With 10-Year U.S. Treasury Bonds currently yielding less than 1% annually, the question on so many investors’ minds is:

Why should I own bonds at all?

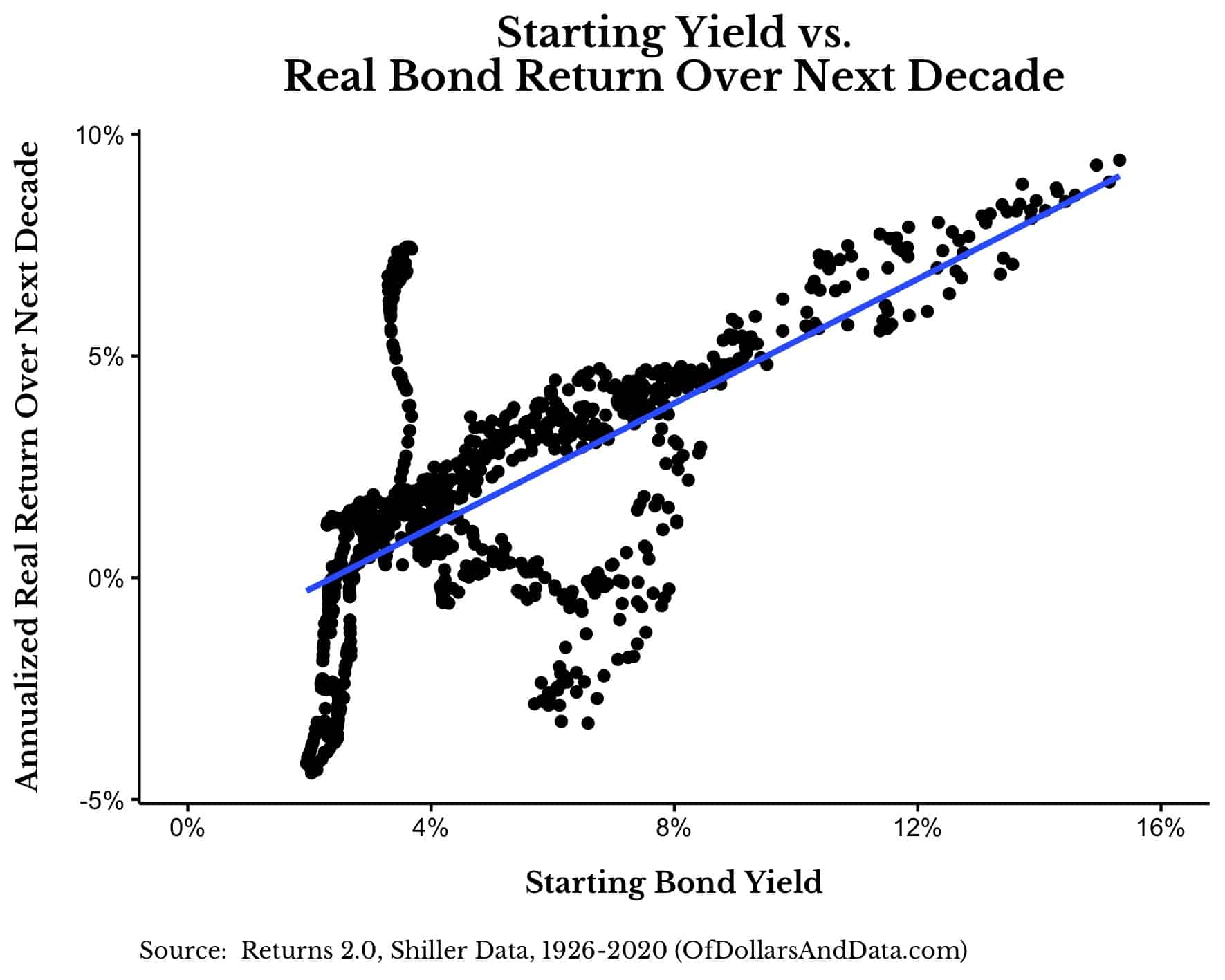

And I understand the sentiment. If we compare the starting yield on 10-Year U.S. Treasury Bonds to the real return on U.S. bonds over the next decade, you can see that there is a positive relationship:

From 1926-2010, a lower starting yield generally meant lower bond returns over the next 10 years.

