I’m not one to make market predictions, but I’ve seen enough at this point. A few weeks ago I wrote about how the crypto community seemed to be getting a little ahead of itself. But, it’s not just crypto anymore. It’s happening in traditional finance too.

For example, less than two weeks ago Rivian ($RIVN), an electric vehicle manufacturer, IPO’d at over $100 billion despite having less than $50 million in pre-order deposits for their vehicles. This puts Rivian’s price-to-sales ratio (P/S) at an astronomical 2,169, which is nearly 100x greater than Tesla’s P/S ratio of 23. For context, most legacy automakers have a P/S ratio of less than 1.

I asked Twitter how things don’t end badly for Rivian shareholders and the only legitimate responses I got required either Rivian having $3-$5 billion in revenue in 2022 or them becoming the 2nd/3rd largest player in the electric vehicle space. Of course these outcomes aren’t impossible, but a lot of things have to go right for Rivian to sustain such a high valuation.

But Rivian is just the tip of the expectations iceberg. As I started digging deeper into what’s happening in markets, it became quite clear that things were getting a bit overextended. Let’s dig in.

Why Markets Seem Somewhat Overvalued (Hint: Look at P/S)

Right now investor expectations for the future are some of the highest on record. How so? Because the number of stocks with elevated price-to-sales (P/S) ratios has increased rapidly in recent years. Why is the P/S ratio the relevant metric here? Because, unlike other accounting measures such as earnings or book value, sales are much harder to manipulate. You either have them or you don’t.

