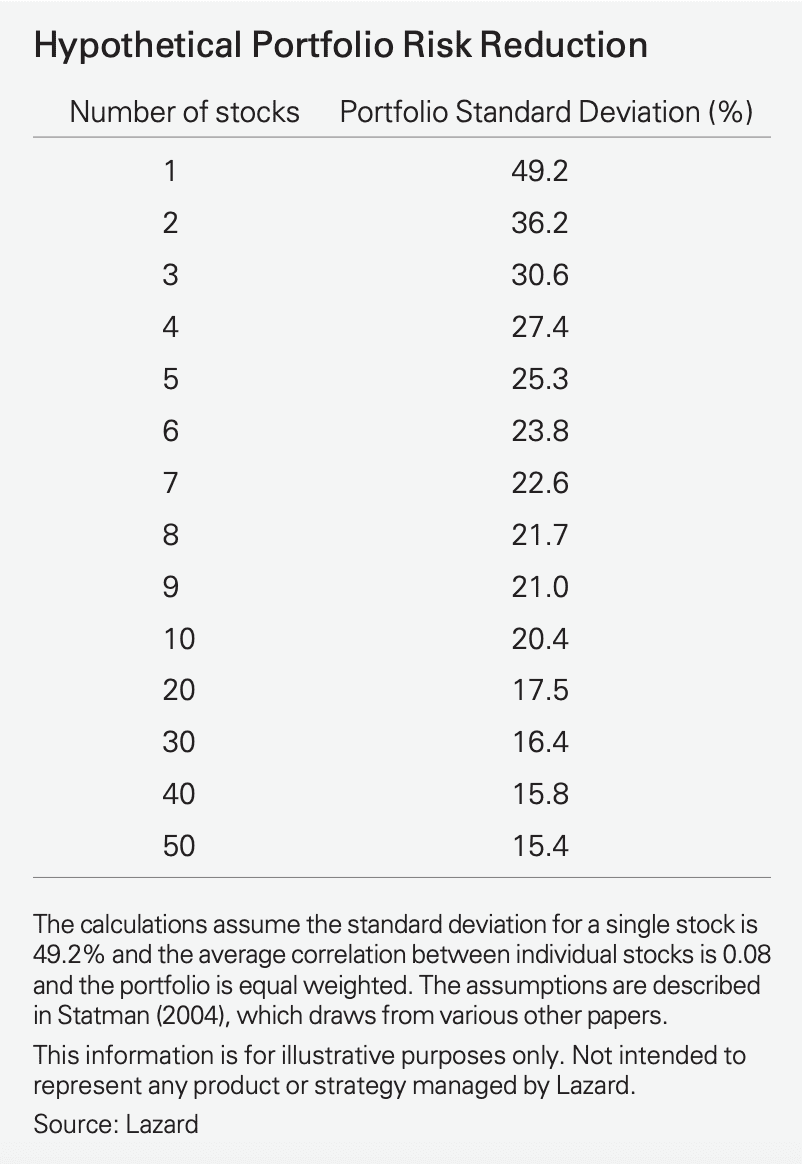

While these plots provide empirical evidence for the riskiness of concentrated positions, the theoretical evidence exists as well. As Lazard highlighted in this review of studies discussing concentrated portfolios, as the number of stocks in your portfolio increases, the standard deviation of your portfolio (i.e. risk) drops:

In particular, going from a 1-stock portfolio to a 5-stock portfolio cuts the standard deviation in half, and going from a 5-stock portfolio to a 50-stock portfolio reduces the standard deviation by another 40%.

This demonstrates how avoiding concentration can reduce risk at the portfolio level. However, there are other things we can do in our financial lives to avoid concentration risk as well.

How to Avoid Concentration Risk (and the Limits to Diversification)

When we talk about avoiding concentration risk, we are typically referring to the risk you take within your portfolio. However, there are many other areas of your financial life where reducing concentration risk could be equally, if not more, impactful. For example, you could:

- Expand your banking relationships. With everything that happened in the last week at SVB, now is a good time to re-evaluate whether you should have a secondary banking relationship in case your primary bank gets into financial trouble.

- Build multiple streams of income. Relying on a single source of income, such as a job or a business, can leave you vulnerable to unexpected changes in employment or market conditions. Consider developing multiple streams of income, such as rental properties, royalties, or other income-producing assets to mitigate this risk.

- Have different insurance providers. Depending on a single insurance provider to cover all your needs can be risky, especially if that provider experiences financial troubles or coverage changes. Consider diversifying your insurance policies across multiple providers to ensure adequate coverage.

- Diversify your geographic location. Concentrating your financial life in a single geographic location can be risky if that area experiences a natural disaster, economic downturn, or other unforeseen event. Consider diversifying your assets and investments across different regions and countries to spread out this risk. Though this will be easy for an index investor, someone who owns physical real estate/businesses may find this more challenging.

While I could continue adding to this list by including the diversification of what currencies you hold, your career skills, and so forth, the truth is that diversification has its limits. We can’t hedge everything in life. At some point we have to take some actual risk.

After all, what would life be like without risk? Could we build anything of substance? And would we even enjoy it?

I don’t think so. In fact, some of the best things in life require risk and concentrated risk at that. For example, choosing a partner, raising a family, and mastering a skill are all things where diversification will lead you astray. These are areas where immense dedication of time, energy, and resources are required.

So while concentration risk is not your friend in your financial life, I wouldn’t be so weary of it everywhere else. Happy investing and thank you for reading.

If you liked this post, consider signing up for my newsletter.

This is post 339. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data