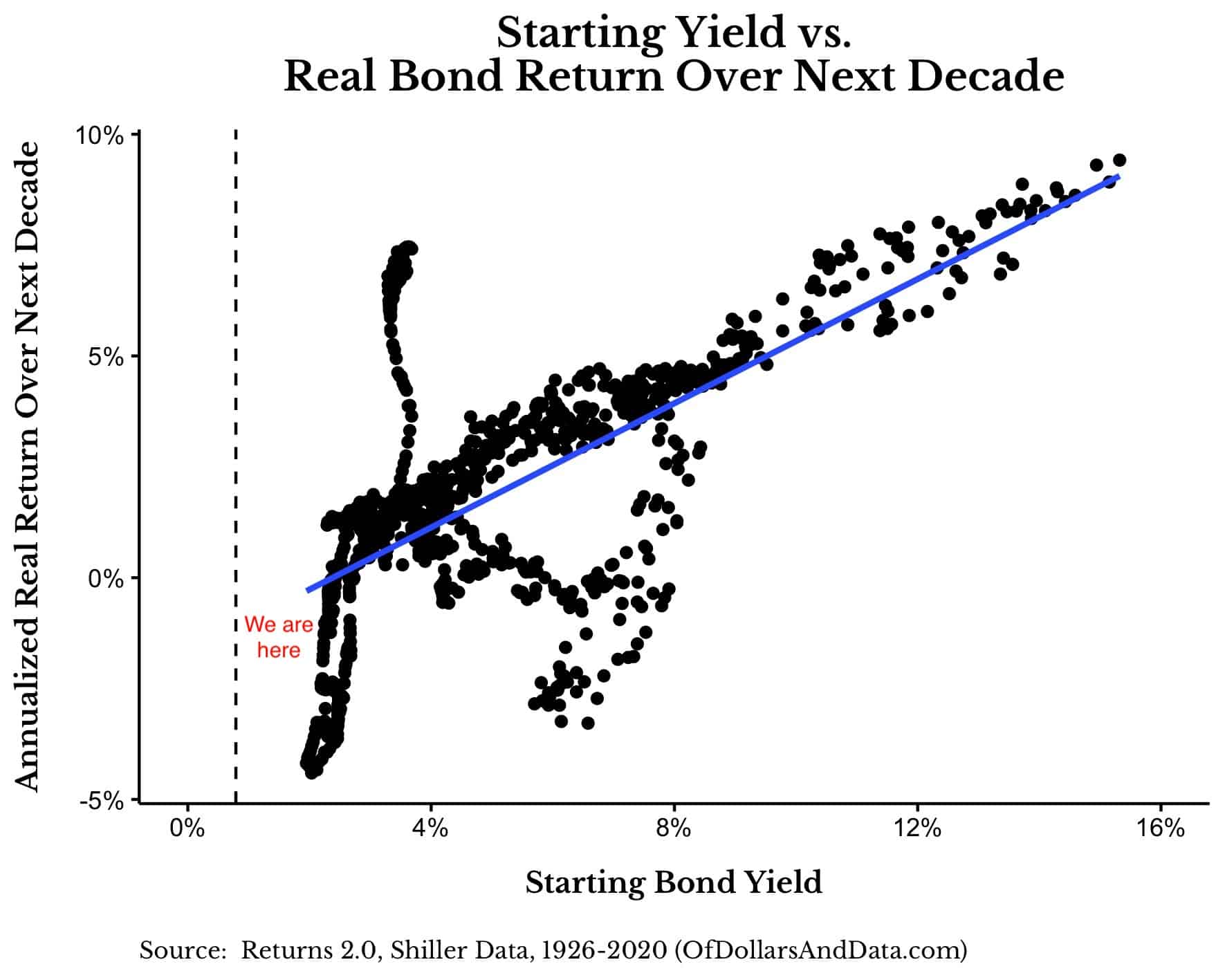

And with 10-Year U.S. Treasury Bonds currently yielding only ~0.79% (see vertical line below), returns for the coming decade are looking pretty grim:

This chart illustrates that investor fears about U.S. bonds are warranted and that real returns are likely to be negative for the foreseeable future.