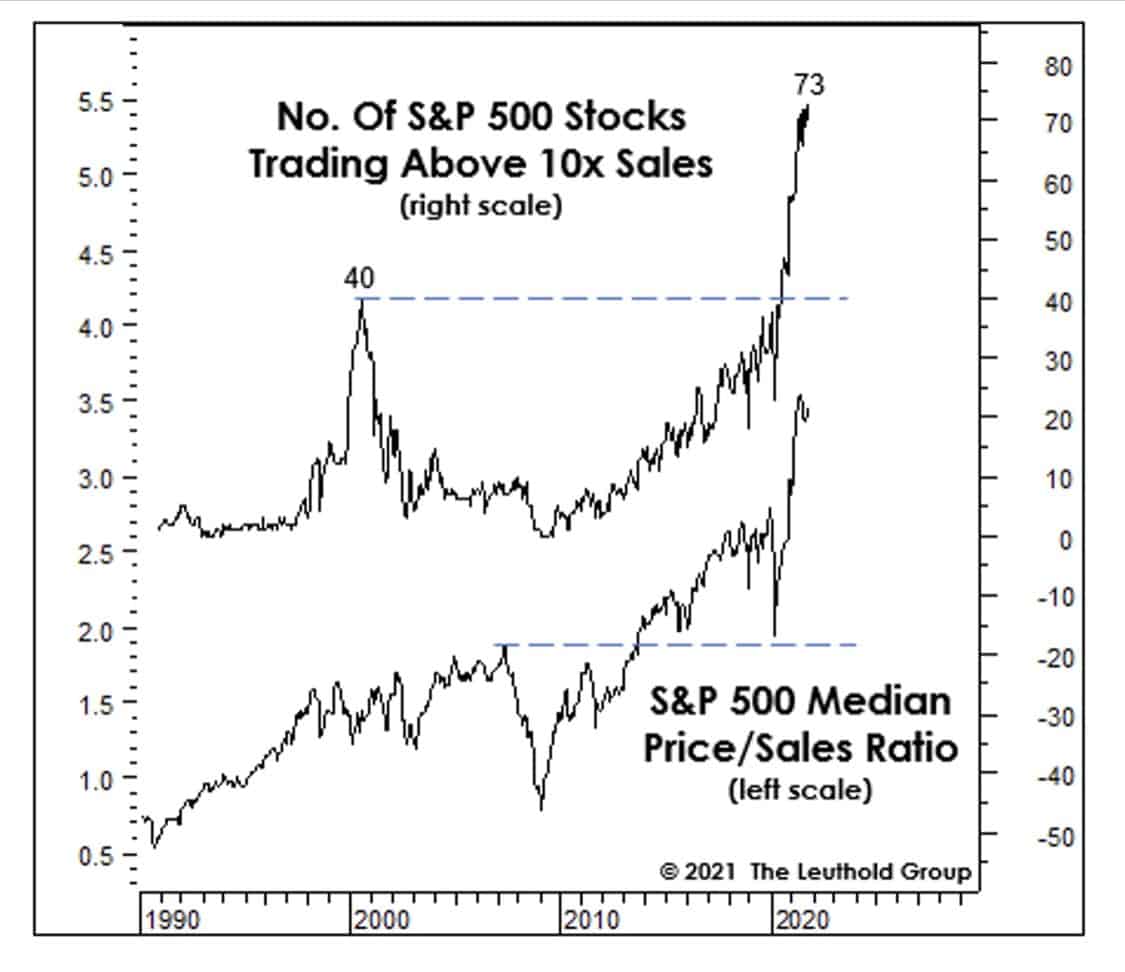

And guess what? As the Leuthold Group illustrated in the chart below, the number of the stocks in the S&P 500 with a P/S ratio of greater than 10 has exploded in recent years (h/t Meb Faber and Michael Batnick):

Seeing this and it makes the DotCom bubble look rather tame.

