If building wealth is hard, building generational wealth is even harder. Generational wealth refers to accumulated assets and resources that can be passed down from one generation to the next. Whether it’s a cash inheritance or a vast estate of trusts, businesses, and other valuables, generational wealth is often considered a sign of success and achievement.

Many people like the idea of generational wealth because of the financial security and access to opportunities it can provide to future heirs. In addition, generational wealth can also be appealing to those who want to leave a legacy that will live on many years into the future.

But, despite the many benefits of generational wealth, it also has its downsides. Generational wealth can ruin the motivation of your future heirs, create conflicts within your family, and perpetuate existing inequalities.

In this blog post, we will explore the concept of generational wealth, how it gets built (and destroyed), and why you might want to reconsider striving so hard for it.

How Do You Build Generational Wealth?

When it comes to building generational wealth, there is no one-size-fits-all approach. The strategy you choose will largely depend on how much wealth you hope to accumulate and pass down to future generations. This is why your strategy should differ if you want to build a significant, multi-generational fortune rather than a smaller sum. This section details both approaches.

Building a Multi-Generational Fortune

If you want to build a vast fortune that can last for multiple generations, then you will need to start a successful business venture. Though exceptions to this rule exist, there aren’t many.

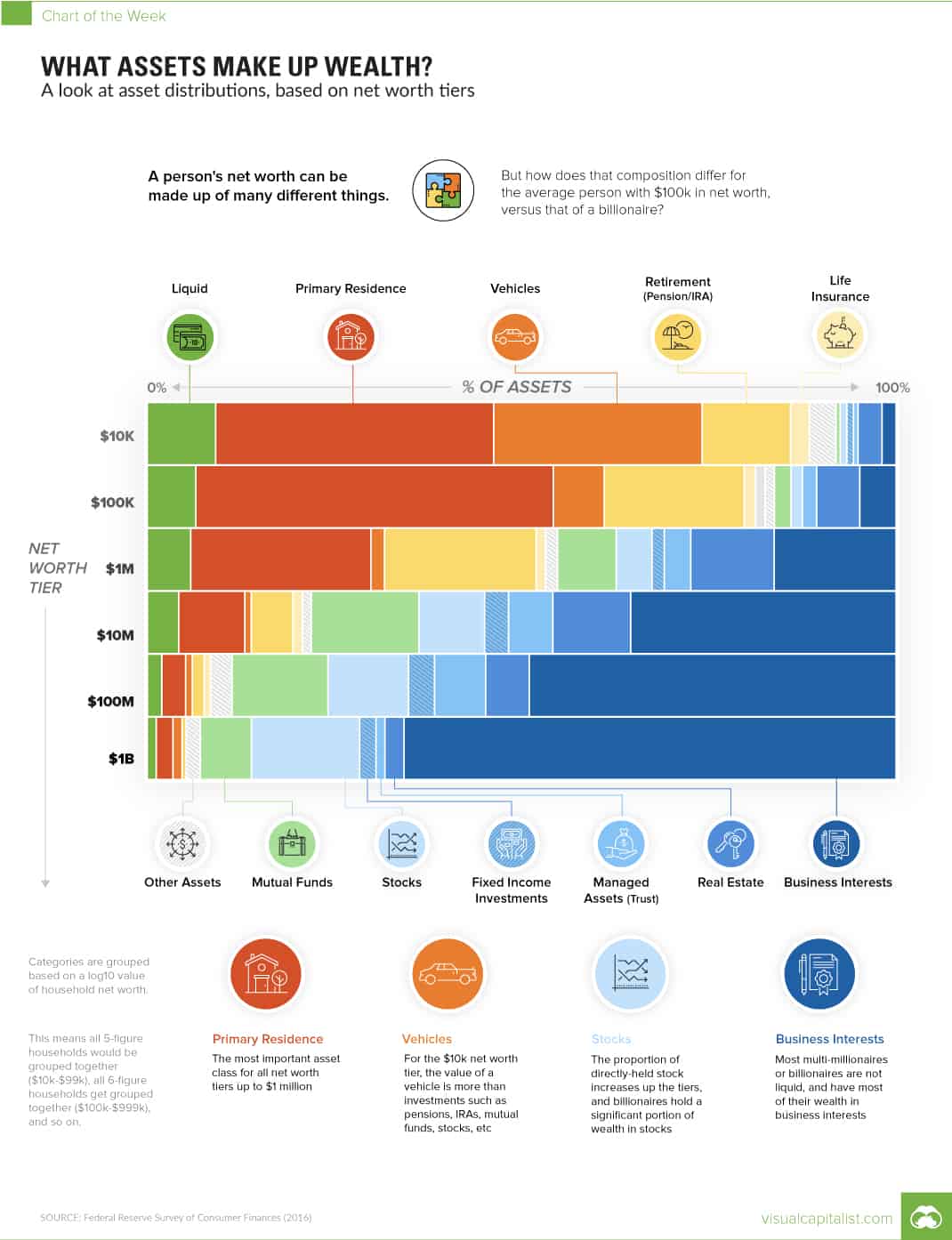

When we examine the wealth composition of the absolute wealthiest households, we see that business ownership is central to their fortunes. The chart below (from VisualCapitalist) demonstrates this clearly by illustrating how household net worth is broken out across different wealth tiers:

As you can see, the allocation to business interests tends to increase alongside wealth and this is true all the way up the wealth spectrum.

Looking at this you will realize that founding (or getting significant equity in) a successful business is how you build wealth on a large scale. This is how the Walton family (of Walmart fame) became the richest family in America with an estate worth over $200 billion, and how most billionaires on the Forbes 400 list got their wealth as well.

And, even for the 30% on the Forbes 400 that inherited a significant portion of their wealth, that inheritance came from someone who created a successful business. It’s business ownership all the way down.

Of course, creating a successful business is easier said than done. But, if vast wealth is your desire, you don’t have much of a choice. For everyone else, there is a much simpler path to generational wealth, albeit on a smaller scale.

Generational Wealth for the Rest of Us

Leaving behind smaller levels of generational wealth can still be a powerful way to impact your family’s financial future. Here are some steps you can take to achieve this:

- Start early: The earlier you start investing, the more time your money has to compound and grow. As I’ve shown previously, someone who invests for 10 years (and then stops) will end up with more money than someone who waits 10 years and then invests for the next 30 years (at a 7% rate of return).