So, if you are nearly guaranteed to reduce your future purchasing power when buying U.S. bonds today, why own them at all? Below are three reasons to consider.

1) Bonds Tend to Rise When Stocks Fall

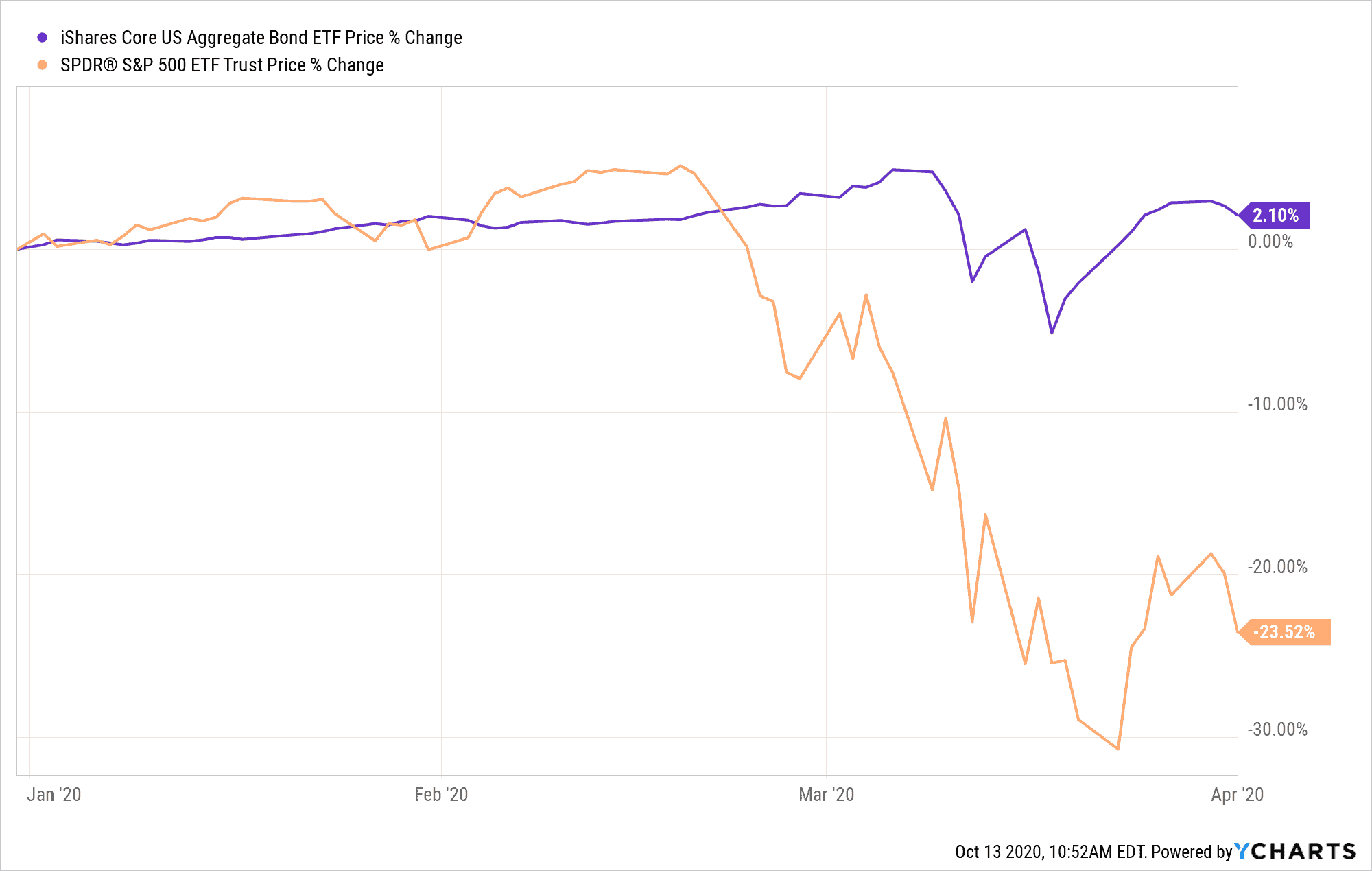

Though expected bond returns are likely to be low for the next decade, during periods of market turbulence bonds tend to do quite well. For example, U.S. bonds were up 2% while the S&P 500 was down 23% on April 1, 2020:

Though the S&P 500 has since recovered, this example illustrates how U.S. bonds can add value during market panics.