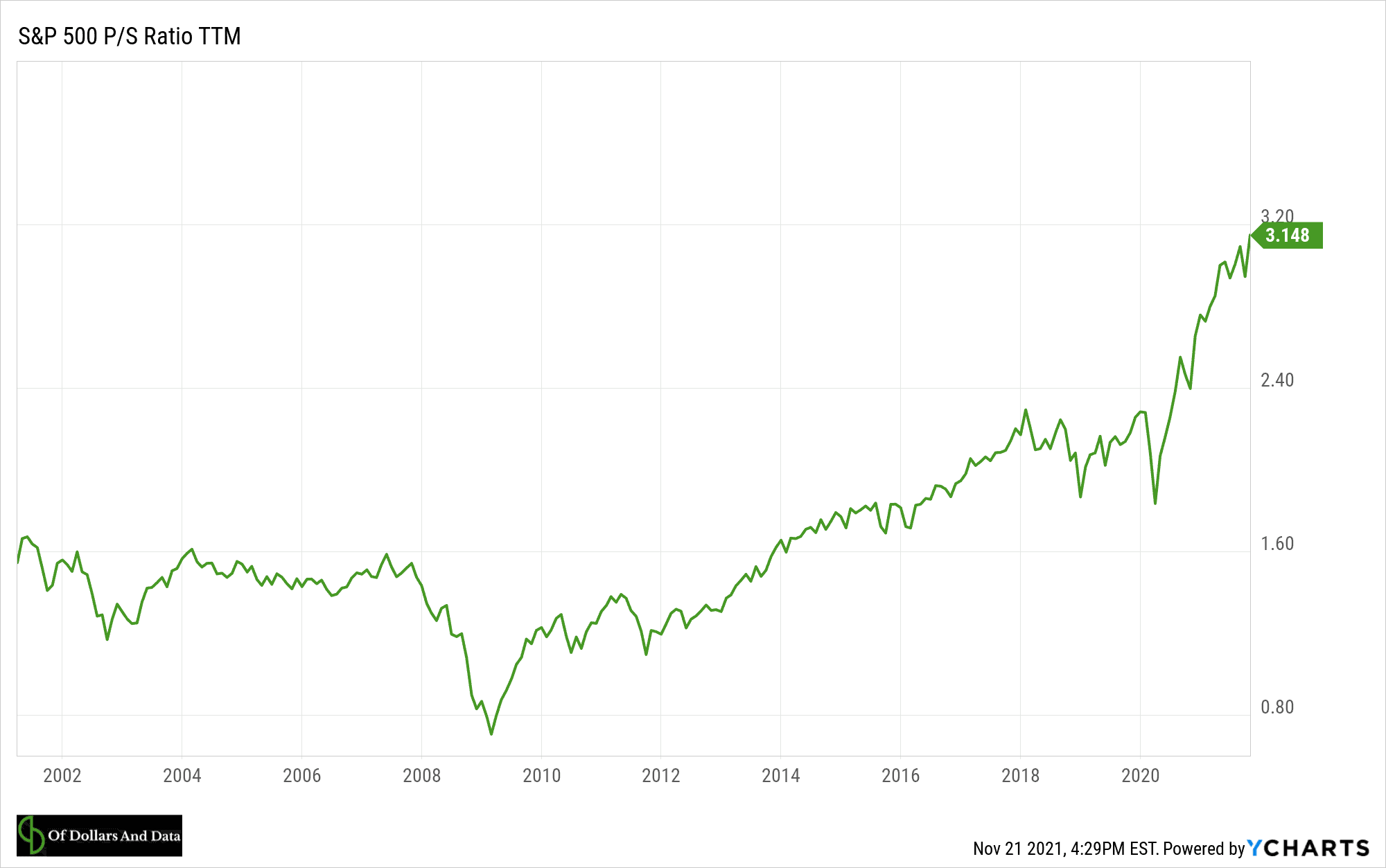

And if we look at the market as a whole, we see the same thing:

But wait there’s more.

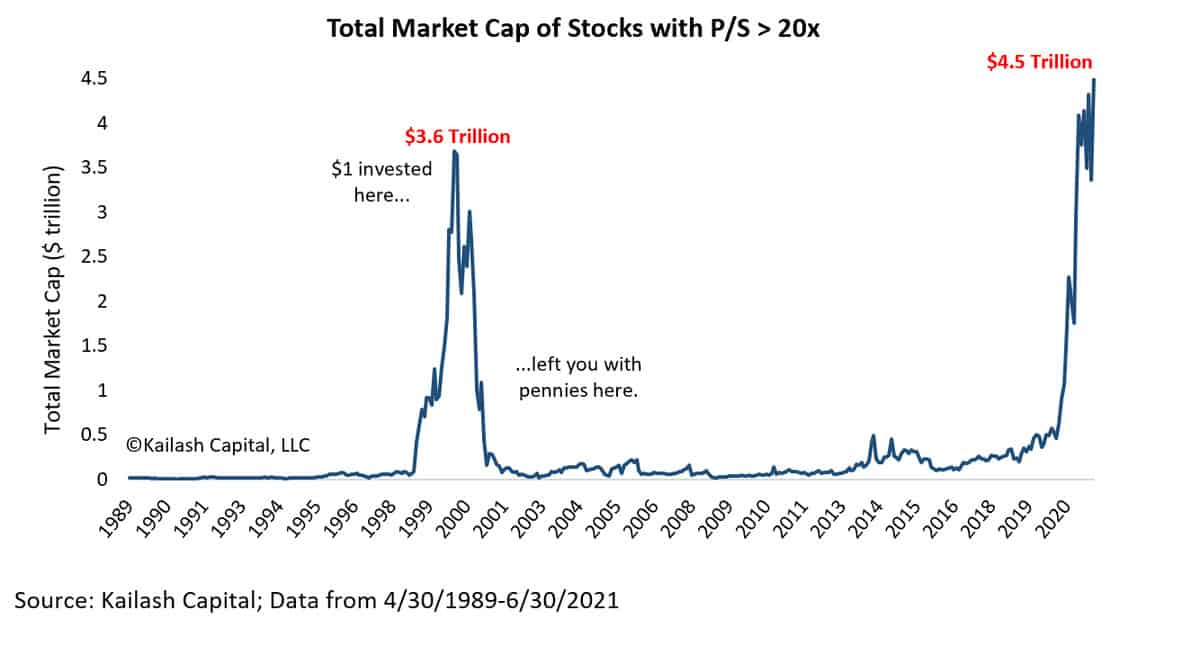

A few months ago Kailash Concepts tweeted out the chart below showing the combined market capitalization of all stocks with a P/S ratio greater than 20:

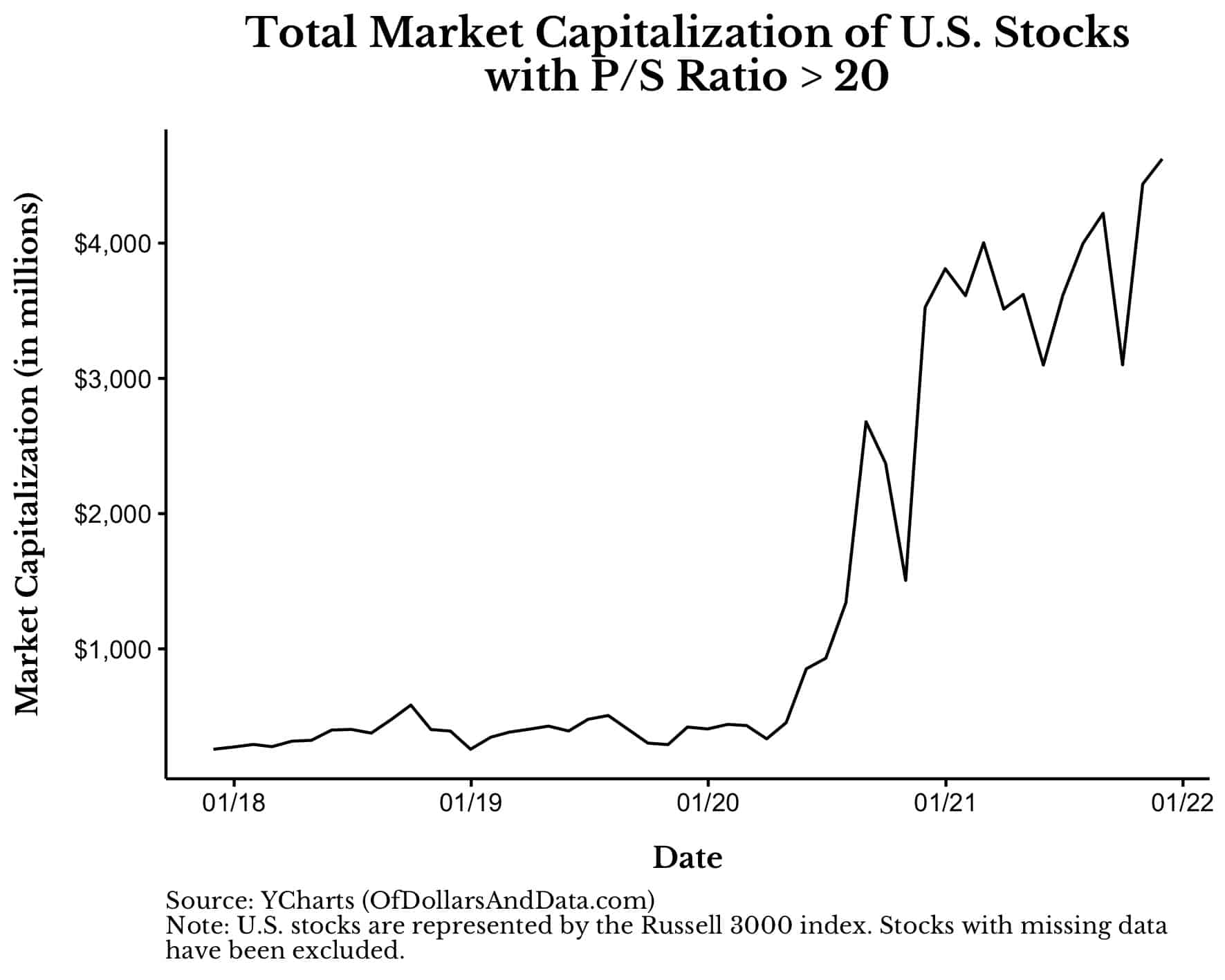

After seeing this chart I assumed there had been some sort of calculation error. There wasn’t. I recreated it using the Russell 3000 over the last four years and it was spot on:

With charts like this it’s hard not to compare everything happening today with the DotCom bubble. The easy money. The excess. The unbridled optimism. While the macroeconomic environment is very different today than during the late 1990s (i.e., interest rates are lower today), things still feel off.

Unfortunately, despite these obvious signs, we have no way of knowing how much longer this can go on for. Will it be one year? Three years? God forbid, ten years? I have no clue, but I do know that when people start to rush for the exits, it won’t be pretty. And I have some data to prove it.

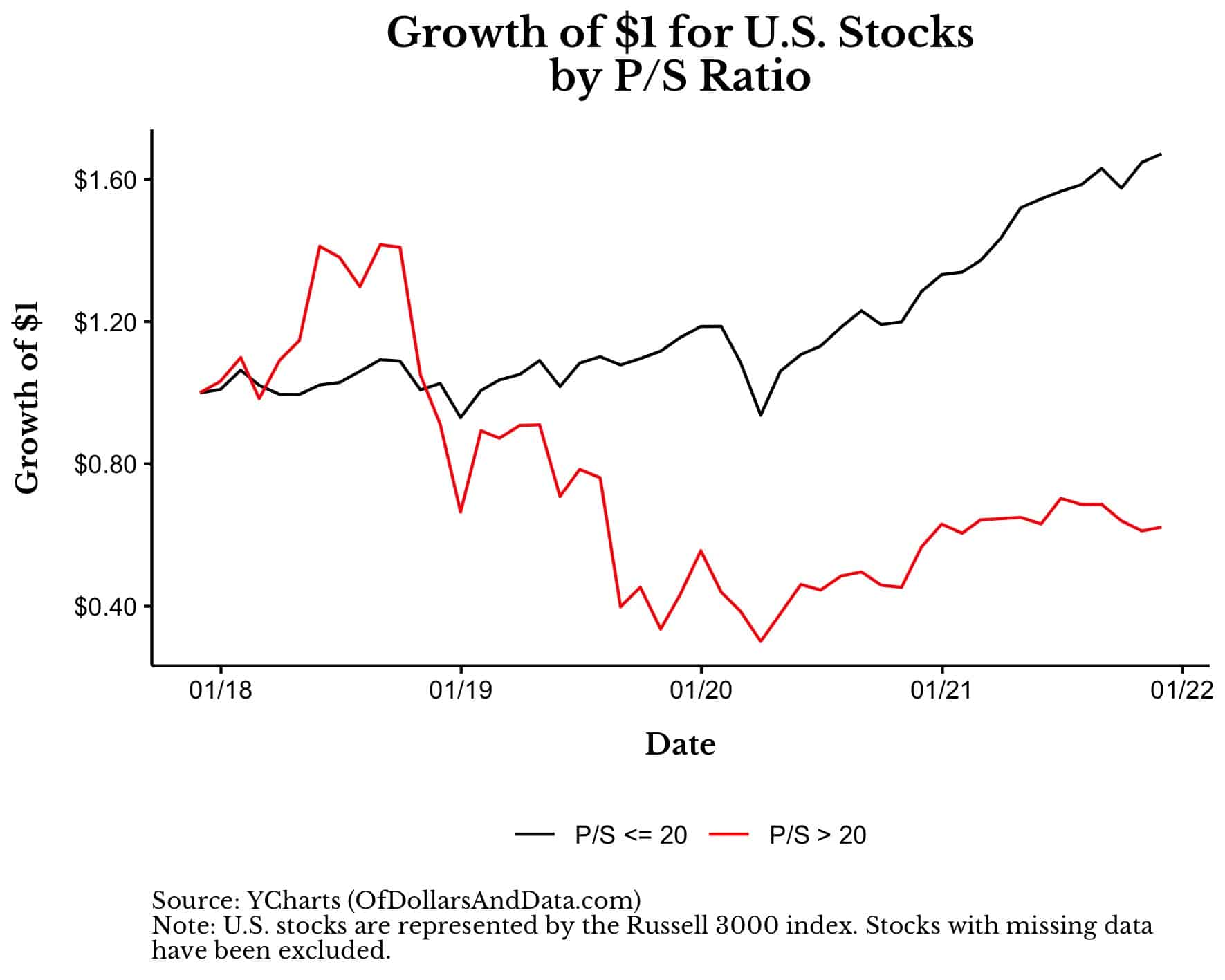

For example, if four years ago you looked at the stocks with a P/S ratio above 20 and those with a P/S ratio below 20, the above 20 group would have underperformed (and lost money on absolute terms) through today:

Of course, stocks with higher valuations don’t always underperform.