- Save diligently: For most people, how much you save will be far more important than how well your portfolio does. As I demonstrated here, the amount of time it takes to double your money is more dependent on your savings rate than your rate of return.

- Invest in a diverse set of income producing assets: The continual purchase of a diverse set of income-producing assets is the most reliable way to build wealth. This approach is backed by over a century’s worth of data and is the core thesis of my book Just Keep Buying. If it could work for your ancestors, then it can work for you.

- Plan for taxes: When passing down wealth, it’s important to consider the tax implications. Depending on the size of your estate and the state you live in, your heirs may be subject to estate or inheritance taxes. Working with an attorney or financial advisor can help you plan for these expenses and minimize their impact on your heirs.

- For example, if you have an aging parent who owns some real estate, it’s probably best not to transfer it into your name before their death. Due to the stepped-up basis rule, the cost basis on the property will be “stepped up” to its market value on the day of your parent’s death. As a result, any capital gains on the property will be eliminated. This is just one example where proper tax planning can make a big difference in terms of generational wealth.

- If you want to learn more about the basics of estate planning, I highly recommend this lecture given at Stanford Business School by Robert N. Grant on the topic.

While we all can’t leave behind massive fortunes for our loved ones, taking the right steps today can make things much easier for your future heirs.

But the most important thing you can do to give your offspring generational wealth is not to destroy it. For this we turn to our next section.

What Destroys Generational Wealth?

As Charlie Munger once said:

The first rule of compounding is to never interrupt it unnecessarily.

The same can be said of generational wealth. Unfortunately, interrupting it unnecessarily is easier than you might imagine. As a result, below I’ve compiled a list of the most common ways generational wealth is destroyed. If you (and your heirs) can avoid such pitfalls, then you stand a chance of preserving wealth for the next generation:

- Poor financial management: A lack of financial education and planning can lead to the mismanagement of assets, resulting in the gradual erosion of generational wealth. The two primary ways in which this occurs are: rising costs from excess spending and declining assets from poor investment choices. Practicing good financial habits and teaching financial literacy to your loved ones are the best ways to mitigate this.

- Family disputes and legal battles: Disagreements over the division of wealth among family members can lead to costly legal battles that may consume a significant portion of your family’s assets and lead to strained relationships. The 2019 film Knives Out and the HBO television series Succession both do a great job illustrating this. Having a culture of open and honest communication within your family can prevent such disputes from materializing.