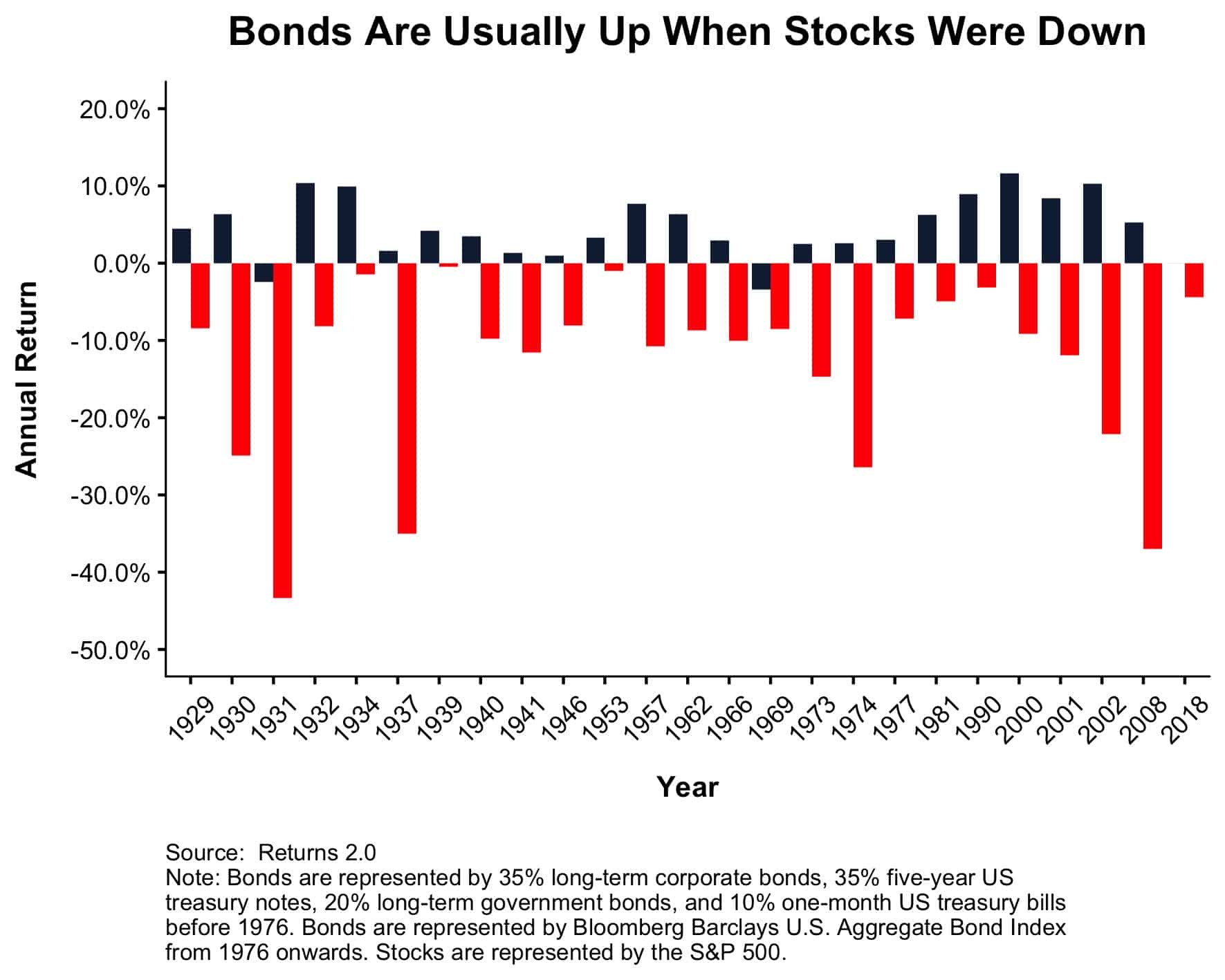

And if you go back further in time, you will notice that bonds are usually up in years when stocks lose money:

This is why the old saying goes:

We buy stocks so we can eat well, but we buy bonds so we can sleep well.