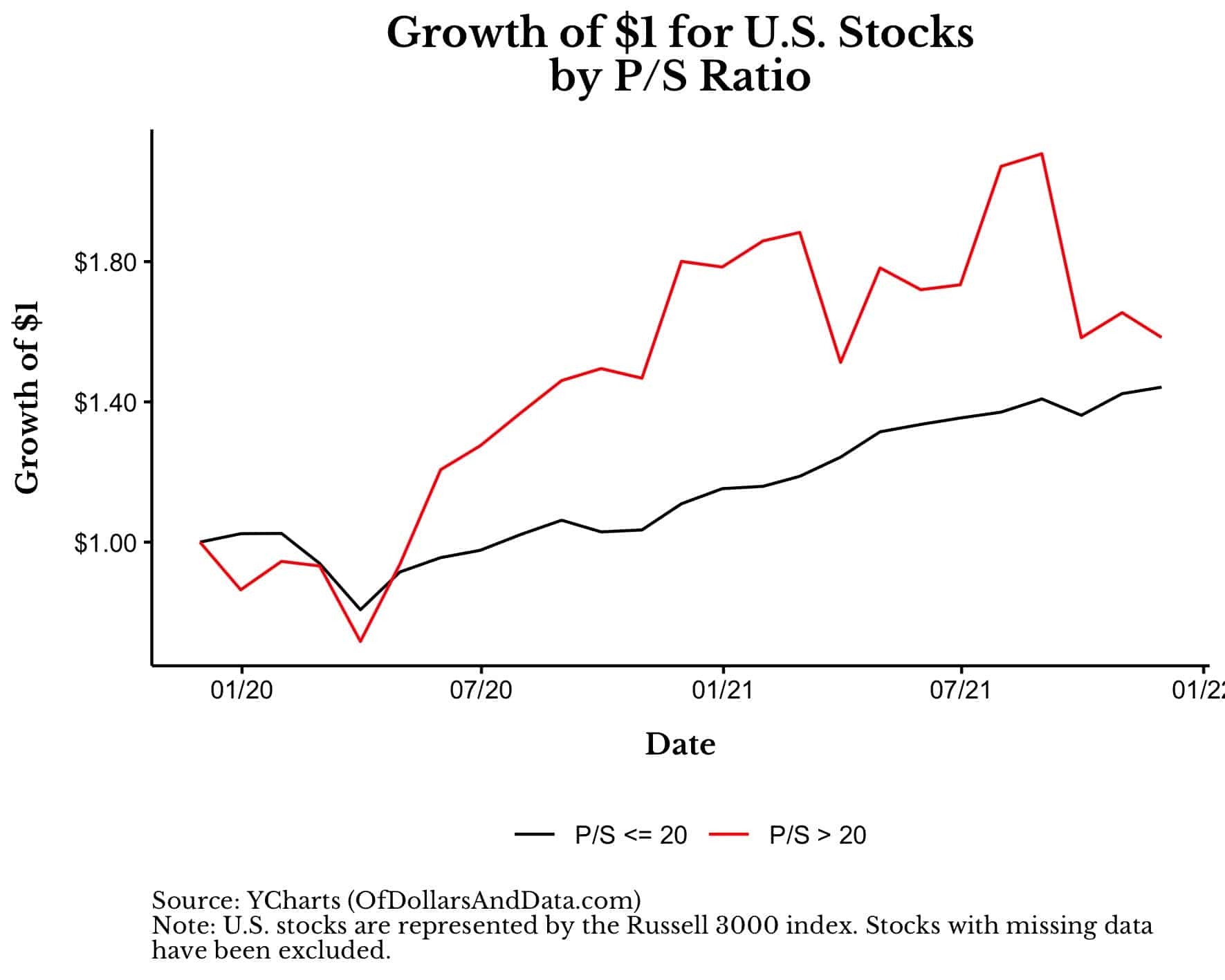

As the chart below illustrates, over the last two years those stocks with a P/S ratio greater than 20 have outperformed those with a P/S ratio less than 20:

But, as you can see, investing in higher P/S stocks seems like an asymmetric bet, and not a good one either. When higher P/S stocks win, they win by a little, but when they lose, they can lose by a lot.

