During the market volatility in late February 2020, I got the following text from a friend:

Finally the bonds in my portfolio are serving a purpose

I responded:

No, the bonds in your portfolio were always serving a purpose. You just didn’t realize it until now.

Despite my comment, my friend makes a good point.

When I first started investing in 2012, I constantly questioned why I owned bonds. Actually, I hated the bonds in my portfolio. Oh, I underperformed the S&P 500 again? Thanks bonds.

But, after weeks like last week, I am reminded of their importance. This is what owning bonds is all about.

When the S&P 500 drops 4% in a day and your portfolio is only down 2.5%, that’s a win. It’s a small win, but one that can make all the difference psychologically. While others are panic selling, bonds keep you away from your financial tipping point.

However, bonds can play a much bigger role in your portfolio than emotional support. Here are three reasons (backed with data) as to why you should invest in bonds.

1) Bonds Tend to Rise When Stocks Fall

Unlike other assets, which tend to fall when stocks fall, bonds tend to rise. Why?

Because bonds, particularly U.S. bonds, represent a safe haven for most investors. Though these bonds can lose money, they generally don’t, at least not over a short period of time.

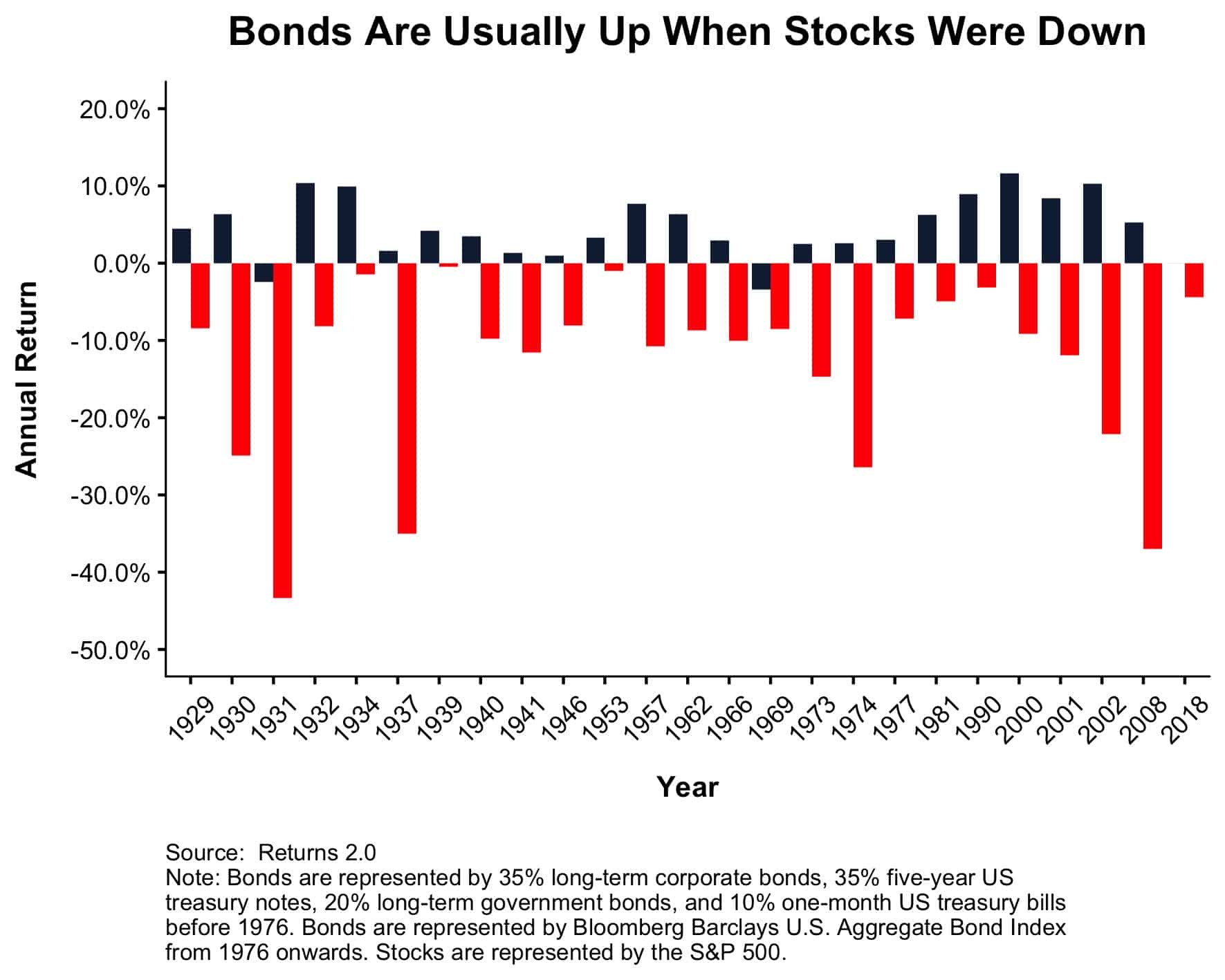

To illustrate this, I created a chart that shows how a long-term bonds performed in each calendar year when stocks were down:

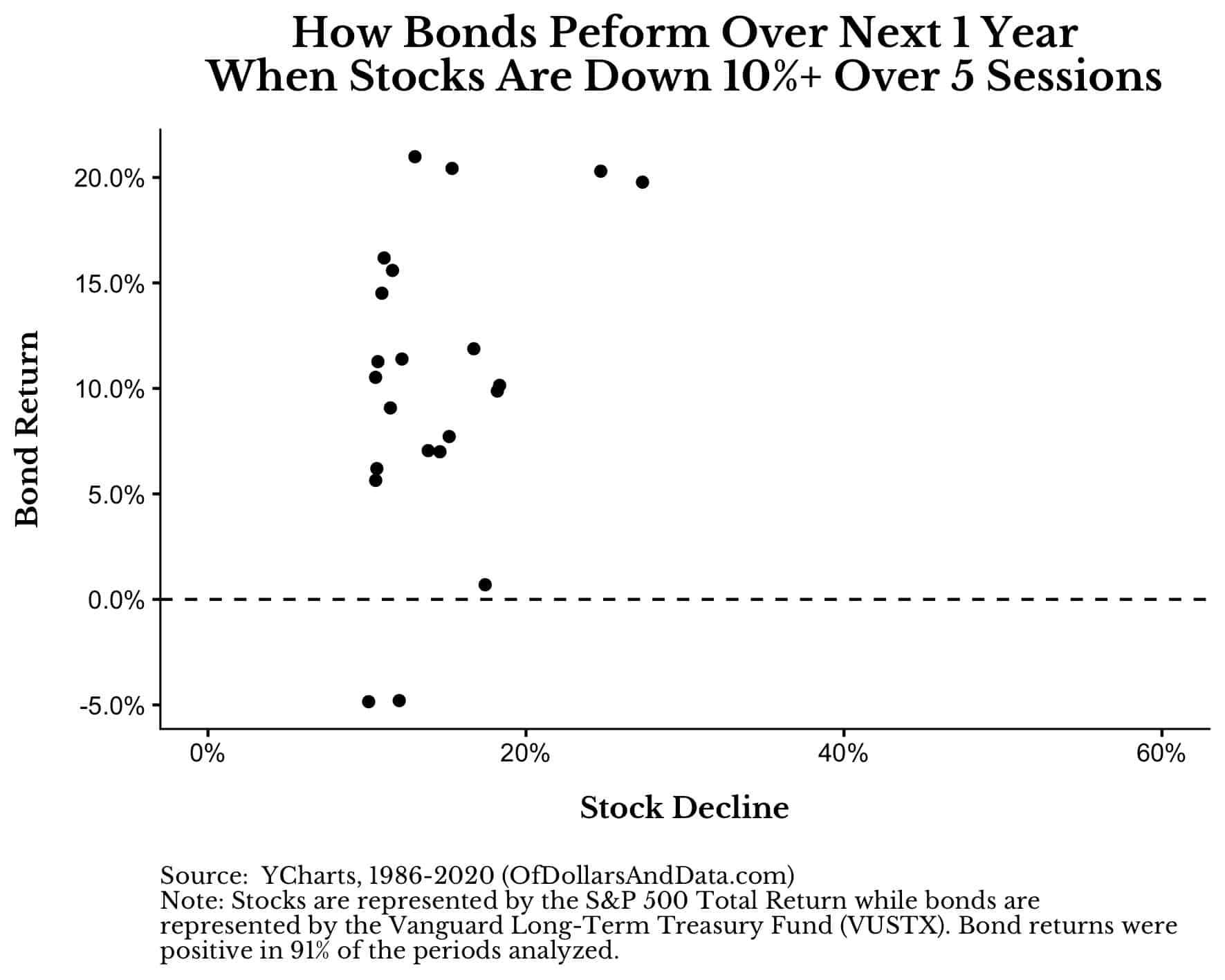

More importantly, you can see that when stocks were down by 10% or more over 5 sessions, long-term Treasury bonds tended to perform quite well over the next year:

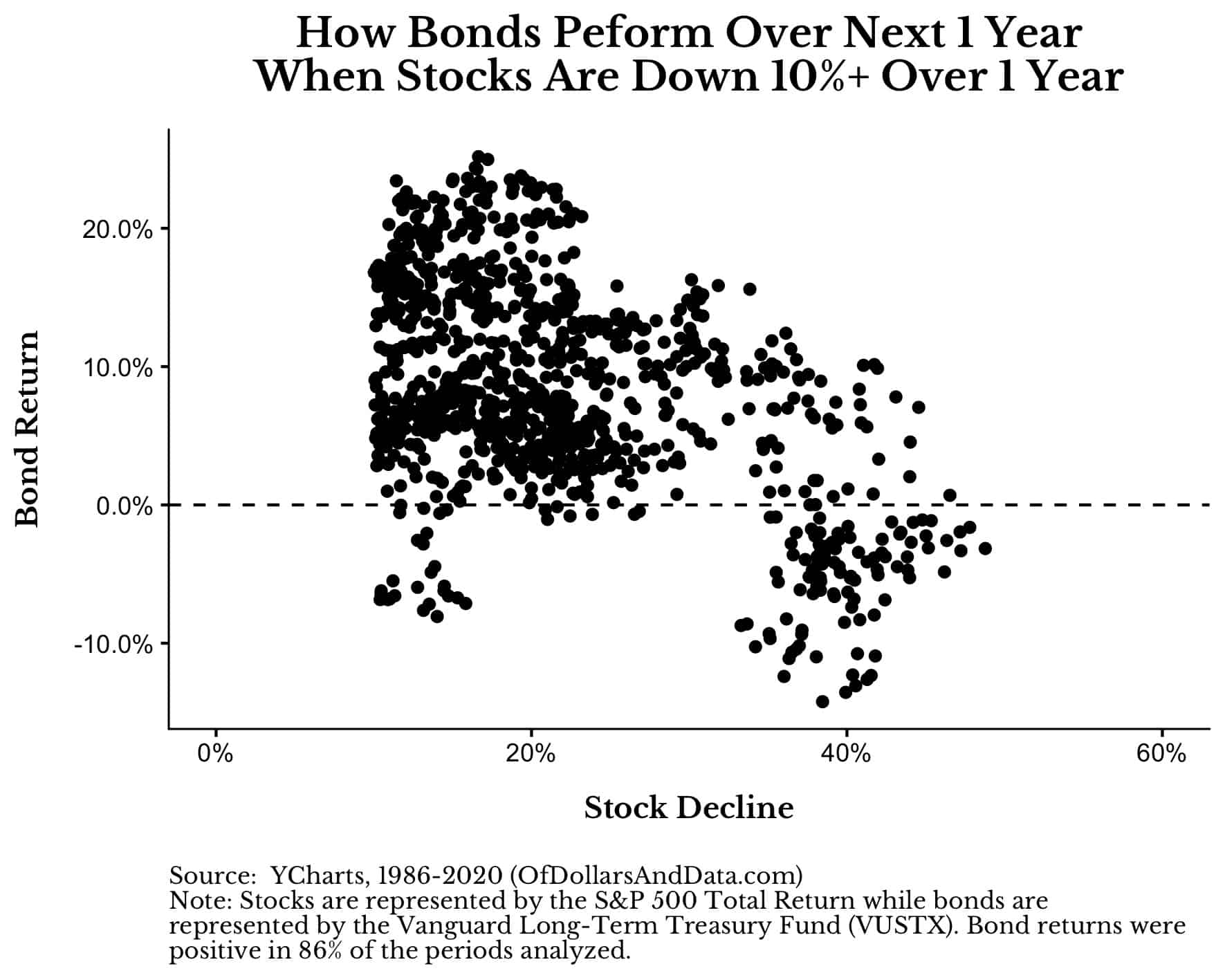

And while this analysis suffers from low sample size, if we look over longer periods of time, the relationship between stock declines and positive long-term Treasury bond returns is still present.

For example, when stocks are down 10% (or more) over 1 year, long-term Treasury bonds had a positive 1-year return 86% of the time since the late 1980s:

As you can see, despite the slight exceptions to this rule, bonds regularly act as a portfolio ballast during stormy economic times.