For this reason alone, bonds can be a worthwhile diversifier within your portfolio. However, the more relevant question you need to answer is:

Are you willing to pay for downside protection that used to pay you?

If you don’t think the downside protection provided by bonds is worth paying for, then what about the boost in returns that you can get through rebalancing?

2) Bonds Can Provide Added Return Through Rebalancing

In addition to providing a counterbalance to the stocks in your portfolio, bonds can also provide added return through periodic rebalancing. Rebalancing improves returns because it forces you to sell assets that are doing well and buy assets that may be temporarily depressed. As long as those temporarily depressed assets recover in price, then this method can be quite profitable.

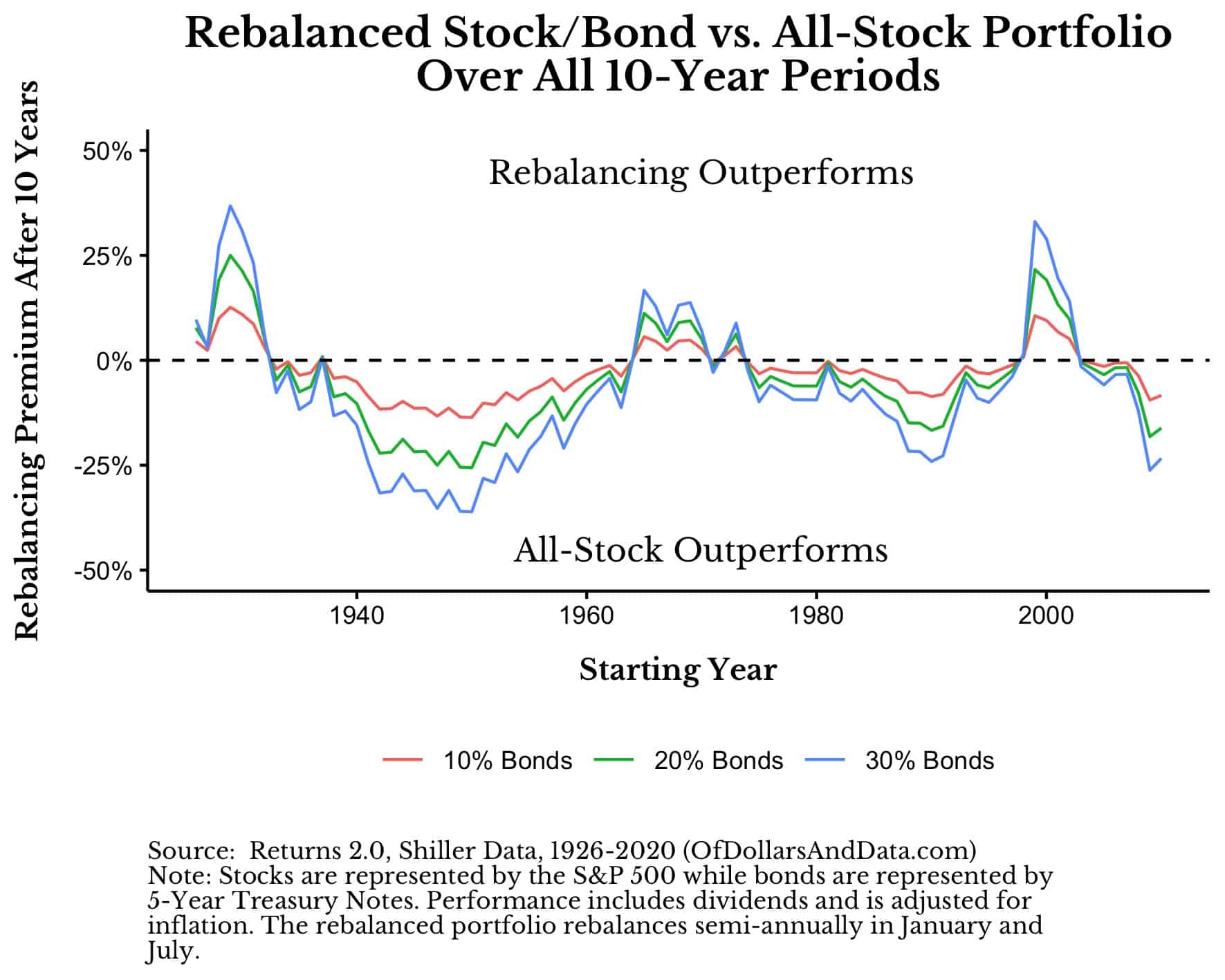

For example, below I did a simulation where I compared the performance of an all-stock portfolio to a portfolio that rebalances semi-annually for every 10-year period starting in 1926. As you can see, during the periods where the stock market performed poorly (1930s, 1970s, 2000s), a rebalanced portfolio outperformed an all-stock one:

This is evidence that holding and rebalancing with bonds can boost your portfolio returns, but only during periods of major market turbulence. More importantly, as you increase your bond exposure (10%, 20%, 30%, etc.) the improvement in returns during these periods increases as well.

However, as the chart above also illustrates, during most 10-year periods a rebalanced portfolio has underperformed an all-stock one. And if we look over longer periods of time, this underperformance generally increases in magnitude. Most investors would take this as evidence against owning bonds, but I don’t think it’s quite that simple.

Because though a rebalanced portfolio only outperforms an all-stock portfolio on rare occasions, it does so at the best possible times. You get the benefits of a rebalanced portfolio precisely when you need them the most. After all, wouldn’t you rather see your portfolio do well during a storm than when everything is smooth sailing?

If you look at portfolio construction from the framework of avoiding maximum pain (i.e. catastrophic loss), than owning bonds is a clear no-brainer even if they are expected to lose you some money while you hold them. As Michael Batnick once wrote, “I’m willing to accept small paper cuts in order to avoid a giant gash.” The question is…are you?