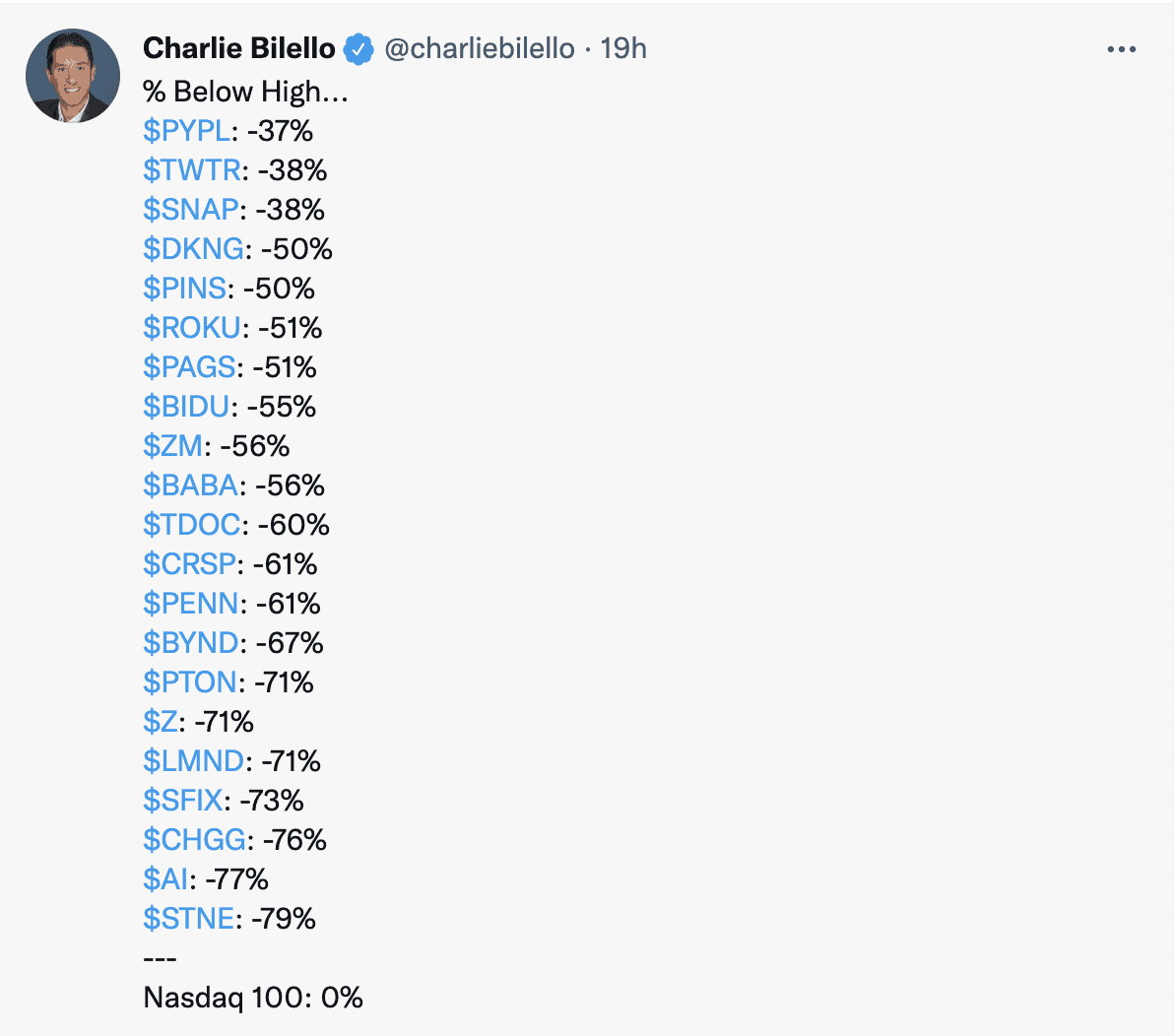

We have already seen this happen with some of the biggest winners of 2020, many of which had elevated valuations. As Charlie Bilello recently tweeted, despite the Nasdaq 100 hitting all-time highs, some popular names in tech are down bad:

Is this the future for memecoins and the overhyped stocks of today? I can’t say with certainty, but it seems so.

There’s this general feeling I have been having over the course of this year that just makes me feel like this has to be the case. It makes me feel like we know better. We know that what we are seeing isn’t sustainable, yet we can’t help but watch in awe from the sidelines.

It reminds me of what Stanley Druckenmiller said after he lost $3 billion during the DotCom bubble:

You asked me what I learned. I didn’t learn anything. I already knew that I wasn’t supposed to do that.

This encapsulates how I feel as I see pockets of the market descend into madness.

But what’s an investor to do?

Should you make a big shift to your allocation and get more defensive?

Should you stop buying altogether (if you aren’t retired)?

No. Both of these strategies are ill-advised, but there are some things that you can do to sleep better at night while investing in a market that seems overvalued.

How to Invest in an Overvalued Market (Hint: Sin a Little)

While we don’t know what the future holds, there are times when making small shifts to your investment strategy can make sense. Given the data above, now seems like one of those times. Is this market timing? Technically, yes. But it is market timing of the lowest degree.

My philosophy on this is stolen from Cliff Asness. If you are going to commit the sin of market timing, sin a little.

In practical terms this could mean any of the following:

- De-risking your portfolio to sell down the seemingly overvalued assets in exchange for more fairly valued assets.

- More frequent rebalancing across your portfolio.

- Reducing the rate at which you buy overvalued assets.

- Increasing the rate at which you buy assets less correlated with traditional financial markets.

Personally, I am not changing anything for my retirement accounts. I will still rebalance annually and keep buying the same percentage of U.S. stocks, international stocks, REITs, and U.S. bonds every month.

However, when it comes to my taxable brokerage account, no new dollars are going to U.S. stocks. Most of my new money is going into international stocks, crypto (with caution), or art (and farmland once I become an accredited investor). I have also made a slight increase to my emergency fund which is in cash. This is how I sin a little. You may find something else that works better for you.

Is this strategy foolproof? Of course not. U.S. stocks could end up ripping upward for another few years. But if they don’t, then you will be glad you sinned a little. Happy investing and thank you for reading!

If you liked this post, consider signing up for my newsletter.

This is post 269. Any code I have related to this post can be found here with the same numbering: https://github.com/nmaggiulli/of-dollars-and-data