- Marital issues and divorce: Similar to family disputes, the dissolution of a marriage can lead to a substantial division of assets and a rapid reduction in generational wealth. Prenuptial agreements and other legal protections can help minimize this impact on your family’s fortune.

- Lack of diversification: As I discussed recently, concentration risk in a single asset class, industry, or geographic location can lead to a loss of generational wealth. If you have the bulk of your fortune in a few assets, an economic downturn or industry disruption could have a disproportionate impact on your finances.

- Inadequate estate planning: Failing to create a comprehensive estate plan that includes wills, trusts, and other legal mechanisms can lead to unintended consequences. Hefty estate taxes, probate fees, and other legal expenses can significantly diminish how much wealth you pass on to the next generation.

- Natural growth of family: While a growing family by itself won’t destroy generational wealth, over many generations it can cause it to slowly dwindle away. As Frazer Rice stated in Wealth Actually: Decision Making for the 1%:

While resources may be bountiful for the first and second generation, the third generation grows and the number of mouths to feed, house, educate, and entertain increases geometrically.

If we assume that your family size doubles every 25 years (i.e. once per generation), then your assets would need to grow by ~2.8% annually (after-inflation and net of spending) to keep up. That might not seem like a lot, but you have all the factors listed above working against you and then some.

For example, even if you plan around estate taxes, avoid family disputes, and are adequately diversified, market volatility may still do you in. This is how the Vanderbilts, one of the richest families in American history, lost the bulk of their fortune in the Great Depression. Their assets declined, yet their spending continued at an elevated rate as economic conditions worsened.

Now that we’ve looked at what destroys generational wealth, let’s examine some of the problems that can arise from obtaining it in the first place.

The Problem with Generational Wealth

While generational wealth can provide financial stability and open doors for your future heirs, it can also cause various issues that impact both individuals and society as a whole. These include:

- Loss of motivation and work ethic: Generational wealth can sometimes lead to a sense of entitlement and complacency among heirs. Knowing they have a financial cushion to fall back on, your heirs may not feel the need to work hard or develop the skills necessary for a successful career. This can result in a lack of purpose and fulfillment in their lives. After all, if you had to overcome all these hardships to grow as a person and become successful, why would you want to eliminate such obstacles for your children?

- Difficulty in forming genuine relationships: Heirs to generational wealth may struggle to form authentic relationships, as they may be unsure whether people are into them for their money or for who they are. This can lead to feelings of isolation and mistrust, making it challenging to build deep, meaningful connections.

- Pressure to maintain wealth and social status: Inheriting wealth can come with significant pressure to continue the family legacy. Your heirs may feel an immense burden to succeed in business or philanthropy, which can result in stress and anxiety.

- Perpetuation of social and economic inequality: As wealth is passed down from one generation to the next, individuals from wealthier families end up having a leg up over those from less privileged backgrounds. While this might not be seen as a problem for those passing down generational wealth, you might feel differently when your heirs are up against those with even more wealth than you.

- Potential for family conflict: As mentioned earlier, generational wealth can sometimes lead to disputes over inheritance and control of assets that, in some cases, can tear families apart.

To mitigate these potential issues, your best option is to educate your heirs on the importance of having strong values, a good work ethic, and the role of money in society. While this won’t guarantee that your heirs will avoid all of the issues listed above, it can better prepare them to handle their inheritance responsibly and make informed decisions when the time comes.

By encouraging financial education, emphasizing the importance of giving back through philanthropy, and fostering a sense of purpose beyond wealth accumulation, you can create a lasting legacy that not only benefits your heirs, but also contributes positively to society.

The Bottom Line

Generational wealth can be a double-edged sword. While it can provide financial security and opportunities for future generations, it can also lead to a host of personal, familial, and societal issues. Fortunately, many of these issues can be mitigated by nurturing a strong set of values, a good work ethic, and financial literacy among your heirs.

Nevertheless, the hardest part about generational wealth is creating and preserving it over time. While early investment, diligent saving, and concentrated business ownership can help you get started, you will need to be vigilant in both your personal and your financial life if you want to safeguard your fortune for future generations.

In the end, the key to passing down a meaningful and lasting legacy lies in striking a balance between providing financial support to your heirs and teaching them how to live a good, fulfilling life. By focusing on these aspects, you can help ensure that your family’s wealth is not only preserved but used responsibly toward a brighter future.

Happy investing and thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 341. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data