3) There is No Alternative

Lastly, you should consider owning U.S. bonds simply because there is no alternative risk-free asset. If you want low risk and decent yield today, sorry, but you’re out of luck.

Yes, this is an unfortunate situation to be in, but every other investor is in the exact same circumstances. We are all seeing the writing on the wall and realizing that the good ‘ole days of earning a risk-free 6% are long gone.

So, if you want to take risk off the table, bonds are really your only option. You could hold cash, but you are likely to lose even more of your purchasing power with cash than with bonds. Yes, you could add other kinds of bonds (with higher yields) to your portfolio, but these kinds of bonds usually come with increased risk. There is nothing wrong with chasing after yield, but you should consider the tradeoffs before doing so.

I know how unappealing it is to hear that “there is no alternative,” but that is the world we live in today. The game has changed and has become more difficult than ever.

For example, in the 1950s Warren Buffett and Benjamin Graham made lots of their money purchasing companies selling below their net current asset value (“net-nets“). This style of investing is the equivalent of paying $50 for a suitcase that has $100 in it. But good luck finding such “net-nets” today.

This process of escalating difficulty has happened over and over again in the investment world. Every breakthrough has been met with increased competition before eventually becoming obsolete. Money never sleeps and neither does the Red Queen. In some ways, we are seeing the same thing happening today in the bond market. The easy money is gone.

It reminds me of this presentation given by Michael Mauboussin and Dan Callahan where they discussed the story of Jim Rutt, the former chairman of the Sante Fe Institute who also used to be an amateur poker player. As Rutt got better at playing poker, he sought out better competitors in order to keep increasing his skill. However, at some point, Rutt’s uncle saw what he was doing and gave him the following advice:

Jim, I wouldn’t spend my time getting better; I’d spend my time finding weaker games.

So unless you can find some weaker games, the road ahead won’t be an easy one. There is no alternative.

Thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 209. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data