Because of this stabilization that bonds provide, this brings us to their next benefit—better performance through periodic rebalancing.

2) Bonds Act as a Form of “Dry Powder” When Rebalancing

Historically, U.S. bonds have compounded at about 5% a year compared to 10% for U.S. stocks, according to the Damodaran data. Despite this subpar performance when compared to equities, you could’ve outperformed an all-stock portfolio through periodic rebalancing with some bonds.

For example, the animated plot below compares an all-stock portfolio to one that rebalances twice annually (January + July) with varying amount of long-term Treasury bonds (10% to 50%):

As you can see, the rebalanced portfolio starts to outperform the all-stock one during periods of sharp market declines (i.e. post DotCom and post GFC), especially with higher bonds weights (40%+).

Of course, there is no guarantee that this will be true going forward, but, historically, bonds have provided you with “dry powder” to buy stocks on the cheap when markets crash.

But, the best part about bonds is not their outperformance potential with proper rebalancing, but that they do all of this with far less volatility.

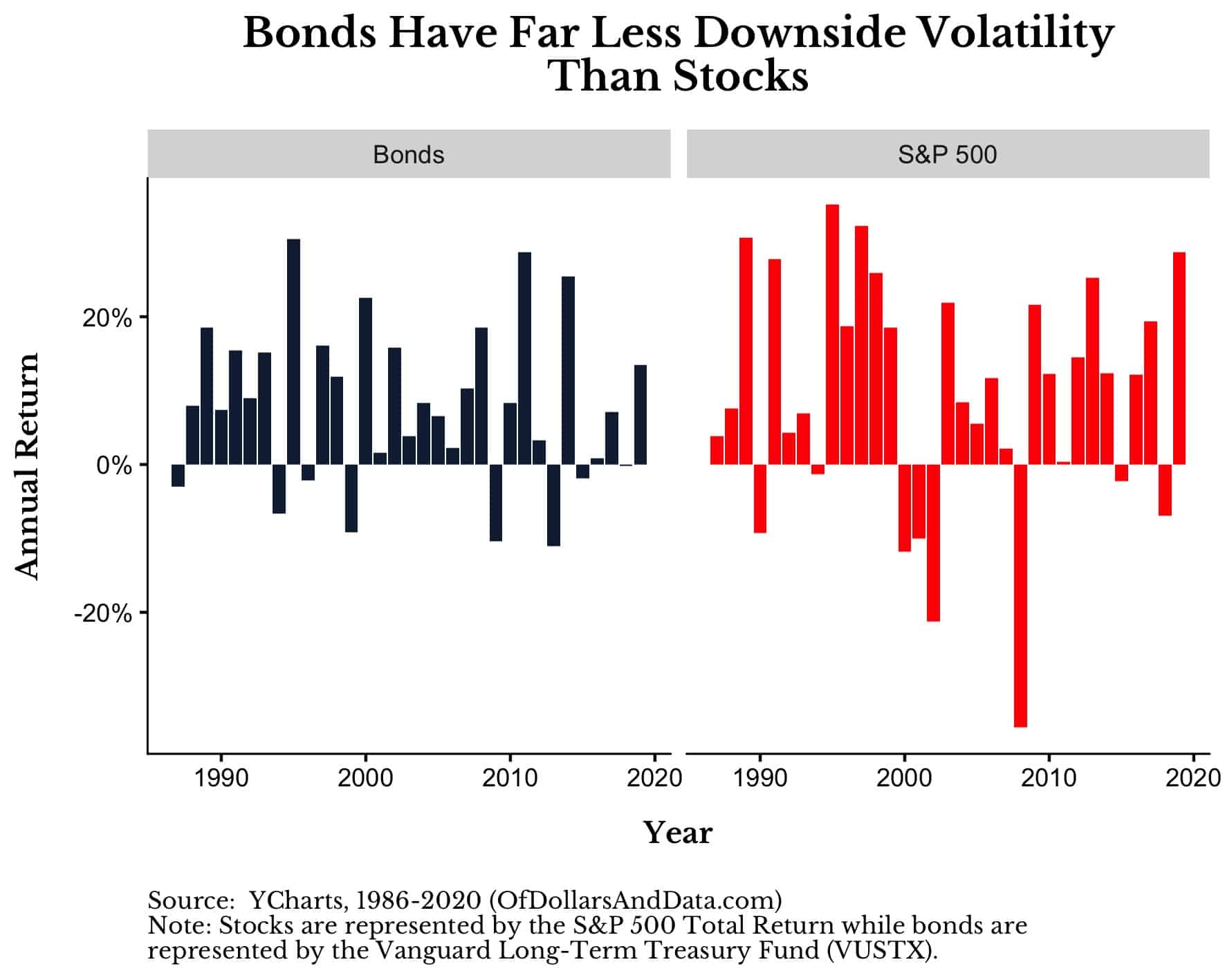

3) Bonds Are Less Volatile Yet Still Provide Income

Last, but not least, bonds can provide consistent income in your portfolio with far less volatility than stocks. If you examine the annual calendar returns for long-term Treasury bonds and the S&P 500, it is quite clear that bonds have much lower downside risk:

Additionally, because bonds pay income periodically, this can be especially important for retirees who rely on such income to fund their lifestyle. While stock dividends usually fall during downturns, bonds are far less likely to experience a similar reduction.

Of course, the highlighted period above (1987-2019) had higher than average bond returns when compared to most of history.

However, even if you believe bond returns will be lower in the future, the income from those bonds is likely to be safer than income derived from equities.

What Kind of Bonds Should You Invest In?

The last thing you may be wondering is, what kinds of bonds should you invest in. My philosophy on this issue is simple:

Your bonds should be as safe as possible. Take risk elsewhere.

As the saying goes:

Stocks let us eat well. Bonds let us sleep well.

And if you want to sleep well, a majority of your bond portfolio should be in U.S. Treasuries. Why U.S. Treasury bonds?

Because the U.S. government can just print the money they owe anytime they want. While this would be disastrous to the U.S. economy for other reasons, they technically can’t default on their obligations.

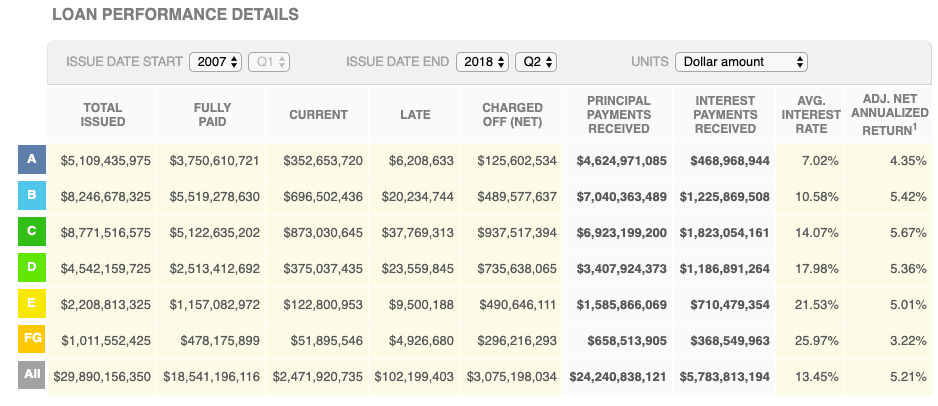

Other kinds of bonds (i.e. corporate, junk, etc.) have higher yields than Treasury bonds, but they don’t offer this same level of default protection. And this makes sense in theory because higher yields should be compensating you for the higher default risk of the underlying bonds.

You can see proof of this relationship from LendingClub, an online platform that matches lenders with borrowers. Their performance data shows that the highest interest rate debt (i.e. lower grade) does not necessarily have better returns (see the 2 columns on the far right for yields and net returns by grade):

This is just some evidence that higher yields aren’t necessarily what you should be chasing. If you want higher returns, do it outside of your bond allocation.

How Do You Invest in Treasury Bonds?

While you can invest in Treasury bonds directly through many online brokerages, I recommend owning a fund/ETF for simplicity.

But, how do you know which funds/ETFs own Treasury bonds? Google it. I’m serious.

If you Google “income from us government obligations” and the name of your fund provider, you should be able to easily find a list of all of their bond funds and what percentage of their income and holdings is from U.S. government obligations.

For example, here is Vanguard’s, Fidelity’s, and BlackRock’s lists (note: I am not recommending any of their products, they just happen to be some of the biggest fund providers in the space).

I use these kinds of lists (and NOT the name of the fund) to make sure I am buying those funds that are nearly 100% backed by U.S. government obligations. Because if the U.S. government bonds stop paying out, we have far bigger problems on our hands than our investment portfolios.

Don’t Miss Out

Despite the lower return expectations that most investors seem to have for bonds going forward, I hope you can see why this asset class can be an integral part of your investment portfolio. With that being said, thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 166. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data